US stocks are on track for their worst quarterly performance in nearly four years, prompting Wall Street to adopt a cautious and defensive stance.

2026-03-31 11:36:34

2026, a year initially expected to be highly anticipated, was supposed to be a banner year for Wall Street. Accelerated economic growth, the prospect of further interest rate cuts by the Federal Reserve, and the market's gradual digestion of uncertainty stemming from trade disputes led many investors to anticipate double-digit returns in the stock market. However, the conflict with Iran, which began on February 28th, completely altered everything. Soaring energy prices not only fueled inflation expectations but also dramatically increased the risk of a global recession.

U.S. stocks are on track for their worst quarterly performance in nearly four years, with investors quickly shifting from a confident start to a defensive mindset.

At the beginning of 2026, the US stock market showed a relatively positive trend. Although some technology stocks stagnated, funds began to flow into previously neglected market sectors, attracted by low valuations and expectations of economic recovery. However, with the outbreak of conflict in the Middle East, everything came to a standstill.

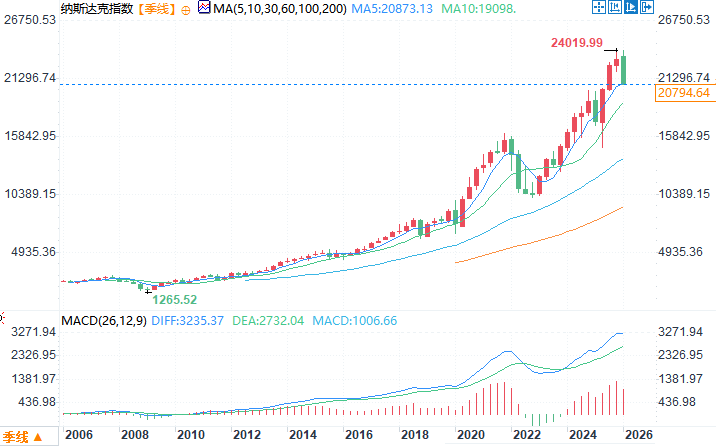

On March 26, the Nasdaq Composite Index, dominated by technology stocks, fell more than 10% from its recent high, officially entering correction territory. A day later, the Dow Jones Industrial Average, a key indicator of the real economy, followed suit. As of now, the S&P 500 has erased all gains from the past seven months. In March, 10 of the S&P 500's 11 sectors declined, with an average drop of 8.3%, the only exception being the energy sector.

"We had the perfect environment to extend the rally, with all the right timing, location, and people, but what happened next put it on hold," said Michael Kantrowitz, chief investment strategist at Piper Sandler.

Since the US and Israel launched military strikes against Iran on February 28, oil prices have risen by 55%. The continued blockade of the Strait of Hormuz has not only disrupted oil supplies but also affected the supply chains of other important commodities such as aluminum and urea.

This series of chain reactions has significantly boosted global inflation expectations, and market expectations for a Federal Reserve rate cut this year have cooled considerably. Before the conflict erupted, traders had priced in a near 80% probability of two Fed rate cuts by the end of the year; now that probability has fallen to less than 2%.

As the stock market accelerated its decline in the second half of March, investors hoping to hedge their investments with bonds were also disappointed. The U.S. Treasury market experienced its worst sell-off since the tariff crisis last April, causing the traditional "60% stocks and 40% bonds" portfolio to perform almost as badly as simply holding stocks.

BlackRock CEO Larry Fink warned last week of the potential impact of a conflict with Iran. He stated that if post-war Iran can reintegrate into the global trading system, the increased supply will help lower and stabilize global energy prices. However, if Tehran continues to pose a threat, oil prices could remain above $100 per barrel for years to come.

Fink said, "The scenario of $40 oil prices corresponds to abundance and growth, while the other scenario could lead to a severe and deep recession."

Despite market pressure, the fundamentals of the stock market have not completely collapsed. According to FactSet data, analysts expect S&P 500 companies to achieve double-digit earnings growth for the sixth consecutive quarter in the first three quarters of 2026. Individual investors, while slowing their buying pace, are still net buyers of stocks.

