A chart shows the Baltic Dry Index fell slightly, with declines in the Capesize and Supramax bulk carrier sectors.

2026-03-19 23:04:26

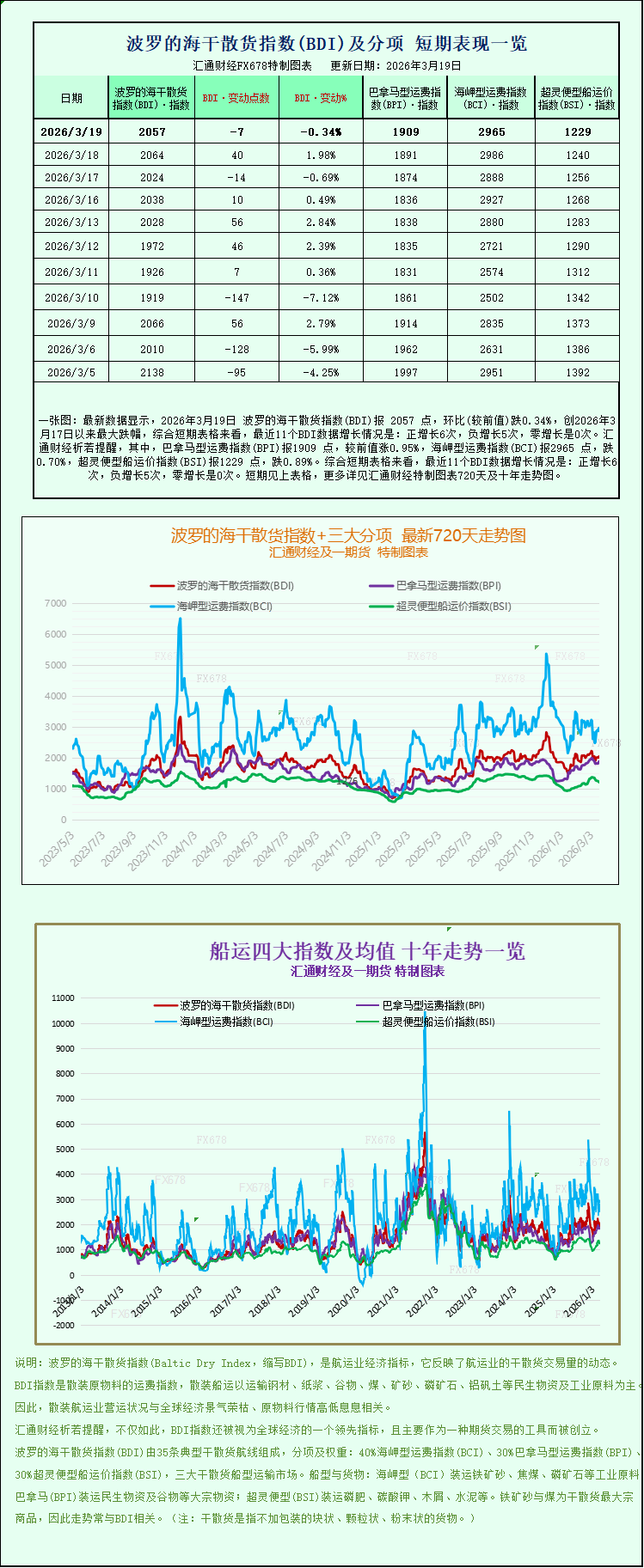

The latest data shows that on March 19, 2026, the Baltic Dry Index (BDI) was 2057 points, a decrease of 0.34% compared to the previous period, marking the largest drop since March 17, 2026. Looking at the short-term charts, the BDI has seen positive growth 6 times, negative growth 5 times, and zero growth in the last 11 BDI readings. Specifically, the Panamax Freight Index (BPI) was 1909 points, up 0.95% from the previous period; the Capesize Freight Index (BCI) was 2965 points, down 0.70%; and the Supramax Freight Index (BSI) was 1229 points, down 0.89%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index, a key indicator of global dry bulk shipping market trends, declined slightly on Thursday. As a crucial measure of freight rates for vessels transporting dry bulk commodities globally, the index showed a divergent trend on the day: the Panamax sector bucked the trend and recorded a slight increase, but this was insufficient to offset the slight declines in the Capesize and Supramax sectors, the two main vessel types, ultimately leading to an overall decline in the index.

