The war hasn't ended, but gold and oil prices have already plummeted. Is the market going to cease trading or reverse course to pick up new buyers?

2026-03-19 21:38:07

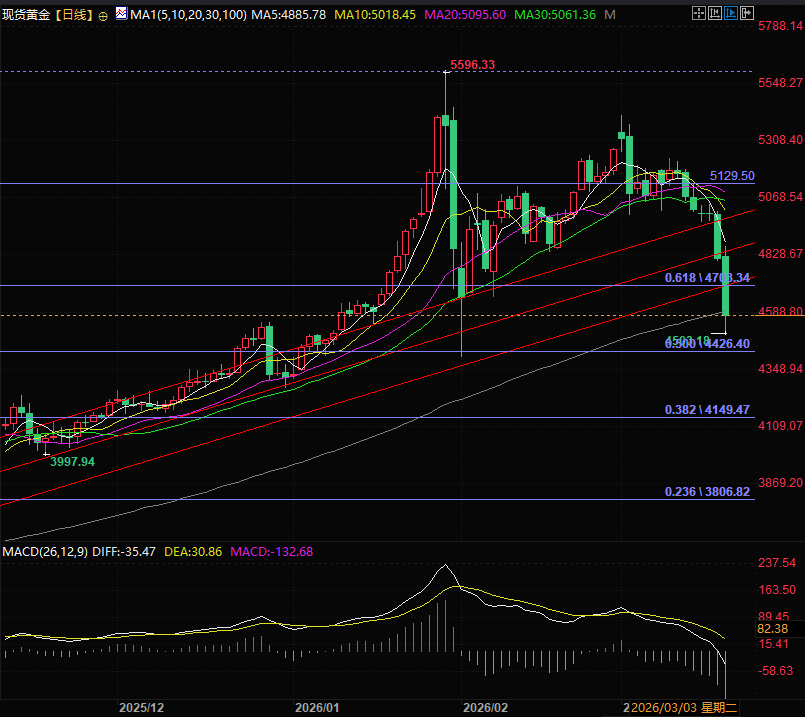

On Thursday (March 19), spot gold prices fell sharply during the European and American trading sessions. The recent continuous decline in gold prices triggered panic selling and leveraged liquidation. It is currently trading around 4533, down -5.98%.

Although geopolitical competition in the Middle East has not stopped recently, the trend of "all parties working together to de-escalate tensions" has gradually become clear.

As a key participant, Iran is facing a complex situation involving multiple fronts: the offensive and defensive battle between Hezbollah and Israel in southern Lebanon continues, with the Israeli army slowly advancing and "systematically destroying" border towns, while Hezbollah destroys several Israeli tanks through ambush tactics, and the stalemate between the two sides remains unchanged.

Multiple explosions occurred near Erbil Airport in Iraq, an area considered a sensitive zone for US and coalition forces, highlighting potential geopolitical risks in the Middle East.

Meanwhile, Iran itself faces direct military pressure, with the US military continuing to strike missile and drone-related capabilities in Iraq and cracking down on pro-Iranian militia groups within Iraq.

To prevent the conflict from escalating further, countries have launched intensive mediation efforts.

The United States has made it clear that it does not want to get bogged down in a protracted war. Defense Secretary Hergsays denied involvement in a "perpetual war" with Iran, emphasizing that the U.S. military's objectives (destroying Iranian missile launchers, defense industrial bases, etc.) are clear and progressing according to plan. Although there is no clear timetable for withdrawal, the U.S. has no intention of engaging in a protracted conflict.

More significantly, the U.S. Treasury Department sent a major conciliatory signal: Treasury Secretary Scott Bessant announced that sanctions on 140 million barrels of Iranian crude oil stranded at sea may be lifted in the coming days, and Iranian oil will be allowed to continue to be transported through the Gulf region. This move aims to increase global crude oil supply, stabilize oil prices, and indirectly ease the confrontation with Iran.

Other countries also actively participated in the mediation: British Prime Minister Starmer strongly condemned Iran's attack on Qatari gas facilities and called for an end to the conflict as soon as possible to reduce the cost of living;

French President Macron called on all parties to halt the attacks, despite criticism from Iranian Foreign Minister Araqchi (who accused him of ignoring previous attacks by the US and Israel), but diplomatic communication channels remain open;

Oman's Foreign Minister Badr Albusaydi directly accused Israel of being the culprit in the conflict and called for the resumption of negotiations to resolve the dispute.

The easing of tensions in the Middle East directly triggered a decline in market risk aversion, leading to a pullback in the US dollar index.

