The US and Iran remain locked in a hardline standoff, but the stagflation crisis has eased somewhat.

2026-03-10 15:44:41

US President Trump said on Monday that the war with Iran is progressing far faster than expected and could end "soon".

He stated that the United States is focused on securing global energy and oil supplies, a statement that contrasts with the previously set four to five-week timeframe. Trump later said that if Iran attempts to block the Strait of Hormuz, it will suffer a strike 20 times more powerful than the United States.

However, according to a report by Iran's Tasnim News Agency on the 10th, Iranian Islamic Revolutionary Guard Corps spokesman Naini publicly responded to Trump's remarks, stating that Iran currently possesses more powerful and numerous missiles aimed directly at US and Israeli military bases, directly refuting the US claim that Iran's military capabilities are declining and the war is about to end.

Around 11 a.m. thereafter, Hezbollah in Lebanon also announced an attack on an Israeli military stronghold, further escalating the conflict in the Middle East.

Iran's new Supreme Leader Mojtaba Khamenei has adopted a tough stance, with Iranian Foreign Minister Abbas Araqchi stating that negotiations with the United States are unlikely to be considered under Khamenei's leadership.

The above statement suggests that the protracted war may continue, but it indirectly reduces market concerns about disorderly oil price increases. This is precisely the sweet spot of capital that the war continues and inflation concerns subside, as mentioned in the previous article.

Previously, as the war escalated, the market began to price in more persistent energy supply shocks, with typical stagflation trading dominating the global market.

Rajiv DeMello, Global Macro Fund Manager at Gamma Asset Management, points out that investors are forced to raise their tail risk probability. The core contradiction of this supply shock is the stagflation characteristic—high inflation and low growth coexisting. This logic strongly echoes the oil crisis of the 1970s.

Stagflation concerns directly drove a sharp rise in global government bond yields. British bond yields have risen by about 50 basis points since the outbreak of the conflict, Turkish bond yields have nearly doubled, US bond yields have risen in tandem, and benchmark bond yields in countries such as Germany, the UK, New Zealand, and Australia have all seen significant increases, leading to a concentrated sell-off in the global bond market.

However, due to current news, government bond yields in various countries have fallen sharply, and at the same time, they have not rebounded significantly. This trend of declining inflation expectations and falling government bond yields is very conducive to the rebound of assets such as gold and equities.

(Daily chart of the yield on 10-year US Treasury bonds)

The stagflation panic once triggered a major shock to global capital markets, with global stock markets experiencing indiscriminate selling, resulting in a cumulative market value loss of $6 trillion.

The core market logic has shifted: rising inflation will significantly limit the central bank's room for interest rate cuts and will be unable to offset economic growth pressures.

Traders raised their U.S. inflation forecasts for the next two years, postponing the timing of the Federal Reserve's rate cut to September; European markets, meanwhile, began pricing in the possibility of the ECB and the Bank of England restarting rate hikes.

Monday saw particularly extreme market volatility: the Nikkei index plunged over 5% in a single day; Europe, as an energy-sensitive region, was hit hardest, with blue-chip stocks falling as much as 3.1% intraday.

However, as Trump signaled a possible easing of oil price concerns, US stocks collectively rebounded from their lows. The three major indices had fallen by more than 1.5% at one point during the session, but ultimately closed with the S&P 500 up 0.83%, the Dow Jones Industrial Average up 0.50%, and the Nasdaq up 1.385%. Later on Tuesday, the positive momentum spread to Asian equity markets during the Asian and European sessions, with the South Korean KOSPI up 5.35% and the Nikkei 225 up 2.78%.

(US and Asian stock indices)

There is a clear divergence between bulls and bears. Below are the analysts' views before and after the market opened on Monday:

Before Monday's rebound:

Andrew Taylor, global head of market intelligence at JPMorgan Chase, has turned tactically bearish on U.S. stocks, warning of further declines in the S&P 500.

Meanwhile, senior strategist Ed Yardeni raised his estimate of the probability of a market crash from 20% to 35%.

