Escalating conflict in Iran hits upstream oil fields, could oil prices soar to $120?

2026-03-17 15:00:57

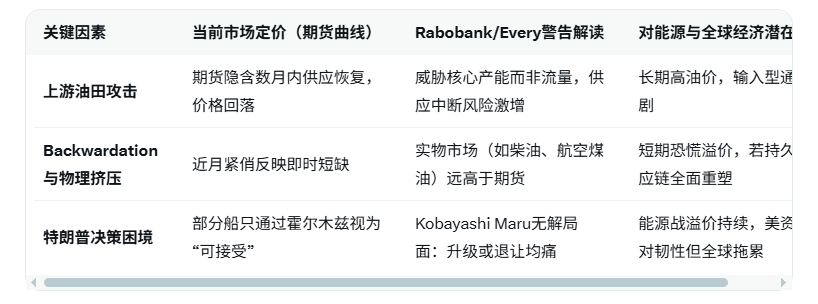

According to APP, Rabobank Senior Global Strategist Michael Every pointed out that with the escalation of conflicts between Iran, Israel, and regional powers, energy supplies face structural threats, shifting from simple flow disruptions to direct attacks on upstream oil fields (such as Iran targeting facilities at the Shah gas field in the UAE). Despite backwardation (near-month contract prices exceeding far-month prices, reflecting the current physical squeeze) and tight physical supply, the futures curve is still pricing in a decline in energy prices over the next few months, suggesting that investors generally expect no long-term disruption to regional energy flows. Even so, Rabobank warns that the situation could easily deteriorate significantly; currently, the media is calling this an "Operation Epic Folly," with physical market prices (such as marine fuel, jet fuel, and diesel) far exceeding futures prices, indicating a severe physical squeeze.

Every further analyzes that the current problem lies in whether President Trump is caught in a "Kobayashi Maru" dilemma: if the attack intensifies, the energy market could face further panic. Israeli media reports that the country is prepared to fight Iran and Hezbollah in Lebanon for at least a month, rather than the previously expected three weeks; Iran has shifted its focus to upstream oil and gas fields rather than just refineries and export terminals, directly threatening supply rather than flow. Every emphasizes that although US Treasury Secretary Bessent stated that there was "no problem" with the successful passage of ships from Iran, major Asian powers, and India through the Strait of Hormuz, this does not change the risk skew: while US assets have not collapsed significantly (which the market sees as a harbinger of a "1956-style failure"), a global energy premium is underway.

The conflict has driven significant oil price volatility: Brent crude recently broke through $ 100 per barrel, and WTI futures also exceeded $ 100 , a rise of over 40% (since the outbreak of the conflict). The obstruction of the Strait of Hormuz has exacerbated supply concerns. Despite some OPEC+ production increases, the direct attacks and strait closure have made it difficult for the market to quickly compensate. Rabobank believes that futures pricing of "cheaper energy" reflects an optimistic assumption (a quick end to the conflict), but Every warns that this underestimates the uncertainty that the conflict could prolong.

Overall, the energy market is embedded with geopolitical premiums , but the futures curve is still speculating on a short-term solution, ignoring the structural shift in Iran's move towards upstream attacks. If the conflict prolongs, oil prices could surge further to the $110-$ 120 range, amplifying global inflationary pressures, suppressing growth, and delaying interest rate cuts by major central banks. Rabobank warns that current pricing may severely underestimate the risks, and investors should be wary of the cascading impacts of geopolitical escalation on commodities, equity markets, and bond markets.

Editor's Summary:

Rabobank strategist Every emphasized that the Iranian conflict has shifted from a flow-based threat to a core supply threat. While futures pricing for cheaper energy in the coming months reflects market optimism, backwardation and physical pressures indicate immediate tensions. Trump's policy faces a Kobayashi Maru dilemma, the situation is prone to deterioration, and the energy premium is reshaping global inflation and growth expectations.

Frequently Asked Questions

1. Why does Michael Every say that the energy market is underestimating the conflict with Iran?

Every points out that the conflict has shifted from targeting refineries/export terminals to direct attacks on upstream oil fields (such as Iran targeting Shah in the UAE), threatening core capacity rather than just transportation flows. The futures curve is still pricing in a price pullback within months, reflecting market bets on a temporary end to the conflict, but Rabobank warns of severe physical backwardation , with physical market prices far exceeding futures prices, indicating an underestimation of the possibility of a prolonged disruption.

2. What is the meaning of "backwardation" in this context?

Backwardation refers to the fact that near-month contract prices are higher than far-month prices, reflecting current tight supply and physical constraints (such as the Hormuz blockade or facility attacks causing immediate shortages). Every emphasizes that this should have warned of long-term risks, but futures still anticipate cheaper energy in the future, suggesting that the market does not believe there will be lasting supply disruptions, contrasting with high prices in the physical market (such as diesel and jet fuel).

3. What exactly does Trump's "Kobayashi Maru" dilemma refer to?

If Trump continues to escalate attacks on Iran, Israel is prepared to extend the conflict (for at least a month), potentially causing further panic in the energy market and a surge in oil prices. Conversely, if Israel backs down or seeks a ceasefire, it could be seen as a sign of weakness, and Iran may continue to exert pressure. Every believes that either choice is painful; while the US has strong self-sufficiency, the global energy premium will amplify inflation and uncertainty.

4. How significant is the impact of Iran's shift to attacking upstream oil fields on global energy supply?

Traditional attacks focus on flow (such as the Strait of Hormuz), but damage to upstream oil fields (such as Shah) will directly reduce production capacity, with repairs taking months or even longer. Every warns that this changes the nature of the risk: it's not a temporary disruption, but a structural supply loss. If the conflict persists, increased OPEC+ production will be insufficient to compensate, and oil prices could break through $ 110 , pushing up global imported inflation and dragging down economic growth.

