Experts: Institutional investors will enter the market; gold is more attractive in the medium term, while silver faces challenges.

2026-03-30 10:49:56

Gold may face headwinds from high U.S. Treasury yields in the short term, but the underlying reasons for rising yields will make gold more attractive to individual and institutional investors in the medium to long term. Silver, on the other hand, may face greater challenges as the conflict in Iran casts a shadow over economic growth prospects and dampens industrial demand. This is the view of Ryan McIntyre, senior managing partner at Sprott Inc.

Earlier last week, McIntyre reiterated his view that the next wave of large-scale gold investment demand will come from broad institutional buying.

McIntyre said, "I still believe that, overall, this wave of demand has not yet arrived. Obviously, central banks started to take the lead a few years ago. By mid-2024, demand began to shift more towards individual investors, as well as some institutional investors entering through exchange-traded funds (ETFs). Then, at the Jackson Hole meeting in late summer last year, the market began to signal interest rate cuts, which drove gold prices up until the recent conflict with Iran."

Despite a significant pullback in gold prices since the end of January, particularly in the initial weeks following the outbreak of the war with Iran, McIntyre believes that the long-term drivers supporting gold's rise since 2022 have not changed.

McIntyre stated, "From a gold perspective, the only thing that has really changed is opportunity cost, which is typically measured by the yield on U.S. Treasury bonds. There has been some change in that regard, as yields have risen since the start of the conflict, so some people have naturally turned to more liquid instruments, in this case, the U.S. dollar. But in my view, this hasn't changed the fundamental reason why you would include gold in your portfolio."

However, in the short term, the opportunity cost, as measured by U.S. Treasury yields, is enough to deter marginal gold buyers from investing, at least for now.

McIntyre points out: "If you held 10-year Treasury bonds in January, the yield would have risen by 30 to 40 basis points by today. So over that period, the value of your Treasury holdings would have lost about 3% to 4%. Considering that people generally view Treasury bonds as very stable assets, this is a fairly large loss."

He added, "The long-term outlook for our financial conditions has not improved; in fact, it is deteriorating. In all the foreseeable scenarios, governments will likely need to print more money. This will be good for gold and bad for holding bonds. "

Even more perplexing than why investors are hesitant to buy gold in the current environment is why institutional investors didn't initially participate heavily in gold trading after years of significant price increases. McIntyre believes this is primarily due to a lack of institutional expertise and the strong performance of other, more familiar investment tools.

McIntyre said, “I think there are two main reasons why institutions are hesitant. One is that very few institutions have extensive expertise in commodities, and I consider gold a separate asset class. I don’t think people have enough insider expertise in these areas. Some of these institutions didn’t have that knowledge until around the end of 2015, when commodities as a whole experienced a significant correction. As a result, many institutions lost their knowledge in this area, whether they were banks, institutional money managers, or endowments. They essentially liquidated all their commodity and gold positions (if they had any prior exposure). Therefore, they lacked the insider knowledge to make proactive buying decisions.”

He added, "From a professional standpoint, I think it's often easier to 'do nothing' than 'take actual action.' That's definitely part of the reason."

Another major reason why institutional investors haven't turned to gold is that even though gold has outperformed other major asset classes in recent years, they don't need to: their most familiar asset, stocks, has performed exceptionally well during gold's multi-year bull market .

McIntyre said, “Stocks have performed so well that they haven’t been forced to consider other assets. This has been true for most of the time, such as since 2015. I think people will continue to hesitate until the very end, unless they feel forced to make a decision.”

He added, "They will postpone this decision as long as possible, or until typical examples like the S&P 500 no longer work and begin to reverse. I think that could be the factor that forces them to actually take action."

When discussing silver, McIntyre stated that the situation with this grey metal is likely more complex, as its strong industrial demand attributes add a layer of uncertainty to any medium-term forecasts.

McIntyre said, "A silver shortage is still expected this year, meaning demand will exceed supply again, marking the sixth consecutive year. That's the fundamental background. From an industrial demand perspective, when something like this happens, there's obviously a concern about the economic situation and people's willingness and ability to spend, so prices may be under pressure in the short term due to a potential decline in industrial demand."

Regarding investment demand, McIntyre sees two opposing forces. He says, "At least in the short term, we are clearly seeing rising yields, which is negative for silver. But on the other hand, silver also has certain risk diversification and monetary instrument properties, which are positive factors. However, in the case of silver, at least in the short term, the weight of weakening demand and rising interest rates outweighs any safety or diversification benefits that people hope to gain from silver as a monetary instrument ."

McIntyre also agrees that silver is unlikely to regain investor interest unless gold starts to rise significantly again.

He said, "I expect gold to continue to lead the rise in silver prices ."

Overall, Ryan McIntyre believes that despite short-term pressures such as rising yields, gold's long-term fundamentals remain solid, and a wave of large-scale institutional buying is still on the way; while silver needs to wait for gold to regain its upward momentum, while also dealing with additional challenges from a potential decline in industrial demand.

