One chart: The Baltic Dry Index strengthens, with Capesize and Panamax vessel freight rates leading the gains.

2026-03-18 23:39:05

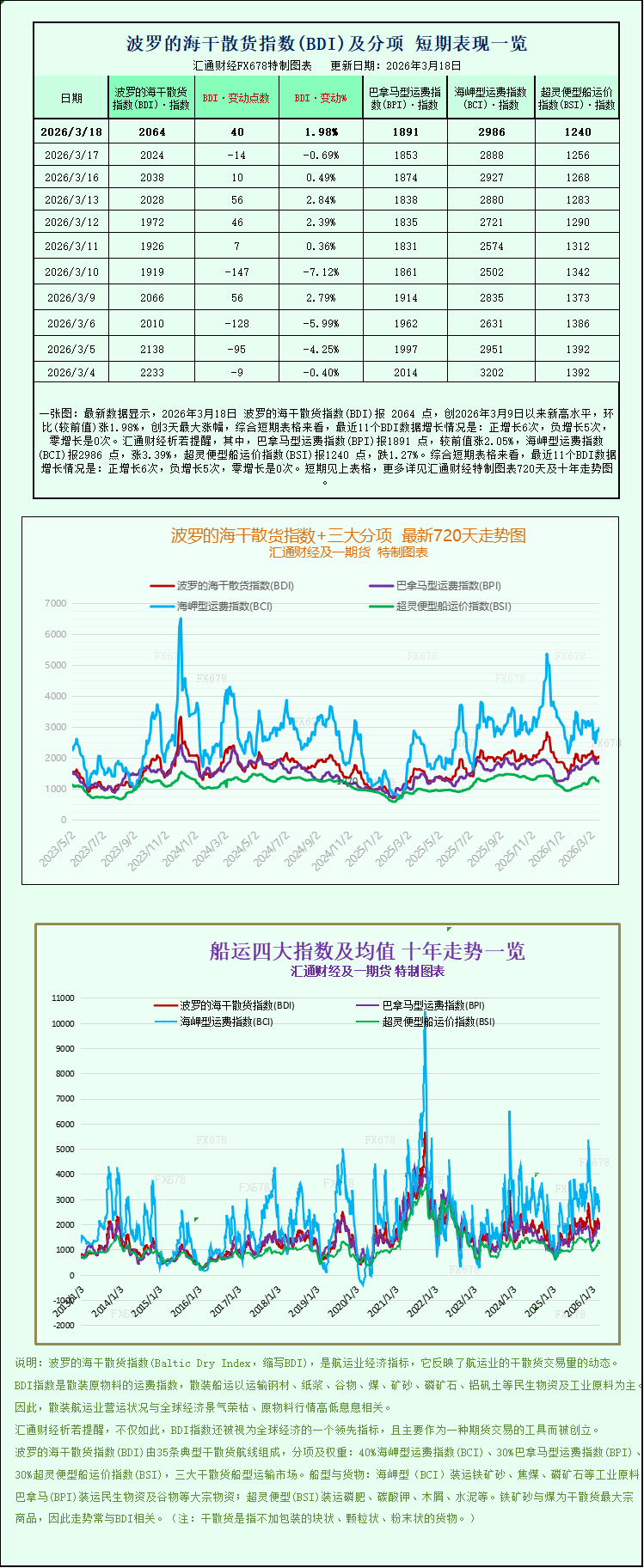

Latest data shows that the Baltic Dry Index (BDI) reached 2064 points on March 18, 2026, a new high since March 9, 2026, up 1.98% month-on-month, marking the largest increase in three days. Looking at the short-term charts, the BDI has seen positive growth 6 times, negative growth 5 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 1891 points, up 2.05% from the previous value; the Capesize Freight Index (BCI) was 2986 points, up 3.39%; and the Supramax Freight Index (BSI) was 1240 points, down 1.27%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI) strengthened: Capesize and Panamax vessel freight rates led the gains, influenced by a combination of market supply and demand factors and external influences.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index saw a significant increase on Wednesday. This surge was primarily driven by strong rises in Capesize and Panamax vessel freight rates, directly reflecting changes in the local supply and demand dynamics of the dry bulk shipping market and mirroring the real-time dynamics of commodity trade and global shipping demand. As an authoritative indicator of the global dry bulk shipping industry, this index specifically monitors freight rates for ocean-going vessels transporting bulk commodities such as iron ore, coal, and grains. Its fluctuations directly impact global commodity trade costs and the profitability of shipping companies.

