The non-farm payrolls report exceeded expectations, but the market reacted negatively.

2026-04-06 09:35:34

The seemingly strong US non-farm payroll data for March last Friday failed to provide a substantial boost to the volatile market. Apart from the US dollar index, US stocks and bonds did not show any signs of improvement.

Amid the intertwined inflationary shocks and recession risks triggered by the Iran war, US stocks and bonds may continue their downward trend from last month, while the US dollar is expected to continue to strengthen due to interest rate stickiness and safe-haven demand.

The US job market delivered better-than-expected results in March: non-farm payrolls increased by 178,000, significantly exceeding economists' median forecast of 60,000; the unemployment rate unexpectedly fell to 4.3%, the same as in January, reversing the slight upward trend that rose to 4.4% in February.

Released as most global financial markets were closed for the Easter holiday, this data should have been a boost to the market. However, it failed to change traders' bearish sentiment. The core reason is that the Federal Reserve is deeply mired in the inflationary predicament triggered by the Iran war, a shock that has posed a substantial threat to US economic growth. Meanwhile, the main driver of the better-than-expected non-farm payrolls data remains the rebound following the strikes in the healthcare and nursing care sectors.

A closer look at the non-farm payroll data reveals multiple hidden concerns beneath the optimistic surface.

Most alarming is the continued decline in the labor force participation rate: in March, the figure fell to 61.9%, the lowest level since November 2021.

From a statistical perspective, this is precisely the key driver behind the decline in the unemployment rate over the past 21 years—those who do not actively seek work are not included in the "unemployment" statistics, which means that the improvement in the unemployment rate does not stem from a genuine recovery in the job market.

The structural imbalances in employment growth further exacerbate the vulnerability of the economy.

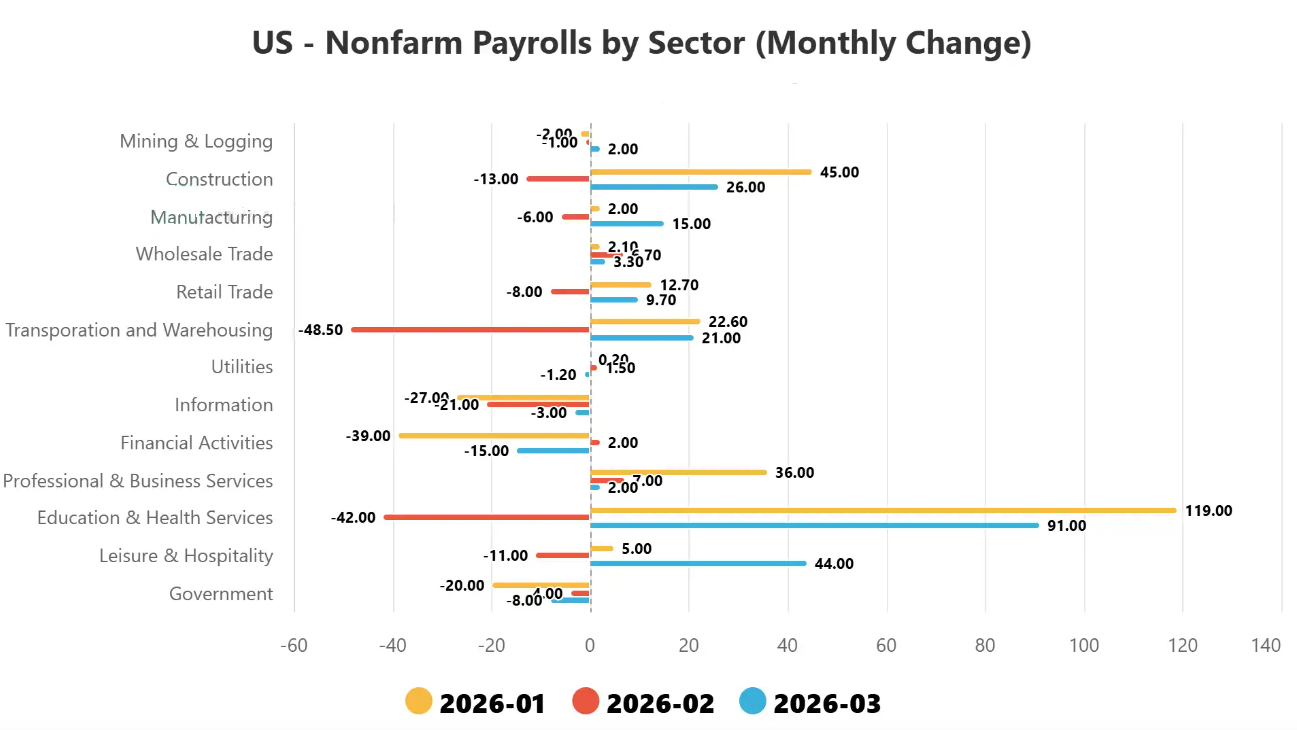

Of the new jobs created in March, the education and healthcare sector contributed 91,000, accounting for half of the total increase, while the second and third ranked sectors, leisure and hospitality (44,000) and construction (26,000), showed significantly weak growth.

