The oil price shock has completely reversed the path of interest rate cuts, and the European Central Bank is expected to hold rates steady at its meeting this week.

2026-03-17 14:35:06

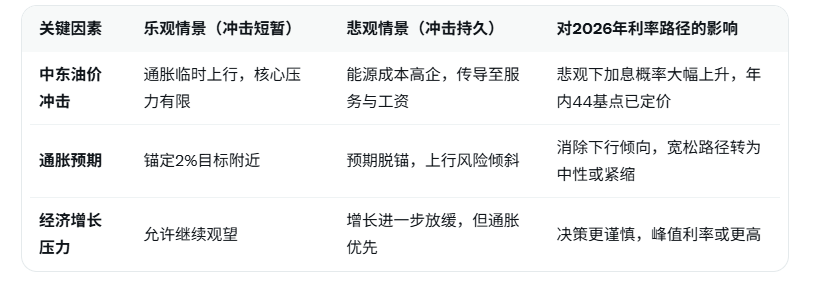

According to APP, Vanguard economist Josefina Rodríguez stated that it is premature for the European Central Bank (ECB) to hint at adjusting its policy stance. Speaking about the Middle East crisis and the ensuing surge in oil prices, she emphasized, "It largely depends on the magnitude and ultimate persistence of the shock." The institution maintains its baseline forecast for ECB policy, namely that interest rates will remain unchanged until the end of 2026 , but "we have eliminated the previous downward bias in the outlook for policy rates." This means that the previously implied room for further easing has been completely removed, in favor of more persistent inflationary pressures. LSEG money market data shows that the probability of the ECB maintaining the main refinancing rate at 3.65% and the deposit facility rate at 3.25% at this week's (March 17-18) meeting is close to 100% , but the market has already priced in a cumulative 44 basis point rate hike by 2026 , a significant upward revision from previous expectations, reflecting the reshaping of inflation expectations by the energy shock.

The geopolitical conflict in the Middle East has led to a sharp rise in oil prices, becoming the biggest uncertainty factor in the current inflation outlook for the Eurozone. Rodriguez points out that the magnitude and duration of the oil price surge will directly determine whether the ECB is forced to shift from a "wait-and-see" approach to "re-tightening." If the shock is short-lived, inflation may only rise temporarily, and the ECB can still adhere to its data-dependent approach; however, if high energy costs are transmitted to core inflation, it may force policymakers to shift to raising interest rates in 2026 to anchor expectations. The ECB has recently repeatedly emphasized its "high attention" to supply-side risks while reiterating its dual mandate (price stability and economic support), but the risk of inflation exceeding the 2% target has significantly cooled expectations for further easing.

The shift in money market pricing is particularly significant: the tail risk previously implied by the market, suggesting a potential for rate cuts or even negative interest rates in 2026 , has now been ruled out. LSEG data shows that a 44 basis point rate hike this year roughly corresponds to 1-2 increases of 25 basis points each, with peak interest rates potentially reaching the 4.00%-4.25% range. This reflects investors' combined concerns about the persistence of the energy shock, the risk of inflation expectations decoupling, and the maintenance of the ECB's credibility. While the Eurozone economy faces pressure from slowing growth (such as continued weakness in manufacturing and a slow recovery in consumption), the resilience of the labor market and wage growth continue to support stubborn core inflation, limiting the scope for further easing.

Overall, the ECB meeting this week is highly likely to leave interest rates unchanged, but President Lagarde's press conference and updated economic forecasts will be the focus. If the sustainability of the shocks described by Rodriguez is confirmed, market-priced expectations of a rate hike this year may strengthen further, potentially supporting the euro and putting pressure on risk assets. Conversely, if oil prices fall rapidly or inflation data eases, the door to easing could still be reopened. The current environment makes the ECB's policy path highly dependent on geopolitical and energy dynamics; investors need to closely monitor Brent crude oil prices, Eurozone HICP data, and the ECB's forward guidance.

Editor's Summary:

The European Central Bank (ECB) is highly likely to keep interest rates unchanged at its meeting this week. However, Vanguard economist Rodriguez points out that the Middle East oil price shock has completely eliminated the previous easing bias, and the policy path will shift to neutral to tight in 2026. The money market's expectation of a 44 basis point rate hike this year highlights the tilt towards inflation risks. ECB decisions will be highly dependent on the persistence of the shock, and the market needs to be wary of the profound impact of energy prices on the Eurozone's outlook.