Macro strategist Skylar Montgomery Corning emphasized that obstruction in the Strait of Hormuz would push up energy and food costs, and the combination of stagflation would directly trigger the risk of a double whammy of stock and bond declines.

Furthermore, the cost of default protection for high-grade corporate bonds in Europe and Asia has risen to a new high since May, further exposing the vulnerability of the credit market. Under the impact of black swan events, only crude oil and the US dollar have shown independent trends.

The high volatility continues, with stagflation logic dominating asset pricing. This round of market correction also includes a correction of previous gains.

South Korean and Taiwanese stock markets have been driven to multi-year highs by the AI chip boom, with high valuations and substantial profits. The oil price shock further amplifies the pressure for a correction, highlighting Asia's high sensitivity to energy disturbances in the Middle East.

Coupled with the slowdown in US economic momentum and an unexpected decline in February employment data, market adjustment pressures continue to accumulate.

Wilson Asset Management hedge fund manager Matthew Haupt stated bluntly that the current market risks are entirely bearish, and there is no clear timetable for the end of the conflict.

Hiroya Akizawa, a fund manager at Tokyo Marine Asset Management, said that the market is dominated by panic and he is actively increasing his cash holdings.

Until there are clear signs of easing tensions in the Middle East, stagflation risks will continue to dominate global asset pricing, and high market volatility will persist.

After Monday's rebound:

In response to Monday's sharp rebound in US stocks, major institutions offered diverse interpretations after assessing geopolitical risks and economic resilience.

Charles Schwab's Michelle Gibley cautioned investors to remain vigilant, warning of the erosion of corporate profits by persistently high energy costs and to closely monitor whether analysts will lower earnings forecasts in the first quarter due to war and weak employment data.

JPMorgan's Hussein Malik remains optimistic about 2026 overall, emphasizing that AI investment will continue to drive the market and that he is optimistic about the growth potential of global stock markets even with a 35% probability of recession.

LivelongWealth analyst Hariprasad K pointed out that the rapid pullback in crude oil prices from their highs was the direct catalyst for this rebound, and this "roller coaster" market reflects the market's extreme sensitivity to the situation in the Middle East.

EnrichMoney's PonmudiR believes that Trump's comments about the potential end of the conflict are key to reshaping risk appetite.

Jurrien Timmer of Fidelity Investments added that the current growth logic has shifted to earnings-driven, and as long as the S&P 500 can deliver double-digit earnings growth, the stock market can absorb the risk of overvaluation.

Fundstrat's Mark Newton, from a technical perspective, believes that the volatility in 2026 is a phase of adjustment within a bull market, and pullbacks present buying opportunities. Finally, SCFR reminds investors to pay attention to the consumer sector, as fluctuations in energy prices are often a leading indicator of weakening earnings reports in this sector.

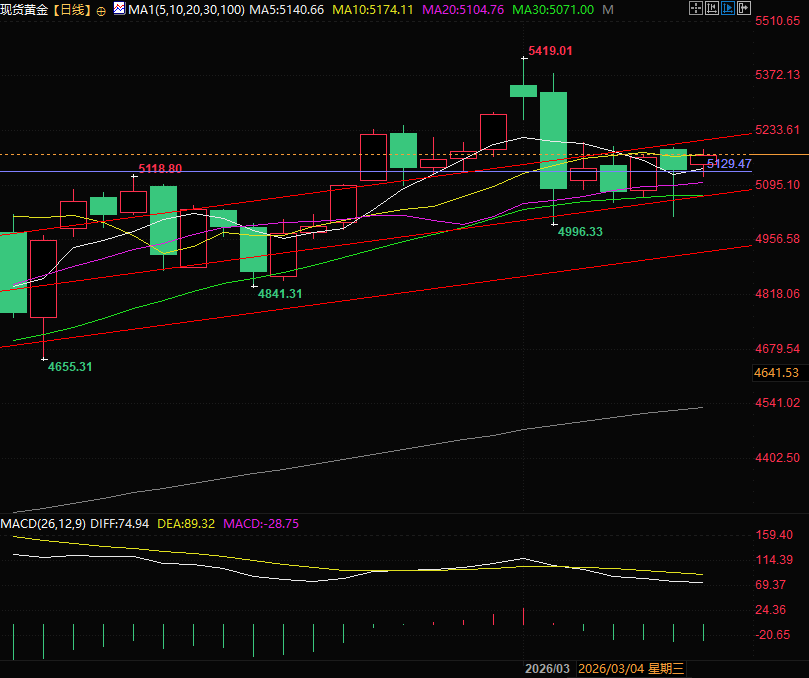

Recently, oil prices and inflation narratives have become highly correlated; when oil prices fall, government bond yields in various countries fall, while gold and equity markets rebound.

