The ongoing geopolitical conflict with Iran could cause Qatar and Kuwait's GDP to shrink by 14%. Goldman Sachs predicts the Gulf economy faces its worst recession since the 1990s.

2026-03-16 10:27:31

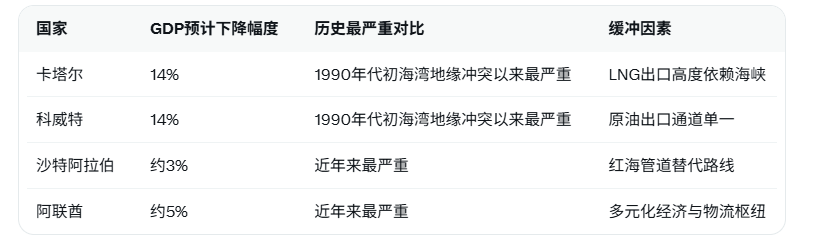

According to APP, as the geopolitical conflict with Iran enters a critical phase, if the conflict fails to subside quickly, core Gulf economies, including Saudi Arabia, the UAE, and Qatar, may face the risk of their most severe economic downturn since the 1990s. A recent scenario simulation by Farouk Soussa, an economist specializing in the Middle East and North Africa at a well-known international financial institution, indicates that assuming the geopolitical conflict continues until April and the Strait of Hormuz is closed for two months, Qatar and Kuwait's GDP will each shrink by 14% this year. This would be the most severe recession for both countries since the Gulf geopolitical conflict began in the early 1990s.

In contrast, Saudi Arabia and the UAE, with their alternative transportation routes such as pipelines, are in a relatively buffered position, but still cannot completely avoid the impact. Analysts predict that their GDPs will decline by approximately 3% and 5% respectively, representing the most significant economic downturn in recent years. Susa recently emphasized: "For many Gulf economies, the short-term impact of this geopolitical conflict may be more severe. When the dust settles, they will rebuild and recover, but the damage this conflict has left to market confidence remains to be seen."

The impact of geopolitical conflicts extends far beyond simple oil price fluctuations. The Strait of Hormuz handles approximately 20% of global oil and liquefied natural gas (LNG) transport; its disruption would not only drastically reduce exports but also directly impact non-oil sectors. Qatar, one of the world's largest LNG exporters, has already seen its LNG production capacity effectively hampered, causing a chain reaction in European and Asian energy markets. Kuwait, heavily reliant on a single crude oil route, is facing pressure on its domestic refining and petrochemical industry chain. While Saudi Arabia can bypass the issue through the Red Sea pipeline, non-oil industries such as tourism, financial services, and investment confidence in large-scale projects will be dampened. Dubai's hub status in the UAE also faces the dual challenges of shipping delays and soaring logistics costs.

Brent crude oil prices have now climbed above $100 per barrel due to supply uncertainty. While this provides a short-term revenue buffer for oil-producing countries, it cannot compensate for the losses caused by the sharp drop in transportation volumes. Analysts indicate that this "double whammy"—disruptions in exports coupled with a contraction in non-oil activities—will amplify economic vulnerability far beyond the mere premium of geopolitical risk.

The following is a comparison of the GDP impact on major Gulf economies under the worst-case scenario (based on the latest institutional scenario simulation):

Historically, the Gulf states experienced a similar precipitous decline in GDP during the Gulf conflicts of the 1990s. This current conflict simultaneously impacts energy exports and global confidence, potentially leading to a longer recovery period. Recent comments by Susa further indicate that while Gulf states possess fiscal buffers (such as sovereign wealth funds), market participants' concerns about regional stability will continue to affect foreign investment inflows and project financing costs.

Overall, the current geopolitical conflict with Iran highlights the Gulf economies' heavy reliance on key energy routes. While significant short-term economic pain is expected, the region's potential for recovery remains, thanks to existing diversified reforms and alternative infrastructure. Investors need to closely monitor the duration of the conflict and the progress of shipping route reopening to assess the transmission effects of oil and gas price volatility on global supply chains.

Editor's Summary : The Gulf economies are facing supply disruptions driven by geopolitical risks: blocked export routes and declining confidence in the non-oil sector are creating combined pressure. Qatar and Kuwait have experienced the largest declines, while Saudi Arabia and the UAE have benefited from infrastructure buffers, resulting in relatively milder losses. Market confidence recovery will be a key variable in the recovery process. Short-term pain may accelerate regional energy diversification and the development of alternative routes, while in the long term, it will test the fiscal resilience of individual countries and the efficiency of global energy pricing transmission.

Frequently Asked Questions

1. Why does the geopolitical conflict in Iran have such a severe impact on the GDP of the Gulf economy?

The conflict directly disrupted shipping through the Strait of Hormuz, leading to a significant reduction in oil and liquefied natural gas exports. Qatar and Kuwait rely almost entirely on this passage, and a two-month export disruption resulted in idle capacity and supply chain stagnation. Even rising oil prices could not compensate for the reduced volume, and coupled with declining confidence in non-oil sectors, this created a compounding recessionary effect.

2. Why are Saudi Arabia and the UAE relatively "resistant to shocks"?

Both countries possess alternative routes, such as the Red Sea pipeline, which can partially bypass the strait and divert oil exports. Furthermore, their economies are highly diversified (tourism, finance, and technology projects), mitigating their reliance on a single energy source. However, non-oil industries are still affected by logistical delays and investor hesitancy, and GDP is expected to experience its largest decline in recent years.