As the core index for comprehensively monitoring freight rates of the three major dry bulk carrier types—Capesize, Panamax, and Supramax—the Baltic Dry Index (BDI) fell 7 points on the day, with an overall decline of 0.3%, finally closing at 2057 points. It continued to fluctuate narrowly around the 2000-point mark, reflecting the current situation in the dry bulk shipping market where the battle between bulls and bears has intensified and the overall trend lacks a clear direction.

The Capesize shipping sector weakened, with freight rates and daily revenue declining in tandem.

Detailed ship type data shows that the Capesize index, which has the largest market share and is most sensitive to commodity demand, performed weakly on the day, falling 21 points, or 0.7%, to close at 2965 points. Capesize vessels, as the mainstay of the dry bulk shipping market, typically carry 150,000 tons of bulk dry cargo, primarily transporting commodities such as iron ore and coal, which are essential for global industrial production. Their freight rates directly reflect the state of global manufacturing and infrastructure demand.

Driven by the decline in the index, the average daily operating revenue of Capesize vessels also fell, decreasing by $185 in a single day to $23,389. Industry analysts pointed out that the decline in revenue for this vessel type is directly related to recent fluctuations in the global iron ore spot market and a slowdown in coal procurement in some regions. The moderate weakening of end-user demand has been transmitted to the shipping sector, suppressing the upward potential of freight rates.

The commodity market also released weak signals. The tight supply situation eased somewhat due to news that Chinese state-owned buyers relaxed restrictions on some iron ore purchases. Coupled with weak restocking intentions from downstream steel mills, global iron ore futures prices fell slightly on the day, further dragging down bullish sentiment in the Capesize shipping market.

Panamax vessel sector bucks the trend and rebounds with both freight rates and revenue rising.

In contrast to Capesize vessels, the Panamax sector was the only bright spot in the market that day. The index for this sector bucked the trend, rising 18 points, or nearly 1%, to close at 1909 points, demonstrating independent strength. Panamax vessels primarily carry medium-sized dry bulk cargo of 60,000 to 70,000 tons, mainly transporting coal, grain, and food products. Their market performance is more influenced by global food trade and regional energy restocking demand.

Rising freight rates directly boosted vessel operating profits, with Panamax vessels seeing an average daily revenue increase of $161 to $17,177. Fearnleys, a leading global ship brokerage firm, stated in its latest weekly market report released Wednesday: "This week, the Panamax market broke free from its previous volatile trend, exhibiting a more stable and positive operating pattern. Increased regional cargo replenishment and transoceanic trade routes are the core drivers supporting this sector's recovery."

The Supramax ship sector continued to decline due to weak overall market fundamentals.

Focusing on the small and medium-sized dry bulk carrier market, the Supramax index continued its decline, falling 11 points, or 0.9%, to close at 1229 points. This type of vessel mainly transports small-volume bulk cargo, building materials, and industrial raw materials. Affected by the slow pace of global supply chain recovery and insufficient supply of scattered cargo, it has been operating in a weak range recently.

Regarding the overall market outlook, Fearnleys Brokerage further added its perspective in the report: "Looking at the current dry bulk shipping market as a whole, the core fundamentals remain weak. Neither the demand side for commodities nor the global supply side of shipping capacity has emerged in the short term as there are any positive factors that can drive a strong market recovery. It is expected that the market will continue to maintain a weak and volatile pattern in the short term."

Geopolitical risks disrupt shipping markets, but regional freight rates remain supported.

It is worth noting that although overall dry bulk freight rates are weak, the shipping risks brought about by global geopolitical conflicts continue to escalate. The escalating conflict in the Middle East has put pressure on the stability of navigation in the Strait of Hormuz, the world's most important oil transport chokepoint. Some shipping routes have been forced to adjust, leading to increased vessel operating costs and insurance premiums. This has not only pushed up oil transport prices but also provided some support for overall global dry bulk shipping rates, offsetting some of the decline caused by weakening demand.