Behind this pattern lies the structural impact of the aging population in the United States: the number of people aged 55 and over has approached 105 million, accounting for 30.6% of the total population (both of which are record highs), but the labor force participation rate in this age group is only 37.2% (the lowest in 11 years); on the other hand, the core working-age group of 24-54 has a participation rate as high as 83.8%, but has failed to become the main force for employment growth.

This structural characteristic has a dual impact: on the one hand, the healthcare industry, which relies on the needs of an aging population, provides employment growth with a certain degree of counter-cyclical capability in the short term; on the other hand, the sluggish growth of cyclical industries means that once an external shock occurs, a wave of layoffs may quickly cover the structural increase in employment, leading to severe economic fluctuations.

(A summary of major changes in non-farm payrolls)

Currently, the Iraq War is becoming the trigger for this potential shock.

Market concerns about the conflict have gradually escalated from an initial "price surge" to "recession risk".

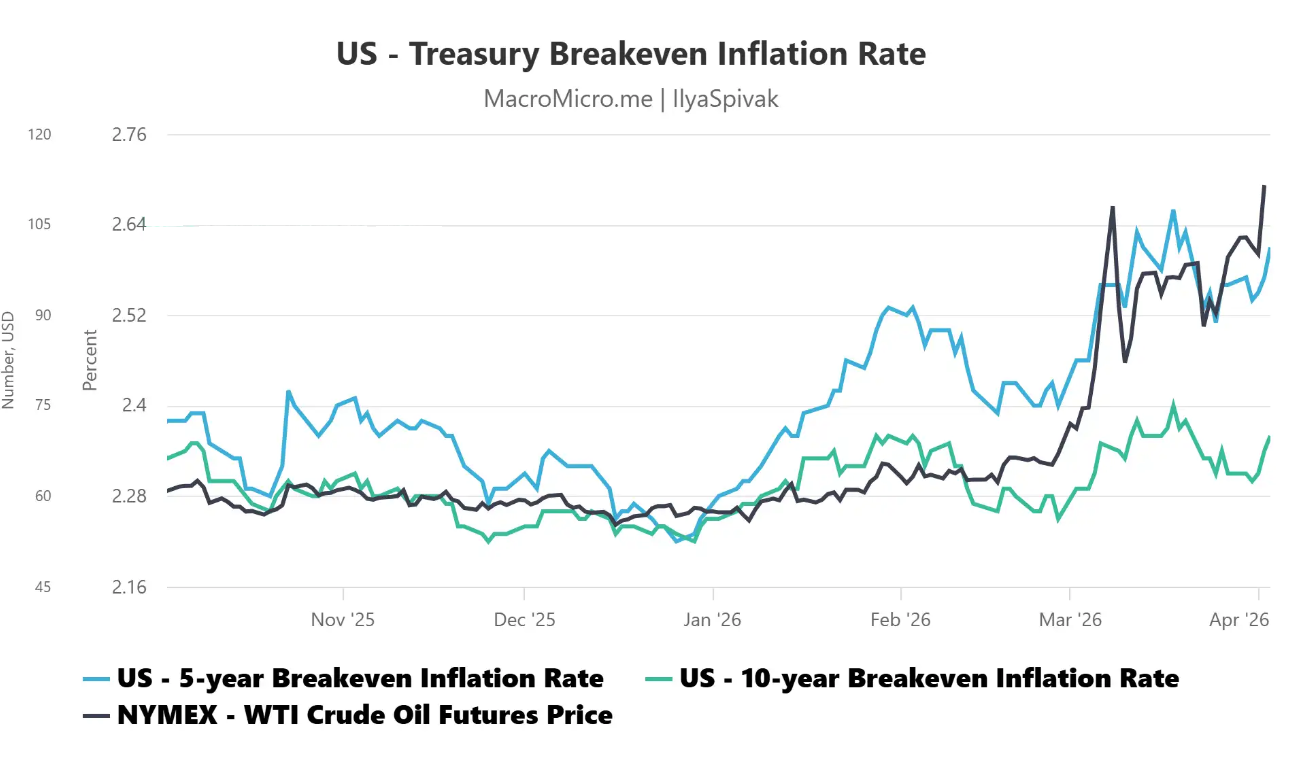

Despite the continued rise in oil prices, inflation expectations implied in the bond market have cooled, reflecting investors' cautious assessment of the economic outlook. The inflationary shock triggered by the closure of the Strait of Hormuz has completely eroded the futures market's pricing of Federal Reserve interest rate cuts, a scenario that had persisted since the outbreak of the war.

(Chart showing the overlay of US Treasury yields and international oil prices)

Before the Federal Reserve can clearly define the peak and duration of inflation, it will be difficult for it to take substantial easing measures. The positive non-farm payroll data in March has given the Fed a reasonable excuse to "wait and see".

For traders, this means that stimulus measures will lag behind the actual damage to the economy.

When high prices actually cause substantial damage to the economy, a structurally imbalanced labor market may trigger a sharp collapse in demand rather than a gradual slowdown.

