A chart shows the Baltic Dry Index falling to a near three-week low, potentially marking its first monthly decline in 2026.

2026-03-31 23:38:05

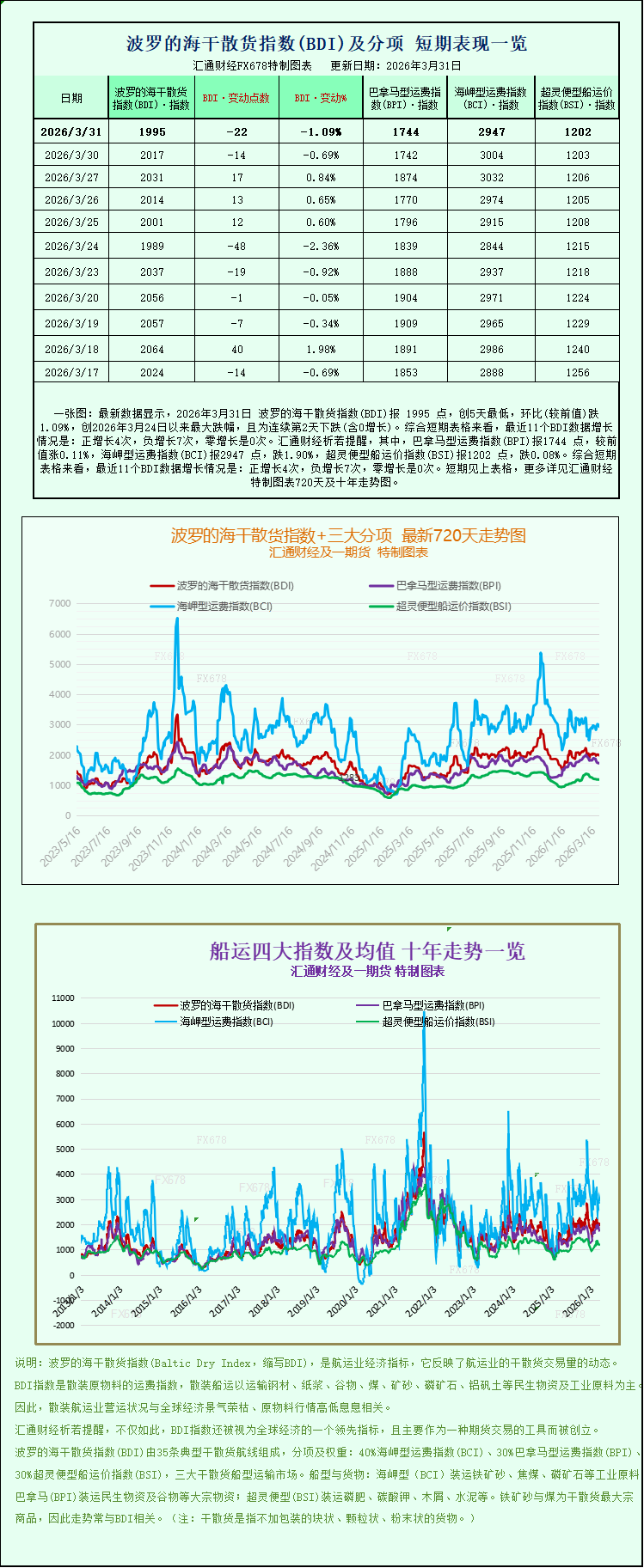

Latest data shows that the Baltic Dry Index (BDI) closed at 1995 points on March 31, 2026, a five-day low, down 1.09% from the previous day, marking the largest drop since March 24, 2026, and the second consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 4 positive increases, 7 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) closed at 1744 points, up 0.11% from the previous day; the Capesize Freight Index (BCI) closed at 2947 points, down 1.90%; and the Supramax Freight Index (BSI) closed at 1202 points, down 0.08%. For detailed 720-day and 10-year trends of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On Tuesday (March 31), the Baltic Dry Index (BDI) continued its downward trend from the previous trading day, marking its second consecutive day of decline. As a core indicator of the global dry bulk shipping market, the BDI primarily monitors freight rates for vessels transporting dry bulk commodities such as iron ore, coal, and grains worldwide. Its trend directly reflects changes in supply and demand and the overall health of the dry bulk shipping market. The core reason for this consecutive decline is the weak freight rates for the two main vessel types, Capesize and Panamax. As a result, the index is heading towards its first monthly loss this year, and market pessimism has increased.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—was under pressure, falling 22 points, or 1.1%, to close at 1995 points, near its lowest point in the past three weeks. Looking at monthly performance, the index's cumulative decline has gradually widened, currently indicating a potential monthly drop of 12.2%. This decline signifies that the dry bulk shipping market, after experiencing previous volatility, is facing a period of adjustment.

Looking at different vessel types, the Capesize market performed the weakest. The Capesize index fell 57 points, or about 1.9%, to close at 2947 points, near its lowest point in a week. So far this month, the index has fallen by nearly 6%. As the "giant" of the dry bulk shipping market, Capesize vessels mainly transport dry bulk cargoes of 150,000 tons and above, with core cargoes including basic industrial raw materials such as iron ore and coal. Their freight rates are closely related to global industrial demand. Affected by this, the average daily revenue of Capesize vessels also declined, decreasing by $524 on the day to $23,221, further squeezing shipowners' profit margins. It is understood that recent typhoons in Western Australia impacted iron ore shipments, while available shipping capacity remained relatively abundant. These two factors combined led to continued downward pressure on Capesize freight rates. Although long-haul routes maintained slight fluctuations at high levels due to tight available capacity, it was difficult to reverse the overall market downturn.