The Baltic Dry Index, a key indicator of global dry bulk shipping market trends, declined slightly on Thursday. As a crucial measure of freight rates for vessels transporting dry bulk commodities globally, the index showed a divergent trend on the day: the Panamax sector bucked the trend and recorded a slight increase, but this was insufficient to offset the slight declines in the Capesize and Supramax sectors, the two main vessel types, ultimately leading to an overall decline in the index.

As the core index for comprehensively monitoring freight rates of the three major dry bulk carrier types—Capesize, Panamax, and Supramax—the Baltic Dry Index (BDI) fell 7 points on the day, with an overall decline of 0.3%, finally closing at 2057 points. It continued to fluctuate narrowly around the 2000-point mark, reflecting the current situation in the dry bulk shipping market where the battle between bulls and bears has intensified and the overall trend lacks a clear direction.

The Capesize shipping sector weakened, with freight rates and daily revenue declining in tandem.

Detailed ship type data shows that the Capesize index, which has the largest market share and is most sensitive to commodity demand, performed weakly on the day, falling 21 points, or 0.7%, to close at 2965 points. Capesize vessels, as the mainstay of the dry bulk shipping market, typically carry 150,000 tons of bulk dry cargo, primarily transporting commodities such as iron ore and coal, which are essential for global industrial production. Their freight rates directly reflect the state of global manufacturing and infrastructure demand.

Driven by the decline in the index, the average daily operating revenue of Capesize vessels also fell, decreasing by $185 in a single day to $23,389. Industry analysts pointed out that the decline in revenue for this vessel type is directly related to recent fluctuations in the global iron ore spot market and a slowdown in coal procurement in some regions. The moderate weakening of end-user demand has been transmitted to the shipping sector, suppressing the upward potential of freight rates.

The commodity market also released weak signals. The tight supply situation eased somewhat due to news that Chinese state-owned buyers relaxed restrictions on some iron ore purchases. Coupled with weak restocking intentions from downstream steel mills, global iron ore futures prices fell slightly on the day, further dragging down bullish sentiment in the Capesize shipping market.

Panamax vessel sector bucks the trend and rebounds with both freight rates and revenue rising.

In contrast to Capesize vessels, the Panamax sector was the only bright spot in the market that day. The index for this sector bucked the trend, rising 18 points, or nearly 1%, to close at 1909 points, demonstrating independent strength. Panamax vessels primarily carry medium-sized dry bulk cargo of 60,000 to 70,000 tons, mainly transporting coal, grain, and food products. Their market performance is more influenced by global food trade and regional energy restocking demand.

Rising freight rates directly boosted vessel operating profits, with Panamax vessels seeing an average daily revenue increase of $161 to $17,177. Fearnleys, a leading global ship brokerage firm, stated in its latest weekly market report released Wednesday: "This week, the Panamax market broke free from its previous volatile trend, exhibiting a more stable and positive operating pattern. Increased regional cargo replenishment and transoceanic trade routes are the core drivers supporting this sector's recovery."

The Supramax ship sector continued to decline due to weak overall market fundamentals.

Focusing on the small and medium-sized dry bulk carrier market, the Supramax index continued its decline, falling 11 points, or 0.9%, to close at 1229 points. This type of vessel mainly transports small-volume bulk cargo, building materials, and industrial raw materials. Affected by the slow pace of global supply chain recovery and insufficient supply of scattered cargo, it has been operating in a weak range recently.

Regarding the overall market outlook, Fearnleys Brokerage further added its perspective in the report: "Looking at the current dry bulk shipping market as a whole, the core fundamentals remain weak. Neither the demand side for commodities nor the global supply side of shipping capacity has emerged in the short term as there are any positive factors that can drive a strong market recovery. It is expected that the market will continue to maintain a weak and volatile pattern in the short term."

Geopolitical risks disrupt shipping markets, but regional freight rates remain supported.

It is worth noting that although overall dry bulk freight rates are weak, the shipping risks brought about by global geopolitical conflicts continue to escalate. The escalating conflict in the Middle East has put pressure on the stability of navigation in the Strait of Hormuz, the world's most important oil transport chokepoint. Some shipping routes have been forced to adjust, leading to increased vessel operating costs and insurance premiums. This has not only pushed up oil transport prices but also provided some support for overall global dry bulk shipping rates, offsetting some of the decline caused by weakening demand.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.