As a result, gold has risen above the key level of 5130 and held above the five-day moving average. As long as the rise in oil prices slows down and the war continues, gold is expected to continue to rise.

(Spot gold daily chart, source: FX678)

At 15:42 Beijing time, spot gold was trading at $5175.45 per ounce.

He stated that the United States is focused on securing global energy and oil supplies, a statement that contrasts with the previously set four to five-week timeframe. Trump later said that if Iran attempts to block the Strait of Hormuz, it will suffer a strike 20 times more powerful than the United States.

However, according to a report by Iran's Tasnim News Agency on the 10th, Iranian Islamic Revolutionary Guard Corps spokesman Naini publicly responded to Trump's remarks, stating that Iran currently possesses more powerful and numerous missiles aimed directly at US and Israeli military bases, directly refuting the US claim that Iran's military capabilities are declining and the war is about to end.

Around 11 a.m. thereafter, Hezbollah in Lebanon also announced an attack on an Israeli military stronghold, further escalating the conflict in the Middle East.

Iran's new Supreme Leader Mojtaba Khamenei has adopted a tough stance, with Iranian Foreign Minister Abbas Araqchi stating that negotiations with the United States are unlikely to be considered under Khamenei's leadership.

The above statement suggests that the protracted war may continue, but it indirectly reduces market concerns about disorderly oil price increases. This is precisely the sweet spot of capital that the war continues and inflation concerns subside, as mentioned in the previous article.

Stagflation trading once caused global bond yields to surge across the board.

Previously, as the war escalated, the market began to price in more persistent energy supply shocks, with typical stagflation trading dominating the global market.

Rajiv DeMello, Global Macro Fund Manager at Gamma Asset Management, points out that investors are forced to raise their tail risk probability. The core contradiction of this supply shock is the stagflation characteristic—high inflation and low growth coexisting. This logic strongly echoes the oil crisis of the 1970s.

Stagflation concerns directly drove a sharp rise in global government bond yields. British bond yields have risen by about 50 basis points since the outbreak of the conflict, Turkish bond yields have nearly doubled, US bond yields have risen in tandem, and benchmark bond yields in countries such as Germany, the UK, New Zealand, and Australia have all seen significant increases, leading to a concentrated sell-off in the global bond market.

However, due to current news, government bond yields in various countries have fallen sharply, and at the same time, they have not rebounded significantly. This trend of declining inflation expectations and falling government bond yields is very conducive to the rebound of assets such as gold and equities.

(Daily chart of the yield on 10-year US Treasury bonds)

Global capital markets experienced a sharp fluctuation, followed by a double whammy of falling stocks and bonds before rebounding from their lows.

The stagflation panic once triggered a major shock to global capital markets, with global stock markets experiencing indiscriminate selling, resulting in a cumulative market value loss of $6 trillion.

The core market logic has shifted: rising inflation will significantly limit the central bank's room for interest rate cuts and will be unable to offset economic growth pressures.

Traders raised their U.S. inflation forecasts for the next two years, postponing the timing of the Federal Reserve's rate cut to September; European markets, meanwhile, began pricing in the possibility of the ECB and the Bank of England restarting rate hikes.

Monday saw particularly extreme market volatility: the Nikkei index plunged over 5% in a single day; Europe, as an energy-sensitive region, was hit hardest, with blue-chip stocks falling as much as 3.1% intraday.