The decline in iron ore prices has further exacerbated the weakness in the Capesize shipping market. Previously, due to the tense situation surrounding the Iran-Iraq conflict, the market was generally concerned that soaring energy prices would lead to a significant increase in freight costs, thereby pushing up the transportation costs and prices of dry bulk commodities such as iron ore. However, with US President Trump's comments on ending the Iran-Iraq conflict, market concerns about soaring energy prices were significantly alleviated, and iron ore prices subsequently fell. This weakened market expectations for iron ore transportation, further dragging down Capesize freight rates and daily revenue. As of 11 PM on March 31, the main iron ore futures price was 815.0 yuan, a slight increase from the previous trading day, but still at a relatively low level, making it difficult to provide effective support for the dry bulk shipping market.

In contrast to the continued weakness in the Capesize market, the Panamax market showed a slight recovery on the day, but failed to reverse the overall monthly decline. The Panamax index rose 2 points, or 0.1%, to close at 1744 points; however, the index's cumulative decline for the month is still close to 10%, indicating that the overall market remains under pressure. Panamax vessels are mainly used for transit through the Panama Canal, with a deadweight tonnage typically between 60,000 and 70,000 tons. Their core cargoes are coal and grain, making them the mainstay of global grain transport, accounting for approximately 45% of global grain shipments. Affected by the recent drop in oil prices, inquiries for coal and grain have increased slightly, but the increase is limited. Therefore, the average daily revenue of Panamax vessels only saw a slight increase, rising by $10 to $15,692 on the day, indicating weak growth momentum and insufficient to drive a recovery in the overall dry bulk shipping market.

The Very Large Bulk Carrier (VLCC) index also saw a slight decline on the day, falling 1 point, or 0.1%, to close at 1202 points. The overall trend was relatively stable without significant fluctuations, and its impact on the overall dry bulk market was limited. VLCCs are mainly used for long-distance transportation of coal and iron ore exceeding 200,000 tons. Their freight rates are primarily influenced by the transportation demand from large global mines and steel mills. Currently, the market supply and demand are relatively balanced, hence the index's small fluctuations.