Generally speaking, a weaker dollar would provide support for gold, but this time gold prices have bucked the trend and come under pressure. The core logic is that as the United States is on the side of the war, the decline in safe-haven demand is negative for the dollar and also negative for gold.

The safe-haven buying of the US dollar, previously fueled by the Middle East conflict, has continued to decline. The benefits brought by the dollar's pullback have been completely offset by the waning safe-haven demand, leaving gold in a unique situation where it is "difficult to rise even with a weak dollar."

The Federal Reserve's policy direction has become a key variable suppressing gold prices.

Recently, the Federal Reserve has not only kept interest rates unchanged, but also raised its 2026 year-end PCE inflation forecast for the United States from 2.4% to 2.7%, while continuing to advance the balance sheet reduction process and optimizing the balance sheet structure through structural tightening.

This combination of "quantitative tightening + rising inflation expectations" directly pushed up and maintained the high level of US Treasury yields: quantitative tightening leads to a long-term tightening of market liquidity, pushing up risk-free interest rates;

Upward revisions to inflation expectations have exacerbated market concerns about the Federal Reserve maintaining high interest rates, further enhancing the attractiveness of US Treasuries. Meanwhile, gold, as a non-interest-bearing asset, has seen its valuation advantage significantly diminished in an environment of high US Treasury yields.

However, although US Treasury yields are currently at high levels, they are showing signs of rising and then falling back, which suggests that gold is likely to rebound.

(Daily chart of 10-year US Treasury yield, source: EasyTrade)

The decline in crude oil supply risks should have weakened expectations of rising inflation, but as Brent crude oil prices surged and then fell back, US Treasury yields did not decline, and gold did not rebound, suggesting that there may be mispricing of assets.

The United States plans to lift sanctions on Iranian oil, while Iranian lawmakers have proposed imposing tolls on shipping through the Strait of Hormuz, indicating that Iran is beginning to study a mechanism for normalizing its oil supply.

Although shipping conditions cannot be restored to pre-war levels, as the core channel for global crude oil transportation, policy changes directly affect the stability of crude oil supply.

Current market concerns about the supply of Middle Eastern seaborne crude oil have not completely dissipated. This uncertainty continues to push up inflation expectations, which in turn supports the high level of US Treasury yields, putting sustained pressure on gold. However, if efforts to normalize crude oil supply continue, inflation expectations are expected to decline, leading to a rebound in gold prices.

In summary, the triple pressure on gold—cooling safe-haven demand, rising inflation expectations, and high US Treasury yields—was the trigger, while the recent continuous decline that triggered panic selling is likely the direct result.

Easing tensions in the Middle East have dampened safe-haven buying, while Federal Reserve policy and inflation expectations have pushed up US Treasury yields, and uncertainty surrounding oil supply has solidified this trend.

For gold traders, three key marginal variables need to be closely monitored in the short term: whether the Middle East conflict will escalate again, whether the Federal Reserve will signal a policy easing, and whether the shipping policy in the Strait of Hormuz will be implemented. Changes in these factors will be crucial to breaking the current suppressive pattern.

However, in the context of transactions, when faced with such extreme situations, blood-stained chips may be both the most expensive and the cheapest.

(Spot gold daily chart, source: FX678)

At 21:30 Beijing time, spot gold was trading at $4,567 per ounce.

Although geopolitical competition in the Middle East has not stopped recently, the trend of "all parties working together to de-escalate tensions" has gradually become clear.

As a key participant, Iran is facing a complex situation involving multiple fronts: the offensive and defensive battle between Hezbollah and Israel in southern Lebanon continues, with the Israeli army slowly advancing and "systematically destroying" border towns, while Hezbollah destroys several Israeli tanks through ambush tactics, and the stalemate between the two sides remains unchanged.

Multiple explosions occurred near Erbil Airport in Iraq, an area considered a sensitive zone for US and coalition forces, highlighting potential geopolitical risks in the Middle East.

Meanwhile, Iran itself faces direct military pressure, with the US military continuing to strike missile and drone-related capabilities in Iraq and cracking down on pro-Iranian militia groups within Iraq.

Mediation efforts: The US signals its intention to "disengage," and multiple countries work to de-escalate the situation.

To prevent the conflict from escalating further, countries have launched intensive mediation efforts.

The United States has made it clear that it does not want to get bogged down in a protracted war. Defense Secretary Hergsays denied involvement in a "perpetual war" with Iran, emphasizing that the U.S. military's objectives (destroying Iranian missile launchers, defense industrial bases, etc.) are clear and progressing according to plan. Although there is no clear timetable for withdrawal, the U.S. has no intention of engaging in a protracted conflict.