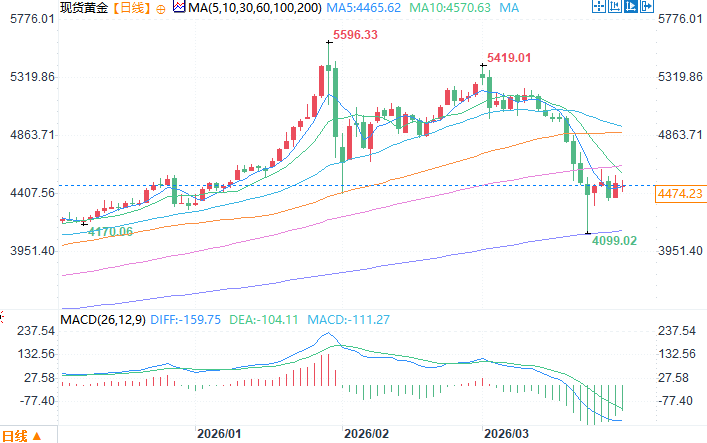

Spot gold daily chart source: EasyForex

At 10:49 AM Beijing time on March 30, spot gold was trading at $4490.23 per ounce.

Earlier last week, McIntyre reiterated his view that the next wave of large-scale gold investment demand will come from broad institutional buying.

McIntyre said, "I still believe that, overall, this wave of demand has not yet arrived. Obviously, central banks started to take the lead a few years ago. By mid-2024, demand began to shift more towards individual investors, as well as some institutional investors entering through exchange-traded funds (ETFs). Then, at the Jackson Hole meeting in late summer last year, the market began to signal interest rate cuts, which drove gold prices up until the recent conflict with Iran."

Despite a significant pullback in gold prices since the end of January, particularly in the initial weeks following the outbreak of the war with Iran, McIntyre believes that the long-term drivers supporting gold's rise since 2022 have not changed.

US Treasury yields pose short-term resistance.

McIntyre stated, "From a gold perspective, the only thing that has really changed is opportunity cost, which is typically measured by the yield on U.S. Treasury bonds. There has been some change in that regard, as yields have risen since the start of the conflict, so some people have naturally turned to more liquid instruments, in this case, the U.S. dollar. But in my view, this hasn't changed the fundamental reason why you would include gold in your portfolio."

However, in the short term, the opportunity cost, as measured by U.S. Treasury yields, is enough to deter marginal gold buyers from investing, at least for now.

McIntyre points out: "If you held 10-year Treasury bonds in January, the yield would have risen by 30 to 40 basis points by today. So over that period, the value of your Treasury holdings would have lost about 3% to 4%. Considering that people generally view Treasury bonds as very stable assets, this is a fairly large loss."

He added, "The long-term outlook for our financial conditions has not improved; in fact, it is deteriorating. In all the foreseeable scenarios, governments will likely need to print more money. This will be good for gold and bad for holding bonds. "

Why have institutions been slow to enter the market on a large scale?

Even more perplexing than why investors are hesitant to buy gold in the current environment is why institutional investors didn't initially participate heavily in gold trading after years of significant price increases. McIntyre believes this is primarily due to a lack of institutional expertise and the strong performance of other, more familiar investment tools.

McIntyre said, “I think there are two main reasons why institutions are hesitant. One is that very few institutions have extensive expertise in commodities, and I consider gold a separate asset class. I don’t think people have enough insider expertise in these areas. Some of these institutions didn’t have that knowledge until around the end of 2015, when commodities as a whole experienced a significant correction. As a result, many institutions lost their knowledge in this area, whether they were banks, institutional money managers, or endowments. They essentially liquidated all their commodity and gold positions (if they had any prior exposure). Therefore, they lacked the insider knowledge to make proactive buying decisions.”

He added, "From a professional standpoint, I think it's often easier to 'do nothing' than 'take actual action.' That's definitely part of the reason."

The strong performance of the stock market has become an institutional obstacle for gold.

Another major reason why institutional investors haven't turned to gold is that even though gold has outperformed other major asset classes in recent years, they don't need to: their most familiar asset, stocks, has performed exceptionally well during gold's multi-year bull market .

McIntyre said, “Stocks have performed so well that they haven’t been forced to consider other assets. This has been true for most of the time, such as since 2015. I think people will continue to hesitate until the very end, unless they feel forced to make a decision.”

He added, "They will postpone this decision as long as possible, or until typical examples like the S&P 500 no longer work and begin to reverse. I think that could be the factor that forces them to actually take action."

Uncertainty in industrial demand further complicates the outlook for silver.

When discussing silver, McIntyre stated that the situation with this grey metal is likely more complex, as its strong industrial demand attributes add a layer of uncertainty to any medium-term forecasts.

McIntyre said, "A silver shortage is still expected this year, meaning demand will exceed supply again, marking the sixth consecutive year. That's the fundamental background. From an industrial demand perspective, when something like this happens, there's obviously a concern about the economic situation and people's willingness and ability to spend, so prices may be under pressure in the short term due to a potential decline in industrial demand."

Regarding investment demand, McIntyre sees two opposing forces. He says, "At least in the short term, we are clearly seeing rising yields, which is negative for silver. But on the other hand, silver also has certain risk diversification and monetary instrument properties, which are positive factors. However, in the case of silver, at least in the short term, the weight of weakening demand and rising interest rates outweighs any safety or diversification benefits that people hope to gain from silver as a monetary instrument ."

McIntyre also agrees that silver is unlikely to regain investor interest unless gold starts to rise significantly again.

He said, "I expect gold to continue to lead the rise in silver prices ."

Overall, Ryan McIntyre believes that despite short-term pressures such as rising yields, gold's long-term fundamentals remain solid, and a wave of large-scale institutional buying is still on the way; while silver needs to wait for gold to regain its upward momentum, while also dealing with additional challenges from a potential decline in industrial demand.

Spot gold daily chart source: EasyForex

At 10:49 AM Beijing time on March 30, spot gold was trading at $4490.23 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.