It is worth noting that fluctuations in the dry bulk shipping market are closely related to global geopolitical situations and energy market trends. On Tuesday, Brent crude oil futures prices continued their upward trend, further approaching highs and poised to record their largest monthly gain ever. Currently, investors are facing a dilemma: on the one hand, US President Trump's remarks about ending the war with Iran have eased market concerns about escalating geopolitical conflicts; on the other hand, the possibility of a prolonged closure of the Strait of Hormuz makes it difficult to completely dispel market concerns about the impact on global oil supply. According to data from the Tonghuashun financial database, as of March 30, the closing price of the main Brent crude oil futures contract reached $108.89 per barrel, a significant increase from $81.96 per barrel at the beginning of March, representing a substantial monthly increase. The sharp fluctuations in the energy market also indirectly affect the costs and demand in the dry bulk shipping market.

Geopolitically, the situation regarding the war with Iran remains at a critical juncture. US Defense Secretary Peter Hegses explicitly stated that the next few days would be decisive for the war against Iran, issuing a stern warning to Tehran that the current conflict would escalate further if Iran did not reach an agreement. Previously, Trump had repeatedly made tough statements on Iran, threatening a "20 times stronger strike" if Iran blocked the Strait of Hormuz. However, his recent stance has subtly shifted, indicating a willingness to end the conflict diplomatically. This shift is primarily influenced by a combination of factors, including uncontrolled military costs, domestic political and economic pressures, and the realities of battlefield combat. Hegses also previously stated that the US's objective in this action against Iran is clear: to "eliminate the risk of nuclear capability," rather than long-term intervention or reconstruction. He criticized the US media for "dooming the war" and European allies for "ungratefulness," adding that the whole world should thank Trump.

The International Monetary Fund (IMF) recently warned that a war between the US and Israel against Iran could trigger a "global but asymmetric" shock, pushing up global prices and dragging down economic growth, particularly impacting African and Asian countries heavily reliant on oil imports. It could also lead to higher food and fertilizer prices, threatening food security in low-income economies. Currently, the dry bulk shipping market is caught in a complex web of geopolitical disturbances, energy price fluctuations, and supply-demand adjustments. Whether the Baltic Dry Index can reverse its monthly losses remains to be seen and depends on close monitoring of the ongoing conflict in Iran, changes in global dry bulk demand, and energy price volatility.

On Tuesday (March 31), the Baltic Dry Index (BDI) continued its downward trend from the previous trading day, marking its second consecutive day of decline. As a core indicator of the global dry bulk shipping market, the BDI primarily monitors freight rates for vessels transporting dry bulk commodities such as iron ore, coal, and grains worldwide. Its trend directly reflects changes in supply and demand and the overall health of the dry bulk shipping market. The core reason for this consecutive decline is the weak freight rates for the two main vessel types, Capesize and Panamax. As a result, the index is heading towards its first monthly loss this year, and market pessimism has increased.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—was under pressure, falling 22 points, or 1.1%, to close at 1995 points, near its lowest point in the past three weeks. Looking at monthly performance, the index's cumulative decline has gradually widened, currently indicating a potential monthly drop of 12.2%. This decline signifies that the dry bulk shipping market, after experiencing previous volatility, is facing a period of adjustment.

Looking at different vessel types, the Capesize market performed the weakest. The Capesize index fell 57 points, or about 1.9%, to close at 2947 points, near its lowest point in a week. So far this month, the index has fallen by nearly 6%. As the "giant" of the dry bulk shipping market, Capesize vessels mainly transport dry bulk cargoes of 150,000 tons and above, with core cargoes including basic industrial raw materials such as iron ore and coal. Their freight rates are closely related to global industrial demand. Affected by this, the average daily revenue of Capesize vessels also declined, decreasing by $524 on the day to $23,221, further squeezing shipowners' profit margins. It is understood that recent typhoons in Western Australia impacted iron ore shipments, while available shipping capacity remained relatively abundant. These two factors combined led to continued downward pressure on Capesize freight rates. Although long-haul routes maintained slight fluctuations at high levels due to tight available capacity, it was difficult to reverse the overall market downturn.

