If the US-Iran ceasefire remains in place, the spread between Brent and WTI near-month contracts is expected to return to a normal premium.

2026-04-10 13:58:36

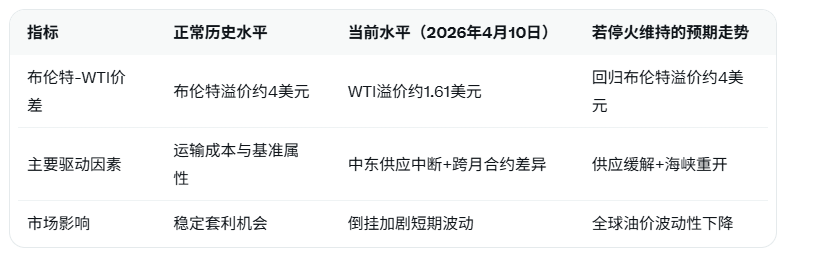

According to the App, Capital Economics economist Hamad Hussein stated that if the recent ceasefire agreement between the US and Iran is maintained, the price spread between Brent and WTI crude oil near-month contracts is expected to return to normal. Normally, Brent crude oil has a premium of about $4 per barrel over WTI crude oil , but this traditional pattern has been completely disrupted since the outbreak of the current Middle East conflict.

Hamad Hussein specifically pointed out that the current inverted spread measures the price difference between Brent crude futures for June delivery and WTI crude futures for May delivery, despite their different contract expiration dates. This cross-month design aims to more accurately reflect market expectations for short-term supply and demand. However, due to the recent significant tightening of the oil market caused by supply disruptions in the Middle East, coupled with widespread market expectations that supply conditions will gradually ease in the coming months, the premium of WTI crude over Brent crude has actually widened further.

The latest market data shows that as of April 10, 2026, the May WTI crude oil futures contract was trading at approximately $98.36 per barrel, while the June Brent crude oil futures contract was trading at approximately $96.75 per barrel. WTI crude oil was trading at a premium of approximately $1.61 per barrel to Brent crude oil , exhibiting a clear price inversion. This inversion has widened since the beginning of the conflict, primarily reflecting the combined impact of relatively abundant domestic crude oil inventories in the United States and disruptions to shipping from the Middle East.

Hamad Hussein 's analysis emphasizes that if the US-Iran ceasefire agreement is truly implemented and maintained, and tanker traffic in the Strait of Hormuz returns to normal, the bottleneck in Middle Eastern crude oil supply will gradually be resolved, and the premium of Brent crude as the global benchmark is expected to quickly return to its historical average level. This will not only help smooth out the current abnormal fluctuations in cross-contract price spreads, but will also provide global refiners with more stable arbitrage opportunities.

The following table compares key changes in the Brent-WTI price spread:

The oil market remains in a phase of high uncertainty. While the ceasefire agreement brings optimistic expectations, the details of its implementation, actual traffic volume in the Strait of Hormuz, and the potential spillover risks from the Israel-Lebanon situation could still cause fluctuations in the normalization of price spreads. Capital Economics ' assessment provides a clear baseline scenario for the market: tight supply will support high oil prices in the short term, but the implementation of the agreement will gradually release downward pressure.

Editor's Summary:

Hamad Hussein 's latest views highlight the direct impact of geopolitical easing on the correction of crude oil benchmark price spreads. While the current inverted spread reflects tight supply, if the ceasefire agreement is maintained, the return of the traditional Brent premium will reshape the global oil market pricing logic. Investors need to continuously monitor Straits Times data and cross-month contract dynamics to seize potential arbitrage and hedging opportunities.

Hamad Hussein specifically pointed out that the current inverted spread measures the price difference between Brent crude futures for June delivery and WTI crude futures for May delivery, despite their different contract expiration dates. This cross-month design aims to more accurately reflect market expectations for short-term supply and demand. However, due to the recent significant tightening of the oil market caused by supply disruptions in the Middle East, coupled with widespread market expectations that supply conditions will gradually ease in the coming months, the premium of WTI crude over Brent crude has actually widened further.

The latest market data shows that as of April 10, 2026, the May WTI crude oil futures contract was trading at approximately $98.36 per barrel, while the June Brent crude oil futures contract was trading at approximately $96.75 per barrel. WTI crude oil was trading at a premium of approximately $1.61 per barrel to Brent crude oil , exhibiting a clear price inversion. This inversion has widened since the beginning of the conflict, primarily reflecting the combined impact of relatively abundant domestic crude oil inventories in the United States and disruptions to shipping from the Middle East.

Hamad Hussein 's analysis emphasizes that if the US-Iran ceasefire agreement is truly implemented and maintained, and tanker traffic in the Strait of Hormuz returns to normal, the bottleneck in Middle Eastern crude oil supply will gradually be resolved, and the premium of Brent crude as the global benchmark is expected to quickly return to its historical average level. This will not only help smooth out the current abnormal fluctuations in cross-contract price spreads, but will also provide global refiners with more stable arbitrage opportunities.

The following table compares key changes in the Brent-WTI price spread:

The oil market remains in a phase of high uncertainty. While the ceasefire agreement brings optimistic expectations, the details of its implementation, actual traffic volume in the Strait of Hormuz, and the potential spillover risks from the Israel-Lebanon situation could still cause fluctuations in the normalization of price spreads. Capital Economics ' assessment provides a clear baseline scenario for the market: tight supply will support high oil prices in the short term, but the implementation of the agreement will gradually release downward pressure.

Editor's Summary:

Hamad Hussein 's latest views highlight the direct impact of geopolitical easing on the correction of crude oil benchmark price spreads. While the current inverted spread reflects tight supply, if the ceasefire agreement is maintained, the return of the traditional Brent premium will reshape the global oil market pricing logic. Investors need to continuously monitor Straits Times data and cross-month contract dynamics to seize potential arbitrage and hedging opportunities.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.