3. What historical significance does the 14% contraction in Qatar and Kuwait represent?

This equates to the most severe economic contraction for both countries since the Gulf geopolitical conflict of the early 1990s, when the event directly destroyed infrastructure and disrupted exports. In this scenario, the dual shutdown of LNG and crude oil will amplify the effects, far exceeding the scale of previous fluctuations.

4. What cascading effects will the conflict have on the global energy market?

The disruption to the Strait of Hormuz pushed Brent crude oil prices above $100 per barrel, increasing import costs for both Europe and Asia, and causing natural gas prices to fluctuate in tandem. Major Asian countries face challenges to their energy security, with some potentially needing to switch to other suppliers, increasing short-term inflationary pressures.

In contrast, Saudi Arabia and the UAE, with their alternative transportation routes such as pipelines, are in a relatively buffered position, but still cannot completely avoid the impact. Analysts predict that their GDPs will decline by approximately 3% and 5% respectively, representing the most significant economic downturn in recent years. Susa recently emphasized: "For many Gulf economies, the short-term impact of this geopolitical conflict may be more severe. When the dust settles, they will rebuild and recover, but the damage this conflict has left to market confidence remains to be seen."

The impact of geopolitical conflicts extends far beyond simple oil price fluctuations. The Strait of Hormuz handles approximately 20% of global oil and liquefied natural gas (LNG) transport; its disruption would not only drastically reduce exports but also directly impact non-oil sectors. Qatar, one of the world's largest LNG exporters, has already seen its LNG production capacity effectively hampered, causing a chain reaction in European and Asian energy markets. Kuwait, heavily reliant on a single crude oil route, is facing pressure on its domestic refining and petrochemical industry chain. While Saudi Arabia can bypass the issue through the Red Sea pipeline, non-oil industries such as tourism, financial services, and investment confidence in large-scale projects will be dampened. Dubai's hub status in the UAE also faces the dual challenges of shipping delays and soaring logistics costs.

Brent crude oil prices have now climbed above $100 per barrel due to supply uncertainty. While this provides a short-term revenue buffer for oil-producing countries, it cannot compensate for the losses caused by the sharp drop in transportation volumes. Analysts indicate that this "double whammy"—disruptions in exports coupled with a contraction in non-oil activities—will amplify economic vulnerability far beyond the mere premium of geopolitical risk.

The following is a comparison of the GDP impact on major Gulf economies under the worst-case scenario (based on the latest institutional scenario simulation):

Historically, the Gulf states experienced a similar precipitous decline in GDP during the Gulf conflicts of the 1990s. This current conflict simultaneously impacts energy exports and global confidence, potentially leading to a longer recovery period. Recent comments by Susa further indicate that while Gulf states possess fiscal buffers (such as sovereign wealth funds), market participants' concerns about regional stability will continue to affect foreign investment inflows and project financing costs.

Overall, the current geopolitical conflict with Iran highlights the Gulf economies' heavy reliance on key energy routes. While significant short-term economic pain is expected, the region's potential for recovery remains, thanks to existing diversified reforms and alternative infrastructure. Investors need to closely monitor the duration of the conflict and the progress of shipping route reopening to assess the transmission effects of oil and gas price volatility on global supply chains.

Editor's Summary : The Gulf economies are facing supply disruptions driven by geopolitical risks: blocked export routes and declining confidence in the non-oil sector are creating combined pressure. Qatar and Kuwait have experienced the largest declines, while Saudi Arabia and the UAE have benefited from infrastructure buffers, resulting in relatively milder losses. Market confidence recovery will be a key variable in the recovery process. Short-term pain may accelerate regional energy diversification and the development of alternative routes, while in the long term, it will test the fiscal resilience of individual countries and the efficiency of global energy pricing transmission.

Frequently Asked Questions

1. Why does the geopolitical conflict in Iran have such a severe impact on the GDP of the Gulf economy?

The conflict directly disrupted shipping through the Strait of Hormuz, leading to a significant reduction in oil and liquefied natural gas exports. Qatar and Kuwait rely almost entirely on this passage, and a two-month export disruption resulted in idle capacity and supply chain stagnation. Even rising oil prices could not compensate for the reduced volume, and coupled with declining confidence in non-oil sectors, this created a compounding recessionary effect.

2. Why are Saudi Arabia and the UAE relatively "resistant to shocks"?

Both countries possess alternative routes, such as the Red Sea pipeline, which can partially bypass the strait and divert oil exports. Furthermore, their economies are highly diversified (tourism, finance, and technology projects), mitigating their reliance on a single energy source. However, non-oil industries are still affected by logistical delays and investor hesitancy, and GDP is expected to experience its largest decline in recent years.

3. What historical significance does the 14% contraction in Qatar and Kuwait represent?

This equates to the most severe economic contraction for both countries since the Gulf geopolitical conflict of the early 1990s, when the event directly destroyed infrastructure and disrupted exports. In this scenario, the dual shutdown of LNG and crude oil will amplify the effects, far exceeding the scale of previous fluctuations.

4. What cascading effects will the conflict have on the global energy market?

The disruption to the Strait of Hormuz pushed Brent crude oil prices above $100 per barrel, increasing import costs for both Europe and Asia, and causing natural gas prices to fluctuate in tandem. Major Asian countries face challenges to their energy security, with some potentially needing to switch to other suppliers, increasing short-term inflationary pressures.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.