The decline in iron ore prices has further exacerbated the weakness in the Capesize shipping market. Previously, due to the tense situation surrounding the Iran-Iraq conflict, the market was generally concerned that soaring energy prices would lead to a significant increase in freight costs, thereby pushing up the transportation costs and prices of dry bulk commodities such as iron ore. However, with US President Trump's comments on ending the Iran-Iraq conflict, market concerns about soaring energy prices were significantly alleviated, and iron ore prices subsequently fell. This weakened market expectations for iron ore transportation, further dragging down Capesize freight rates and daily revenue. As of 11 PM on March 31, the main iron ore futures price was 815.0 yuan, a slight increase from the previous trading day, but still at a relatively low level, making it difficult to provide effective support for the dry bulk shipping market.

In contrast to the continued weakness in the Capesize market, the Panamax market showed a slight recovery on the day, but failed to reverse the overall monthly decline. The Panamax index rose 2 points, or 0.1%, to close at 1744 points; however, the index's cumulative decline for the month is still close to 10%, indicating that the overall market remains under pressure. Panamax vessels are mainly used for transit through the Panama Canal, with a deadweight tonnage typically between 60,000 and 70,000 tons. Their core cargoes are coal and grain, making them the mainstay of global grain transport, accounting for approximately 45% of global grain shipments. Affected by the recent drop in oil prices, inquiries for coal and grain have increased slightly, but the increase is limited. Therefore, the average daily revenue of Panamax vessels only saw a slight increase, rising by $10 to $15,692 on the day, indicating weak growth momentum and insufficient to drive a recovery in the overall dry bulk shipping market.

The Very Large Bulk Carrier (VLCC) index also saw a slight decline on the day, falling 1 point, or 0.1%, to close at 1202 points. The overall trend was relatively stable without significant fluctuations, and its impact on the overall dry bulk market was limited. VLCCs are mainly used for long-distance transportation of coal and iron ore exceeding 200,000 tons. Their freight rates are primarily influenced by the transportation demand from large global mines and steel mills. Currently, the market supply and demand are relatively balanced, hence the index's small fluctuations.

It is worth noting that fluctuations in the dry bulk shipping market are closely related to global geopolitical situations and energy market trends. On Tuesday, Brent crude oil futures prices continued their upward trend, further approaching highs and poised to record their largest monthly gain ever. Currently, investors are facing a dilemma: on the one hand, US President Trump's remarks about ending the war with Iran have eased market concerns about escalating geopolitical conflicts; on the other hand, the possibility of a prolonged closure of the Strait of Hormuz makes it difficult to completely dispel market concerns about the impact on global oil supply. According to data from the Tonghuashun financial database, as of March 30, the closing price of the main Brent crude oil futures contract reached $108.89 per barrel, a significant increase from $81.96 per barrel at the beginning of March, representing a substantial monthly increase. The sharp fluctuations in the energy market also indirectly affect the costs and demand in the dry bulk shipping market.

Geopolitically, the situation regarding the war with Iran remains at a critical juncture. US Defense Secretary Peter Hegses explicitly stated that the next few days would be decisive for the war against Iran, issuing a stern warning to Tehran that the current conflict would escalate further if Iran did not reach an agreement. Previously, Trump had repeatedly made tough statements on Iran, threatening a "20 times stronger strike" if Iran blocked the Strait of Hormuz. However, his recent stance has subtly shifted, indicating a willingness to end the conflict diplomatically. This shift is primarily influenced by a combination of factors, including uncontrolled military costs, domestic political and economic pressures, and the realities of battlefield combat. Hegses also previously stated that the US's objective in this action against Iran is clear: to "eliminate the risk of nuclear capability," rather than long-term intervention or reconstruction. He criticized the US media for "dooming the war" and European allies for "ungratefulness," adding that the whole world should thank Trump.

The International Monetary Fund (IMF) recently warned that a war between the US and Israel against Iran could trigger a "global but asymmetric" shock, pushing up global prices and dragging down economic growth, particularly impacting African and Asian countries heavily reliant on oil imports. It could also lead to higher food and fertilizer prices, threatening food security in low-income economies. Currently, the dry bulk shipping market is caught in a complex web of geopolitical disturbances, energy price fluctuations, and supply-demand adjustments. Whether the Baltic Dry Index can reverse its monthly losses remains to be seen and depends on close monitoring of the ongoing conflict in Iran, changes in global dry bulk demand, and energy price volatility.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.