However, the sharp rise in energy prices is putting additional pressure on the U.S. economy. Steven Blitz, chief economist at TS Lombard, stated, "The main risk is that the U.S. economy was already somewhat shaky going into the first quarter, and now an energy tax has been added to that." The oil shock will significantly increase energy costs for consumers and businesses, thereby dragging down economic growth.

Amidst the sharp fluctuations, the market has also shown a clear divergence. The S&P 500 energy sector has risen 39% year-to-date, on track for its best quarterly performance on record.

"Heavy asset" industries such as materials have also shown relative resilience, with investors tending to look for companies that are less susceptible to disruption by artificial intelligence.

Meanwhile, many analysts maintain their forecasts for a modest rise in the stock market in 2026, but these forecasts are all based on a key assumption: that the Middle East conflict will be relatively short-lived and that its impact on the global economy can be effectively controlled.

Overall, the Iranian conflict has become the single biggest variable dominating the US stock market. High oil prices have not only pushed up inflation and suppressed expectations of interest rate cuts, but have also rendered traditional hedging mechanisms ineffective, with Wall Street rapidly shifting from its optimism at the beginning of the year to a cautious defensive stance.

Michael Kantrowitz summarized: "This is a market driven by a single variable. If oil prices don't fall, the market won't rise—it's that simple."

In the short term, the US stock market still faces significant downward pressure. If the Iranian conflict continues, the Strait of Hormuz blockade will remain difficult to lift, oil prices will continue to remain high, inflation expectations will be difficult to decline, the probability of a Federal Reserve rate cut will further decrease, and stock market valuations will be squeezed. The energy sector and some defensive, asset-heavy sectors may continue to be relatively strong, while technology and growth stocks will face greater downward pressure.

In the medium term, if the conflict sees substantial easing or a diplomatic breakthrough before summer, oil prices are expected to fall, market expectations for a Federal Reserve rate cut will rise again, and the stock market is likely to see a corrective rebound. However, if the conflict becomes protracted or even escalates, global supply chains continue to be disrupted, energy prices remain high for an extended period, the risk of a US recession will increase significantly, and the stock market may experience a deeper correction.

Overall assessment: The US stock market will maintain high volatility in the second quarter of 2026, with its performance heavily dependent on oil prices and geopolitical developments.

Investors should remain cautious and pay attention to the actual impact of energy costs on corporate profits and consumer spending. In terms of portfolio allocation, they can appropriately increase the weighting of defensive and energy-related sectors while controlling overall portfolio risk.

US Nasdaq quarterly chart. Source: FX678.

U.S. stocks are on track for their worst quarterly performance in nearly four years, with investors quickly shifting from a confident start to a defensive mindset.

The stock market shifted from optimism to correction, with both the Nasdaq and Dow Jones entering a period of adjustment.

At the beginning of 2026, the US stock market showed a relatively positive trend. Although some technology stocks stagnated, funds began to flow into previously neglected market sectors, attracted by low valuations and expectations of economic recovery. However, with the outbreak of conflict in the Middle East, everything came to a standstill.

On March 26, the Nasdaq Composite Index, dominated by technology stocks, fell more than 10% from its recent high, officially entering correction territory. A day later, the Dow Jones Industrial Average, a key indicator of the real economy, followed suit. As of now, the S&P 500 has erased all gains from the past seven months. In March, 10 of the S&P 500's 11 sectors declined, with an average drop of 8.3%, the only exception being the energy sector.

The conflict with Iran has become the biggest variable in the market, causing oil prices to surge by 55%.

"We had the perfect environment to extend the rally, with all the right timing, location, and people, but what happened next put it on hold," said Michael Kantrowitz, chief investment strategist at Piper Sandler.

Since the US and Israel launched military strikes against Iran on February 28, oil prices have risen by 55%. The continued blockade of the Strait of Hormuz has not only disrupted oil supplies but also affected the supply chains of other important commodities such as aluminum and urea.