More significantly, the U.S. Treasury Department sent a major conciliatory signal: Treasury Secretary Scott Bessant announced that sanctions on 140 million barrels of Iranian crude oil stranded at sea may be lifted in the coming days, and Iranian oil will be allowed to continue to be transported through the Gulf region. This move aims to increase global crude oil supply, stabilize oil prices, and indirectly ease the confrontation with Iran.

Other countries also actively participated in the mediation: British Prime Minister Starmer strongly condemned Iran's attack on Qatari gas facilities and called for an end to the conflict as soon as possible to reduce the cost of living;

French President Macron called on all parties to halt the attacks, despite criticism from Iranian Foreign Minister Araqchi (who accused him of ignoring previous attacks by the US and Israel), but diplomatic communication channels remain open;

Oman's Foreign Minister Badr Albusaydi directly accused Israel of being the culprit in the conflict and called for the resumption of negotiations to resolve the dispute.

Market Interaction: As risk aversion eases, a dollar pullback fails to rescue gold.

The easing of tensions in the Middle East directly triggered a decline in market risk aversion, leading to a pullback in the US dollar index.

Generally speaking, a weaker dollar would provide support for gold, but this time gold prices have bucked the trend and come under pressure. The core logic is that as the United States is on the side of the war, the decline in safe-haven demand is negative for the dollar and also negative for gold.

The safe-haven buying of the US dollar, previously fueled by the Middle East conflict, has continued to decline. The benefits brought by the dollar's pullback have been completely offset by the waning safe-haven demand, leaving gold in a unique situation where it is "difficult to rise even with a weak dollar."

The Federal Reserve's balance sheet reduction and upward revision of inflation expectations have kept US Treasury yields high.

The Federal Reserve's policy direction has become a key variable suppressing gold prices.

Recently, the Federal Reserve has not only kept interest rates unchanged, but also raised its 2026 year-end PCE inflation forecast for the United States from 2.4% to 2.7%, while continuing to advance the balance sheet reduction process and optimizing the balance sheet structure through structural tightening.

This combination of "quantitative tightening + rising inflation expectations" directly pushed up and maintained the high level of US Treasury yields: quantitative tightening leads to a long-term tightening of market liquidity, pushing up risk-free interest rates;

Upward revisions to inflation expectations have exacerbated market concerns about the Federal Reserve maintaining high interest rates, further enhancing the attractiveness of US Treasuries. Meanwhile, gold, as a non-interest-bearing asset, has seen its valuation advantage significantly diminished in an environment of high US Treasury yields.

However, although US Treasury yields are currently at high levels, they are showing signs of rising and then falling back, which suggests that gold is likely to rebound.

(Daily chart of 10-year US Treasury yield, source: EasyTrade)

Crude oil supply risks have decreased, but who is lying?

The decline in crude oil supply risks should have weakened expectations of rising inflation, but as Brent crude oil prices surged and then fell back, US Treasury yields did not decline, and gold did not rebound, suggesting that there may be mispricing of assets.

The United States plans to lift sanctions on Iranian oil, while Iranian lawmakers have proposed imposing tolls on shipping through the Strait of Hormuz, indicating that Iran is beginning to study a mechanism for normalizing its oil supply.

Although shipping conditions cannot be restored to pre-war levels, as the core channel for global crude oil transportation, policy changes directly affect the stability of crude oil supply.

Current market concerns about the supply of Middle Eastern seaborne crude oil have not completely dissipated. This uncertainty continues to push up inflation expectations, which in turn supports the high level of US Treasury yields, putting sustained pressure on gold. However, if efforts to normalize crude oil supply continue, inflation expectations are expected to decline, leading to a rebound in gold prices.

Summary: Gold is under short-term pressure due to triple resistance; watch for a breakout from marginal variables.

In summary, the triple pressure on gold—cooling safe-haven demand, rising inflation expectations, and high US Treasury yields—was the trigger, while the recent continuous decline that triggered panic selling is likely the direct result.

Easing tensions in the Middle East have dampened safe-haven buying, while Federal Reserve policy and inflation expectations have pushed up US Treasury yields, and uncertainty surrounding oil supply has solidified this trend.

For gold traders, three key marginal variables need to be closely monitored in the short term: whether the Middle East conflict will escalate again, whether the Federal Reserve will signal a policy easing, and whether the shipping policy in the Strait of Hormuz will be implemented. Changes in these factors will be crucial to breaking the current suppressive pattern.

However, in the context of transactions, when faced with such extreme situations, blood-stained chips may be both the most expensive and the cheapest.

(Spot gold daily chart, source: FX678)

At 21:30 Beijing time, spot gold was trading at $4,567 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.