However, as Trump signaled a possible easing of oil price concerns, US stocks collectively rebounded from their lows. The three major indices had fallen by more than 1.5% at one point during the session, but ultimately closed with the S&P 500 up 0.83%, the Dow Jones Industrial Average up 0.50%, and the Nasdaq up 1.385%. Later on Tuesday, the positive momentum spread to Asian equity markets during the Asian and European sessions, with the South Korean KOSPI up 5.35% and the Nikkei 225 up 2.78%.

(US and Asian stock indices)

A clear divergence between bulls and bears suggests that the market is in a period of high volatility.

There is a clear divergence between bulls and bears. Below are the analysts' views before and after the market opened on Monday:

Before Monday's rebound:

Andrew Taylor, global head of market intelligence at JPMorgan Chase, has turned tactically bearish on U.S. stocks, warning of further declines in the S&P 500.

Meanwhile, senior strategist Ed Yardeni raised his estimate of the probability of a market crash from 20% to 35%.

Macro strategist Skylar Montgomery Corning emphasized that obstruction in the Strait of Hormuz would push up energy and food costs, and the combination of stagflation would directly trigger the risk of a double whammy of stock and bond declines.

Furthermore, the cost of default protection for high-grade corporate bonds in Europe and Asia has risen to a new high since May, further exposing the vulnerability of the credit market. Under the impact of black swan events, only crude oil and the US dollar have shown independent trends.

The high volatility continues, with stagflation logic dominating asset pricing. This round of market correction also includes a correction of previous gains.

South Korean and Taiwanese stock markets have been driven to multi-year highs by the AI chip boom, with high valuations and substantial profits. The oil price shock further amplifies the pressure for a correction, highlighting Asia's high sensitivity to energy disturbances in the Middle East.

Coupled with the slowdown in US economic momentum and an unexpected decline in February employment data, market adjustment pressures continue to accumulate.

Wilson Asset Management hedge fund manager Matthew Haupt stated bluntly that the current market risks are entirely bearish, and there is no clear timetable for the end of the conflict.

Hiroya Akizawa, a fund manager at Tokyo Marine Asset Management, said that the market is dominated by panic and he is actively increasing his cash holdings.

Until there are clear signs of easing tensions in the Middle East, stagflation risks will continue to dominate global asset pricing, and high market volatility will persist.

After Monday's rebound:

In response to Monday's sharp rebound in US stocks, major institutions offered diverse interpretations after assessing geopolitical risks and economic resilience.

Charles Schwab's Michelle Gibley cautioned investors to remain vigilant, warning of the erosion of corporate profits by persistently high energy costs and to closely monitor whether analysts will lower earnings forecasts in the first quarter due to war and weak employment data.

JPMorgan's Hussein Malik remains optimistic about 2026 overall, emphasizing that AI investment will continue to drive the market and that he is optimistic about the growth potential of global stock markets even with a 35% probability of recession.

LivelongWealth analyst Hariprasad K pointed out that the rapid pullback in crude oil prices from their highs was the direct catalyst for this rebound, and this "roller coaster" market reflects the market's extreme sensitivity to the situation in the Middle East.

EnrichMoney's PonmudiR believes that Trump's comments about the potential end of the conflict are key to reshaping risk appetite.

Jurrien Timmer of Fidelity Investments added that the current growth logic has shifted to earnings-driven, and as long as the S&P 500 can deliver double-digit earnings growth, the stock market can absorb the risk of overvaluation.

Fundstrat's Mark Newton, from a technical perspective, believes that the volatility in 2026 is a phase of adjustment within a bull market, and pullbacks present buying opportunities. Finally, SCFR reminds investors to pay attention to the consumer sector, as fluctuations in energy prices are often a leading indicator of weakening earnings reports in this sector.

Summary and Technical Analysis:

Recently, oil prices and inflation narratives have become highly correlated; when oil prices fall, government bond yields in various countries fall, while gold and equity markets rebound.

As a result, gold has risen above the key level of 5130 and held above the five-day moving average. As long as the rise in oil prices slows down and the war continues, gold is expected to continue to rise.

(Spot gold daily chart, source: FX678)

At 15:42 Beijing time, spot gold was trading at $5175.45 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.