Overall performance of core indices: Up nearly 2%, firmly above the 2000-point mark.

The Baltic Dry Index (BDI), which encompasses the three major dry bulk carrier types—Capemax, Panamax, and Supramax—rose sharply by 40 points on the day, with an overall increase approaching 2%, ultimately closing at 2064 points. This successfully broke through the key psychological barrier of 2000 points, signaling a phased recovery in the dry bulk shipping market. Looking at individual vessel types, the three main types showed divergent trends. Capemax and Panamax vessels were the core drivers of this upward movement, while Supramax vessels experienced a slight pullback, exhibiting a "polarized" market characteristic.

Capesize vessels: Freight rates surge, leading to a significant increase in daily profits.

As the "giants" of the dry bulk shipping market, Capesize vessels mainly carry ultra-large dry bulk cargoes such as iron ore and coal, with a single cargo capacity of up to 150,000 tons. They are the core carriers for global bulk industrial raw material transportation, and their freight rates are highly correlated with global steel and energy trade. On that day, the Capesize index performed the best, surging 98 points, a gain of 3.4%, to close at 2986 points.

Along with rising freight rates, the profitability of Capesize vessels has also increased, with average daily operating revenue rising by $883 and daily profit exceeding $23,000, reaching $23,574. This data indicates a significant improvement in the short-term profitability of shipping companies operating Capesize vessels, and also reflects a phased recovery in global demand for iron ore and coal ocean shipping, with tight supply and demand of shipping capacity supporting higher freight rates.

Panamax vessels: Steady growth, with demand for grain and coal transportation providing a safety net.

Panamax vessels are the backbone of the dry bulk shipping market. Their size is adapted to the navigation conditions of the Panama Canal, and they primarily transport 60,000 to 70,000 tons of bulk commodities such as coal, grain, and food, covering core global energy and agricultural trade routes. The Panamax index rose in tandem with the Panamax index, gaining 38 points, or 2.1%, to close at 1891 points.

In terms of profitability, Panamax vessels saw an average daily revenue increase of $342, with daily profits rising to $17,016. The approaching peak season for global agricultural trade and a recovery in demand for cross-regional coal transportation were the core factors supporting the rise in Panamax vessel freight rates and earnings. This, coupled with a slowdown in capacity deployment, further boosted the market for this vessel type.

Supramax vessels: Slight pullback, market performance remains weak.

Unlike the strong performance of the first two ship types, the Very Large Bulk Carrier (Supramax) index declined slightly on the day, falling 16 points, or 1.3%, to close at 1240 points. This ship type mainly carries small-volume dry bulk cargoes, building materials, and other goods, and is more affected by regional trade fluctuations and changes in short-haul transportation demand. This round of correction also reflects the differentiated demand pattern among different cargo types and routes within the dry bulk market.

Related Impacts: Iron ore futures are under pressure; geopolitical tensions disrupt shipping safety.

The rise in shipping freight rates has also had a reverse impact on the commodity market. Affected by the increase in Capesize vessel freight rates, the cost of ocean shipping of iron ore has risen, which has hindered the pace of global steel exports to some extent. In addition, domestic steel mills are constrained by high energy costs and are maintaining firm ex-factory prices for steel products, which has further suppressed the demand for iron ore. Under the combined effect of multiple factors, iron ore futures prices fell in response.

Meanwhile, geopolitical risks are adding uncertainty to the global shipping market. The US military issued a statement on Tuesday saying it had used high-explosive bunker busters to strike targets off the coast of Iran near the Strait of Hormuz, claiming that Iranian anti-ship missiles pose a direct threat to the security of international shipping lanes. As a crucial chokepoint for global energy transport, the heightened geopolitical tensions in the Strait of Hormuz could disrupt global shipping routes, increase hedging costs, and potentially have a ripple effect on the dry bulk and tanker shipping markets.