This series of chain reactions has significantly boosted global inflation expectations, and market expectations for a Federal Reserve rate cut this year have cooled considerably. Before the conflict erupted, traders had priced in a near 80% probability of two Fed rate cuts by the end of the year; now that probability has fallen to less than 2%.

Traditional 60/40 portfolios are failing, putting pressure on both safe-haven assets.

As the stock market accelerated its decline in the second half of March, investors hoping to hedge their investments with bonds were also disappointed. The U.S. Treasury market experienced its worst sell-off since the tariff crisis last April, causing the traditional "60% stocks and 40% bonds" portfolio to perform almost as badly as simply holding stocks.

BlackRock CEO Larry Fink warned last week of the potential impact of a conflict with Iran. He stated that if post-war Iran can reintegrate into the global trading system, the increased supply will help lower and stabilize global energy prices. However, if Tehran continues to pose a threat, oil prices could remain above $100 per barrel for years to come.

Fink said, "The scenario of $40 oil prices corresponds to abundance and growth, while the other scenario could lead to a severe and deep recession."

The fundamentals remain resilient, but energy shocks pose new risks.

Despite market pressure, the fundamentals of the stock market have not completely collapsed. According to FactSet data, analysts expect S&P 500 companies to achieve double-digit earnings growth for the sixth consecutive quarter in the first three quarters of 2026. Individual investors, while slowing their buying pace, are still net buyers of stocks.

However, the sharp rise in energy prices is putting additional pressure on the U.S. economy. Steven Blitz, chief economist at TS Lombard, stated, "The main risk is that the U.S. economy was already somewhat shaky going into the first quarter, and now an energy tax has been added to that." The oil shock will significantly increase energy costs for consumers and businesses, thereby dragging down economic growth.

Winners and losers diverged, with the energy sector emerging as the biggest bright spot.

Amidst the sharp fluctuations, the market has also shown a clear divergence. The S&P 500 energy sector has risen 39% year-to-date, on track for its best quarterly performance on record.

"Heavy asset" industries such as materials have also shown relative resilience, with investors tending to look for companies that are less susceptible to disruption by artificial intelligence.

Meanwhile, many analysts maintain their forecasts for a modest rise in the stock market in 2026, but these forecasts are all based on a key assumption: that the Middle East conflict will be relatively short-lived and that its impact on the global economy can be effectively controlled.

In summary: A single variable is dominating the market; future trends depend on oil prices and the course of the conflict.

Overall, the Iranian conflict has become the single biggest variable dominating the US stock market. High oil prices have not only pushed up inflation and suppressed expectations of interest rate cuts, but have also rendered traditional hedging mechanisms ineffective, with Wall Street rapidly shifting from its optimism at the beginning of the year to a cautious defensive stance.

Michael Kantrowitz summarized: "This is a market driven by a single variable. If oil prices don't fall, the market won't rise—it's that simple."

Analysis of the Future Trend of the US Stock Market

In the short term, the US stock market still faces significant downward pressure. If the Iranian conflict continues, the Strait of Hormuz blockade will remain difficult to lift, oil prices will continue to remain high, inflation expectations will be difficult to decline, the probability of a Federal Reserve rate cut will further decrease, and stock market valuations will be squeezed. The energy sector and some defensive, asset-heavy sectors may continue to be relatively strong, while technology and growth stocks will face greater downward pressure.

In the medium term, if the conflict sees substantial easing or a diplomatic breakthrough before summer, oil prices are expected to fall, market expectations for a Federal Reserve rate cut will rise again, and the stock market is likely to see a corrective rebound. However, if the conflict becomes protracted or even escalates, global supply chains continue to be disrupted, energy prices remain high for an extended period, the risk of a US recession will increase significantly, and the stock market may experience a deeper correction.

Overall assessment: The US stock market will maintain high volatility in the second quarter of 2026, with its performance heavily dependent on oil prices and geopolitical developments.

Investors should remain cautious and pay attention to the actual impact of energy costs on corporate profits and consumer spending. In terms of portfolio allocation, they can appropriately increase the weighting of defensive and energy-related sectors while controlling overall portfolio risk.

US Nasdaq quarterly chart. Source: FX678.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.