This expectation also directly points to a bearish outlook in the asset market:

US stocks and bonds may resume their synchronized downward trend from last month, while the US dollar will continue to strengthen, driven by interest rate stickiness and liquidity demand fueled by risk aversion – in fact, the US dollar has already shown clear upward momentum after the release of the March non-farm payroll data.

Ultimately, the "optimism" surrounding the March US non-farm payroll data remains superficial. The structural imbalance in job growth, the sluggish labor force participation rate, coupled with the external shocks from the Iran war and the Federal Reserve's policy lag, make it difficult for the market to truly recognize the boosting significance of this data. Cautious sentiment will continue to dominate short-term market trends.

Amid the intertwined inflationary shocks and recession risks triggered by the Iran war, US stocks and bonds may continue their downward trend from last month, while the US dollar is expected to continue to strengthen due to interest rate stickiness and safe-haven demand.

The US job market delivered better-than-expected results in March: non-farm payrolls increased by 178,000, significantly exceeding economists' median forecast of 60,000; the unemployment rate unexpectedly fell to 4.3%, the same as in January, reversing the slight upward trend that rose to 4.4% in February.

Released as most global financial markets were closed for the Easter holiday, this data should have been a boost to the market. However, it failed to change traders' bearish sentiment. The core reason is that the Federal Reserve is deeply mired in the inflationary predicament triggered by the Iran war, a shock that has posed a substantial threat to US economic growth. Meanwhile, the main driver of the better-than-expected non-farm payrolls data remains the rebound following the strikes in the healthcare and nursing care sectors.

Beneath the optimistic surface of the data lie two major hidden concerns.

A closer look at the non-farm payroll data reveals multiple hidden concerns beneath the optimistic surface.

Most alarming is the continued decline in the labor force participation rate: in March, the figure fell to 61.9%, the lowest level since November 2021.

From a statistical perspective, this is precisely the key driver behind the decline in the unemployment rate over the past 21 years—those who do not actively seek work are not included in the "unemployment" statistics, which means that the improvement in the unemployment rate does not stem from a genuine recovery in the job market.

The employment structure is unbalanced, and the economy is weak in its ability to withstand risks.

The structural imbalances in employment growth further exacerbate the vulnerability of the economy.

Of the new jobs created in March, the education and healthcare sector contributed 91,000, accounting for half of the total increase, while the second and third ranked sectors, leisure and hospitality (44,000) and construction (26,000), showed significantly weak growth.

Behind this pattern lies the structural impact of the aging population in the United States: the number of people aged 55 and over has approached 105 million, accounting for 30.6% of the total population (both of which are record highs), but the labor force participation rate in this age group is only 37.2% (the lowest in 11 years); on the other hand, the core working-age group of 24-54 has a participation rate as high as 83.8%, but has failed to become the main force for employment growth.

This structural characteristic has a dual impact: on the one hand, the healthcare industry, which relies on the needs of an aging population, provides employment growth with a certain degree of counter-cyclical capability in the short term; on the other hand, the sluggish growth of cyclical industries means that once an external shock occurs, a wave of layoffs may quickly cover the structural increase in employment, leading to severe economic fluctuations.

(A summary of major changes in non-farm payrolls)

Escalating conflict with Iran: Recession risks replace inflation concerns

Currently, the Iraq War is becoming the trigger for this potential shock.

Market concerns about the conflict have gradually escalated from an initial "price surge" to "recession risk".

Despite the continued rise in oil prices, inflation expectations implied in the bond market have cooled, reflecting investors' cautious assessment of the economic outlook. The inflationary shock triggered by the closure of the Strait of Hormuz has completely eroded the futures market's pricing of Federal Reserve interest rate cuts, a scenario that had persisted since the outbreak of the war.

(Chart showing the overlay of US Treasury yields and international oil prices)

The Federal Reserve's lagging policy and wait-and-see attitude have exacerbated market anxiety.

Before the Federal Reserve can clearly define the peak and duration of inflation, it will be difficult for it to take substantial easing measures. The positive non-farm payroll data in March has given the Fed a reasonable excuse to "wait and see".

For traders, this means that stimulus measures will lag behind the actual damage to the economy.

When high prices actually cause substantial damage to the economy, a structurally imbalanced labor market may trigger a sharp collapse in demand rather than a gradual slowdown.

Asset Market Outlook: US stocks and bonds under pressure, stronger dollar highly probable

This expectation also directly points to a bearish outlook in the asset market:

US stocks and bonds may resume their synchronized downward trend from last month, while the US dollar will continue to strengthen, driven by interest rate stickiness and liquidity demand fueled by risk aversion – in fact, the US dollar has already shown clear upward momentum after the release of the March non-farm payroll data.

Ultimately, the "optimism" surrounding the March US non-farm payroll data remains superficial. The structural imbalance in job growth, the sluggish labor force participation rate, coupled with the external shocks from the Iran war and the Federal Reserve's policy lag, make it difficult for the market to truly recognize the boosting significance of this data. Cautious sentiment will continue to dominate short-term market trends.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.