The Baltic Dry Index (BDI) strengthened: Capesize and Panamax vessel freight rates led the gains, influenced by a combination of market supply and demand factors and external influences.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index saw a significant increase on Wednesday. This surge was primarily driven by strong rises in Capesize and Panamax vessel freight rates, directly reflecting changes in the local supply and demand dynamics of the dry bulk shipping market and mirroring the real-time dynamics of commodity trade and global shipping demand. As an authoritative indicator of the global dry bulk shipping industry, this index specifically monitors freight rates for ocean-going vessels transporting bulk commodities such as iron ore, coal, and grains. Its fluctuations directly impact global commodity trade costs and the profitability of shipping companies.

Overall performance of core indices: Up nearly 2%, firmly above the 2000-point mark.

The Baltic Dry Index (BDI), which encompasses the three major dry bulk carrier types—Capemax, Panamax, and Supramax—rose sharply by 40 points on the day, with an overall increase approaching 2%, ultimately closing at 2064 points. This successfully broke through the key psychological barrier of 2000 points, signaling a phased recovery in the dry bulk shipping market. Looking at individual vessel types, the three main types showed divergent trends. Capemax and Panamax vessels were the core drivers of this upward movement, while Supramax vessels experienced a slight pullback, exhibiting a "polarized" market characteristic.

Capesize vessels: Freight rates surge, leading to a significant increase in daily profits.

As the "giants" of the dry bulk shipping market, Capesize vessels mainly carry ultra-large dry bulk cargoes such as iron ore and coal, with a single cargo capacity of up to 150,000 tons. They are the core carriers for global bulk industrial raw material transportation, and their freight rates are highly correlated with global steel and energy trade. On that day, the Capesize index performed the best, surging 98 points, a gain of 3.4%, to close at 2986 points.

Along with rising freight rates, the profitability of Capesize vessels has also increased, with average daily operating revenue rising by $883 and daily profit exceeding $23,000, reaching $23,574. This data indicates a significant improvement in the short-term profitability of shipping companies operating Capesize vessels, and also reflects a phased recovery in global demand for iron ore and coal ocean shipping, with tight supply and demand of shipping capacity supporting higher freight rates.

Panamax vessels: Steady growth, with demand for grain and coal transportation providing a safety net.

Panamax vessels are the backbone of the dry bulk shipping market. Their size is adapted to the navigation conditions of the Panama Canal, and they primarily transport 60,000 to 70,000 tons of bulk commodities such as coal, grain, and food, covering core global energy and agricultural trade routes. The Panamax index rose in tandem with the Panamax index, gaining 38 points, or 2.1%, to close at 1891 points.

In terms of profitability, Panamax vessels saw an average daily revenue increase of $342, with daily profits rising to $17,016. The approaching peak season for global agricultural trade and a recovery in demand for cross-regional coal transportation were the core factors supporting the rise in Panamax vessel freight rates and earnings. This, coupled with a slowdown in capacity deployment, further boosted the market for this vessel type.

Supramax vessels: Slight pullback, market performance remains weak.

Unlike the strong performance of the first two ship types, the Very Large Bulk Carrier (Supramax) index declined slightly on the day, falling 16 points, or 1.3%, to close at 1240 points. This ship type mainly carries small-volume dry bulk cargoes, building materials, and other goods, and is more affected by regional trade fluctuations and changes in short-haul transportation demand. This round of correction also reflects the differentiated demand pattern among different cargo types and routes within the dry bulk market.

Related Impacts: Iron ore futures are under pressure; geopolitical tensions disrupt shipping safety.

The rise in shipping freight rates has also had a reverse impact on the commodity market. Affected by the increase in Capesize vessel freight rates, the cost of ocean shipping of iron ore has risen, which has hindered the pace of global steel exports to some extent. In addition, domestic steel mills are constrained by high energy costs and are maintaining firm ex-factory prices for steel products, which has further suppressed the demand for iron ore. Under the combined effect of multiple factors, iron ore futures prices fell in response.

Meanwhile, geopolitical risks are adding uncertainty to the global shipping market. The US military issued a statement on Tuesday saying it had used high-explosive bunker busters to strike targets off the coast of Iran near the Strait of Hormuz, claiming that Iranian anti-ship missiles pose a direct threat to the security of international shipping lanes. As a crucial chokepoint for global energy transport, the heightened geopolitical tensions in the Strait of Hormuz could disrupt global shipping routes, increase hedging costs, and potentially have a ripple effect on the dry bulk and tanker shipping markets.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.