5. How does the current divergence between energy market pricing and Rabobank's views affect investors?

Futures trading implies a short-term solution (without long-term disruption), but Every believes this is "wishful thinking"—US Treasury Secretary Bessent's statement that there are "no problems" with some ships passing through the Strait of Hormuz has not changed the risk skew. Investors who follow the optimistic outlook of futures trading may underestimate the risks of inflationary shocks and central bank tightening; conversely, to be wary of a protracted conflict, they can proactively position themselves in defensive assets (such as energy stocks and inflation-linked bonds). Close monitoring of oil prices, the developments at the Strait of Hormuz, and Trump's statements is necessary to determine the sustainability of the premium .

Every further analyzes that the current problem lies in whether President Trump is caught in a "Kobayashi Maru" dilemma: if the attack intensifies, the energy market could face further panic. Israeli media reports that the country is prepared to fight Iran and Hezbollah in Lebanon for at least a month, rather than the previously expected three weeks; Iran has shifted its focus to upstream oil and gas fields rather than just refineries and export terminals, directly threatening supply rather than flow. Every emphasizes that although US Treasury Secretary Bessent stated that there was "no problem" with the successful passage of ships from Iran, major Asian powers, and India through the Strait of Hormuz, this does not change the risk skew: while US assets have not collapsed significantly (which the market sees as a harbinger of a "1956-style failure"), a global energy premium is underway.

The conflict has driven significant oil price volatility: Brent crude recently broke through $ 100 per barrel, and WTI futures also exceeded $ 100 , a rise of over 40% (since the outbreak of the conflict). The obstruction of the Strait of Hormuz has exacerbated supply concerns. Despite some OPEC+ production increases, the direct attacks and strait closure have made it difficult for the market to quickly compensate. Rabobank believes that futures pricing of "cheaper energy" reflects an optimistic assumption (a quick end to the conflict), but Every warns that this underestimates the uncertainty that the conflict could prolong.

Overall, the energy market is embedded with geopolitical premiums , but the futures curve is still speculating on a short-term solution, ignoring the structural shift in Iran's move towards upstream attacks. If the conflict prolongs, oil prices could surge further to the $110-$ 120 range, amplifying global inflationary pressures, suppressing growth, and delaying interest rate cuts by major central banks. Rabobank warns that current pricing may severely underestimate the risks, and investors should be wary of the cascading impacts of geopolitical escalation on commodities, equity markets, and bond markets.

Editor's Summary:

Rabobank strategist Every emphasized that the Iranian conflict has shifted from a flow-based threat to a core supply threat. While futures pricing for cheaper energy in the coming months reflects market optimism, backwardation and physical pressures indicate immediate tensions. Trump's policy faces a Kobayashi Maru dilemma, the situation is prone to deterioration, and the energy premium is reshaping global inflation and growth expectations.

Frequently Asked Questions

1. Why does Michael Every say that the energy market is underestimating the conflict with Iran?

Every points out that the conflict has shifted from targeting refineries/export terminals to direct attacks on upstream oil fields (such as Iran targeting Shah in the UAE), threatening core capacity rather than just transportation flows. The futures curve is still pricing in a price pullback within months, reflecting market bets on a temporary end to the conflict, but Rabobank warns of severe physical backwardation , with physical market prices far exceeding futures prices, indicating an underestimation of the possibility of a prolonged disruption.

2. What is the meaning of "backwardation" in this context?

Backwardation refers to the fact that near-month contract prices are higher than far-month prices, reflecting current tight supply and physical constraints (such as the Hormuz blockade or facility attacks causing immediate shortages). Every emphasizes that this should have warned of long-term risks, but futures still anticipate cheaper energy in the future, suggesting that the market does not believe there will be lasting supply disruptions, contrasting with high prices in the physical market (such as diesel and jet fuel).

3. What exactly does Trump's "Kobayashi Maru" dilemma refer to?

If Trump continues to escalate attacks on Iran, Israel is prepared to extend the conflict (for at least a month), potentially causing further panic in the energy market and a surge in oil prices. Conversely, if Israel backs down or seeks a ceasefire, it could be seen as a sign of weakness, and Iran may continue to exert pressure. Every believes that either choice is painful; while the US has strong self-sufficiency, the global energy premium will amplify inflation and uncertainty.

4. How significant is the impact of Iran's shift to attacking upstream oil fields on global energy supply?

Traditional attacks focus on flow (such as the Strait of Hormuz), but damage to upstream oil fields (such as Shah) will directly reduce production capacity, with repairs taking months or even longer. Every warns that this changes the nature of the risk: it's not a temporary disruption, but a structural supply loss. If the conflict persists, increased OPEC+ production will be insufficient to compensate, and oil prices could break through $ 110 , pushing up global imported inflation and dragging down economic growth.

5. How does the current divergence between energy market pricing and Rabobank's views affect investors?

Futures trading implies a short-term solution (without long-term disruption), but Every believes this is "wishful thinking"—US Treasury Secretary Bessent's statement that there are "no problems" with some ships passing through the Strait of Hormuz has not changed the risk skew. Investors who follow the optimistic outlook of futures trading may underestimate the risks of inflationary shocks and central bank tightening; conversely, to be wary of a protracted conflict, they can proactively position themselves in defensive assets (such as energy stocks and inflation-linked bonds). Close monitoring of oil prices, the developments at the Strait of Hormuz, and Trump's statements is necessary to determine the sustainability of the premium .

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.