Frequently Asked Questions

1. Why does the European Central Bank currently believe it is too early to adjust its policy stance?

The ECB assesses that current inflation dynamics remain dominated by supply-side shocks, particularly the surge in oil prices triggered by the Middle East crisis. Rodriguez emphasized that policy adjustments will depend on the magnitude and duration of the shock. If the energy price increase is merely a short-term disturbance, inflation may subside on its own, and the ECB can continue to remain on the sidelines. However, if the shock is persistent and transmits to the core, a reassessment is necessary. At present, there is insufficient evidence for an immediate shift, and maintaining data-driven reliance is prioritized to avoid premature action that could damage credibility.

2. What does "eliminating the previous downward bias in the outlook for policy rates" specifically mean?

Previous market and ECB forecasts implied the possibility of further interest rate cuts or even the tail risk of negative interest rates in 2026 to address economic slowdown. However, due to the oil price shock boosting inflation expectations, this downward bias has been completely removed, and the interest rate path has shifted from neutral-to-dovish to neutral-to-hawkish. This means that the room for easing has been significantly reduced, and future policies are more likely to remain stable or slightly increase, rather than continue to decrease.

3. How was the LSEG money market's 44 basis point rate hike this year calculated?

LSEG's implied pricing through short-term euro interest rate futures indicates that the market expects a cumulative 44 basis point rate hikes by 2026 , roughly corresponding to 1-2 increases of 25 basis points each (possibly accompanied by a tail adjustment). This is a significant upward revision from previous pricing, reflecting investors' comprehensive assessment of the persistence of the energy shock, the decoupling of inflation expectations, and the ECB's need to maintain price stability.

4. How much impact will the Middle East oil price shock have on the European Central Bank's decision-making?

Rodriguez stated bluntly that it "largely depends on the magnitude and ultimate persistence of the shock." Soaring oil prices directly push up imported inflation; if they remain high, they will be passed on to transportation, manufacturing, and service prices through energy costs, amplifying core inflationary pressures and raising inflation expectations. If the shock is short-lived (e.g., the conflict is quickly resolved), the impact will be manageable; if it is prolonged, it may force the ECB to shift to interest rate hikes in 2026 to prevent inflation from spiraling out of control, becoming a key variable dominating the policy path.

5. What are the potential impacts of the outcome of this meeting on the Eurozone economy and financial markets?

The meeting is highly unlikely to adjust interest rates. However, if the chairman's press conference confirms the elimination of easing tendencies and emphasizes inflation risks, the euro may strengthen, bond yields may rise, and European stocks and risk assets may come under pressure. If a more dovish signal is unexpectedly released (though this is unlikely), the euro will be pressured and risk assets may rebound. In the long term, the priced-in 44 basis point rate hike this year will increase borrowing costs and suppress consumption and investment. Investors should pay attention to oil prices, the HICP inflation component, and ECB forecast updates.

The geopolitical conflict in the Middle East has led to a sharp rise in oil prices, becoming the biggest uncertainty factor in the current inflation outlook for the Eurozone. Rodriguez points out that the magnitude and duration of the oil price surge will directly determine whether the ECB is forced to shift from a "wait-and-see" approach to "re-tightening." If the shock is short-lived, inflation may only rise temporarily, and the ECB can still adhere to its data-dependent approach; however, if high energy costs are transmitted to core inflation, it may force policymakers to shift to raising interest rates in 2026 to anchor expectations. The ECB has recently repeatedly emphasized its "high attention" to supply-side risks while reiterating its dual mandate (price stability and economic support), but the risk of inflation exceeding the 2% target has significantly cooled expectations for further easing.

The shift in money market pricing is particularly significant: the tail risk previously implied by the market, suggesting a potential for rate cuts or even negative interest rates in 2026 , has now been ruled out. LSEG data shows that a 44 basis point rate hike this year roughly corresponds to 1-2 increases of 25 basis points each, with peak interest rates potentially reaching the 4.00%-4.25% range. This reflects investors' combined concerns about the persistence of the energy shock, the risk of inflation expectations decoupling, and the maintenance of the ECB's credibility. While the Eurozone economy faces pressure from slowing growth (such as continued weakness in manufacturing and a slow recovery in consumption), the resilience of the labor market and wage growth continue to support stubborn core inflation, limiting the scope for further easing.

