One chart: The Baltic Dry Index remains stable, with various sectors trending towards equilibrium.

2026-04-28 00:39:17

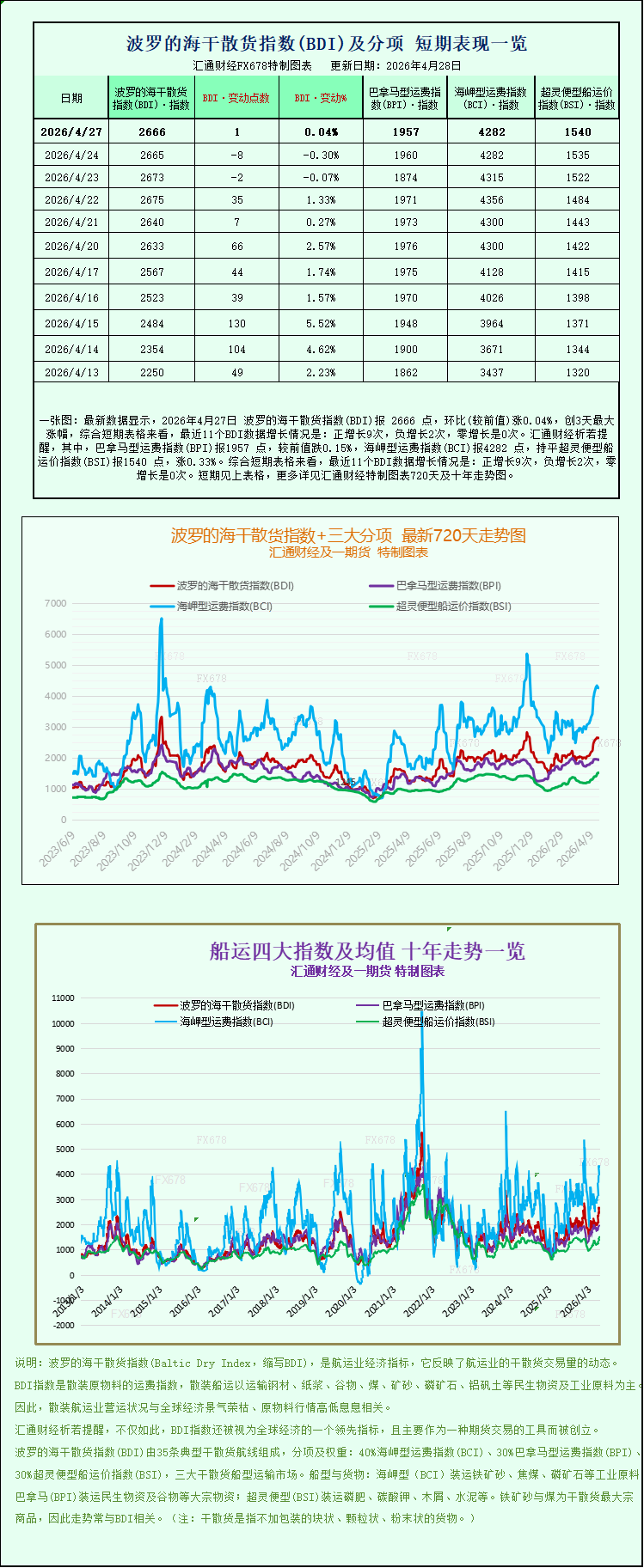

The latest data shows that on April 27, 2026, the Baltic Dry Index (BDI) was 2666 points, up 0.04% from the previous day, marking the largest increase in three days. Looking at the short-term charts, the BDI saw positive growth 9 times, negative growth 2 times, and zero growth in the last 11 BDI readings. Specifically, the Panamax Freight Index (BPI) was 1957 points, down 0.15% from the previous day; the Capesize Freight Index (BCI) was 4282 points; the Supramax Freight Index (BSI) was unchanged at 1540 points, up 0.33%. For detailed charts including the latest 720-day and 10-year trends of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The global dry bulk shipping market has been operating smoothly recently. The Baltic Dry Index has remained stable overall, with freight rates for various vessel segments showing mixed trends and narrowing fluctuations. The overall market trend is gradually moving towards equilibrium, without any significant unilateral fluctuations.

The global dry bulk shipping market saw a moderate correction on Monday. The Baltic Dry Index, a key indicator for real-time monitoring of freight rates for global industrial raw materials and bulk dry bulk shipping vessels, remained generally stable. Due to a balance between order increases and decreases across different vessel types and routes, and a moderate supply-demand dynamic, freight rate fluctuations across different tonnage segments were minimal, resulting in a generally calmer industry pace.