Overall, the ECB meeting this week is highly likely to leave interest rates unchanged, but President Lagarde's press conference and updated economic forecasts will be the focus. If the sustainability of the shocks described by Rodriguez is confirmed, market-priced expectations of a rate hike this year may strengthen further, potentially supporting the euro and putting pressure on risk assets. Conversely, if oil prices fall rapidly or inflation data eases, the door to easing could still be reopened. The current environment makes the ECB's policy path highly dependent on geopolitical and energy dynamics; investors need to closely monitor Brent crude oil prices, Eurozone HICP data, and the ECB's forward guidance.

Editor's Summary:

The European Central Bank (ECB) is highly likely to keep interest rates unchanged at its meeting this week. However, Vanguard economist Rodriguez points out that the Middle East oil price shock has completely eliminated the previous easing bias, and the policy path will shift to neutral to tight in 2026. The money market's expectation of a 44 basis point rate hike this year highlights the tilt towards inflation risks. ECB decisions will be highly dependent on the persistence of the shock, and the market needs to be wary of the profound impact of energy prices on the Eurozone's outlook.

Frequently Asked Questions

1. Why does the European Central Bank currently believe it is too early to adjust its policy stance?

The ECB assesses that current inflation dynamics remain dominated by supply-side shocks, particularly the surge in oil prices triggered by the Middle East crisis. Rodriguez emphasized that policy adjustments will depend on the magnitude and duration of the shock. If the energy price increase is merely a short-term disturbance, inflation may subside on its own, and the ECB can continue to remain on the sidelines. However, if the shock is persistent and transmits to the core, a reassessment is necessary. At present, there is insufficient evidence for an immediate shift, and maintaining data-driven reliance is prioritized to avoid premature action that could damage credibility.

2. What does "eliminating the previous downward bias in the outlook for policy rates" specifically mean?

Previous market and ECB forecasts implied the possibility of further interest rate cuts or even the tail risk of negative interest rates in 2026 to address economic slowdown. However, due to the oil price shock boosting inflation expectations, this downward bias has been completely removed, and the interest rate path has shifted from neutral-to-dovish to neutral-to-hawkish. This means that the room for easing has been significantly reduced, and future policies are more likely to remain stable or slightly increase, rather than continue to decrease.

3. How was the LSEG money market's 44 basis point rate hike this year calculated?

LSEG's implied pricing through short-term euro interest rate futures indicates that the market expects a cumulative 44 basis point rate hikes by 2026 , roughly corresponding to 1-2 increases of 25 basis points each (possibly accompanied by a tail adjustment). This is a significant upward revision from previous pricing, reflecting investors' comprehensive assessment of the persistence of the energy shock, the decoupling of inflation expectations, and the ECB's need to maintain price stability.

4. How much impact will the Middle East oil price shock have on the European Central Bank's decision-making?

Rodriguez stated bluntly that it "largely depends on the magnitude and ultimate persistence of the shock." Soaring oil prices directly push up imported inflation; if they remain high, they will be passed on to transportation, manufacturing, and service prices through energy costs, amplifying core inflationary pressures and raising inflation expectations. If the shock is short-lived (e.g., the conflict is quickly resolved), the impact will be manageable; if it is prolonged, it may force the ECB to shift to interest rate hikes in 2026 to prevent inflation from spiraling out of control, becoming a key variable dominating the policy path.

5. What are the potential impacts of the outcome of this meeting on the Eurozone economy and financial markets?

The meeting is highly unlikely to adjust interest rates. However, if the chairman's press conference confirms the elimination of easing tendencies and emphasizes inflation risks, the euro may strengthen, bond yields may rise, and European stocks and risk assets may come under pressure. If a more dovish signal is unexpectedly released (though this is unlikely), the euro will be pressured and risk assets may rebound. In the long term, the priced-in 44 basis point rate hike this year will increase borrowing costs and suppress consumption and investment. Investors should pay attention to oil prices, the HICP inflation component, and ECB forecast updates.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.