The Baltic Dry Index, which integrates freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose slightly by 1 point to close at 2666 points, showing a small upward trend but demonstrating strong overall resilience.

Among them, the Capesize index, which mainly transports bulk industrial raw materials, remained flat throughout the day, closing unchanged at 4282 points, indicating that the large ocean freight sector remained strong. This type of vessel mainly carries ultra-large cargoes of 150,000 tons, with core transport categories including essential industrial raw materials such as iron ore and thermal coal. The average daily charter income of its benchmark vessels rose slightly, increasing by $1 per day to reach $35,334, and the profitability of large shipowners remained basically stable.

On the raw material market, international iron ore spot prices fluctuated within a narrow range on Monday. Downstream demand provided ample support. As a major global steel producer and consumer, domestic steel companies began concentrated pre-holiday restocking, coupled with a continued decline in overall industry raw material inventories, effectively offsetting the increased supply pressure from upstream suppliers. Meanwhile, negative factors such as continued increases in shipments from major Australian mines and weak profit margins in the steel industry were gradually absorbed, collectively contributing to stable iron ore prices and indirectly stabilizing demand for Capesize shipping.

The medium-tonnage shipping sector saw a slight decline, with the Panamax index falling 3 points, or about 0.2%, to close at 1957 points, indicating slight downward pressure. This type of vessel has a standard deadweight range of 60,000 to 70,000 tons and is primarily responsible for transporting bulk commodities such as coal and grain across global regions. The average daily operating revenue of benchmark vessels also declined, decreasing by $21 to $17,617, indicating slightly weaker demand in the medium-tonnage freight market.

In the small and medium-sized cargo vessel sector, the market rebounded slightly against the trend. The Supramax vessel index steadily rose, gaining 5 points (0.3%) to close at 1540 points. Small and medium-sized bulk carriers are more flexible and suitable for short-distance and diversified transportation. The slight increase in this sector made up for the decline in Panamax vessels, further helping the overall market index maintain a balanced pattern.

The global dry bulk shipping market has been operating smoothly recently. The Baltic Dry Index has remained stable overall, with freight rates for various vessel segments showing mixed trends and narrowing fluctuations. The overall market trend is gradually moving towards equilibrium, without any significant unilateral fluctuations.

The global dry bulk shipping market saw a moderate correction on Monday. The Baltic Dry Index, a key indicator for real-time monitoring of freight rates for global industrial raw materials and bulk dry bulk shipping vessels, remained generally stable. Due to a balance between order increases and decreases across different vessel types and routes, and a moderate supply-demand dynamic, freight rate fluctuations across different tonnage segments were minimal, resulting in a generally calmer industry pace.

The Baltic Dry Index, which integrates freight rates for the three major vessel types—Capesize, Panamax, and Supramax—rose slightly by 1 point to close at 2666 points, showing a small upward trend but demonstrating strong overall resilience.

Among them, the Capesize index, which mainly transports bulk industrial raw materials, remained flat throughout the day, closing unchanged at 4282 points, indicating that the large ocean freight sector remained strong. This type of vessel mainly carries ultra-large cargoes of 150,000 tons, with core transport categories including essential industrial raw materials such as iron ore and thermal coal. The average daily charter income of its benchmark vessels rose slightly, increasing by $1 per day to reach $35,334, and the profitability of large shipowners remained basically stable.

On the raw material market, international iron ore spot prices fluctuated within a narrow range on Monday. Downstream demand provided ample support. As a major global steel producer and consumer, domestic steel companies began concentrated pre-holiday restocking, coupled with a continued decline in overall industry raw material inventories, effectively offsetting the increased supply pressure from upstream suppliers. Meanwhile, negative factors such as continued increases in shipments from major Australian mines and weak profit margins in the steel industry were gradually absorbed, collectively contributing to stable iron ore prices and indirectly stabilizing demand for Capesize shipping.

The medium-tonnage shipping sector saw a slight decline, with the Panamax index falling 3 points, or about 0.2%, to close at 1957 points, indicating slight downward pressure. This type of vessel has a standard deadweight range of 60,000 to 70,000 tons and is primarily responsible for transporting bulk commodities such as coal and grain across global regions. The average daily operating revenue of benchmark vessels also declined, decreasing by $21 to $17,617, indicating slightly weaker demand in the medium-tonnage freight market.

In the small and medium-sized cargo vessel sector, the market rebounded slightly against the trend. The Supramax vessel index steadily rose, gaining 5 points (0.3%) to close at 1540 points. Small and medium-sized bulk carriers are more flexible and suitable for short-distance and diversified transportation. The slight increase in this sector made up for the decline in Panamax vessels, further helping the overall market index maintain a balanced pattern.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.