A chart shows the Baltic Dry Index hitting a five-month high, driven by a significant rise in Capesize and Panamax bulk carriers.

2026-05-05 22:57:04

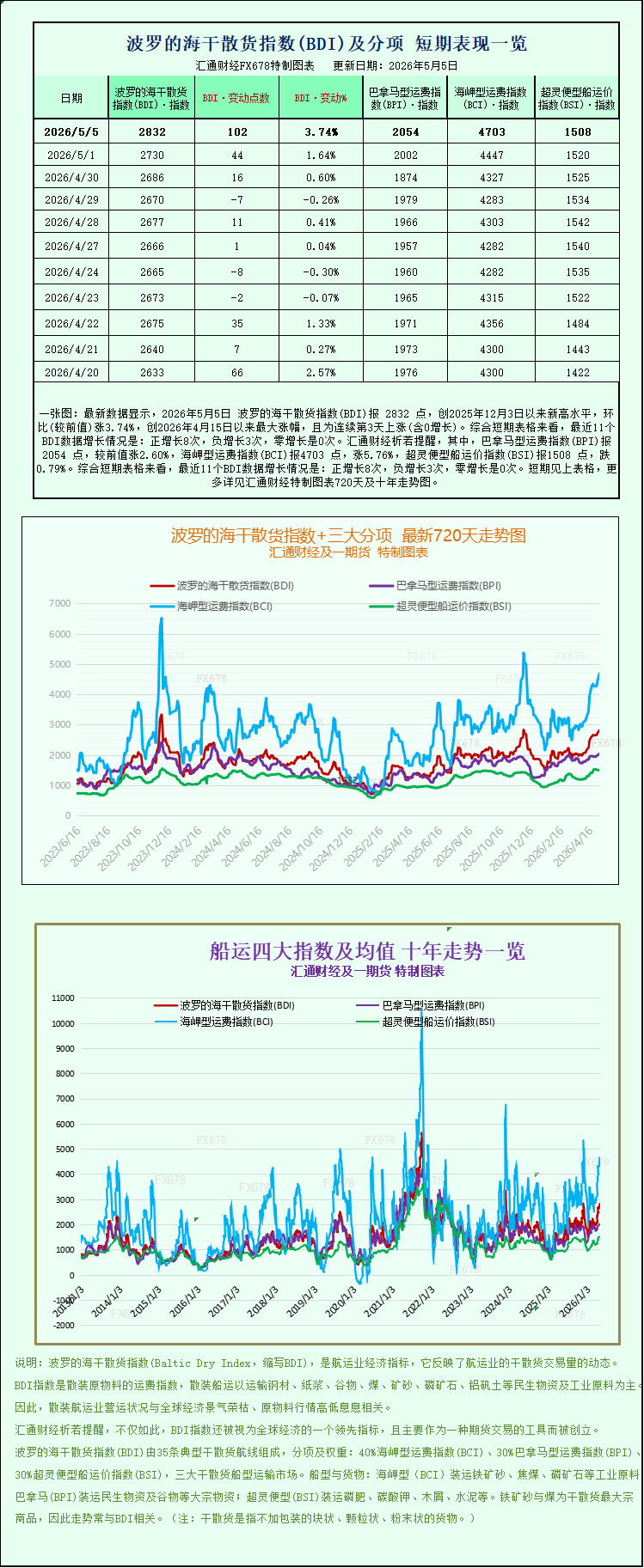

Latest data shows that the Baltic Dry Index (BDI) reached 2832 points on May 5, 2026, a new high since December 3, 2025, up 3.74% month-on-month, the largest increase since April 15, 2026, and marking the third consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) reached 2054 points, up 2.60% from the previous value; the Capesize Freight Index (BCI) reached 4703 points, up 5.76%; and the Supramax Freight Index (BSI) reached 1508 points, down 0.79%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a significant surge on Tuesday, reaching its highest level in five months. This strong rise was mainly driven by the continued strength of the two core bulk carrier sectors, Capesize and Panamax, reflecting the structural recovery in the current global dry bulk shipping market and also profoundly influenced by recent geopolitical events. As a core indicator of the global dry bulk shipping market, the index directly monitors fluctuations in freight rates for ships transporting dry bulk commodities such as iron ore, coal, and grains worldwide, and its trends have historically been regarded as a "barometer" of global industrial demand and international trade activity.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—performed strongly on the day, rising 102 points, or 3.7%, to close at 2832 points. This closing level not only marked the highest point since early December 2025 but also signifies a two-month consecutive rebound since the index bottomed out in early March, with a cumulative increase of over 40%, highlighting the strong recovery momentum in the dry bulk market. Historically, the index fell to a low of 1919 points on March 10, 2026, before gradually stabilizing and rebounding, accelerating its rise since April and demonstrating a clear upward trend.

The Capesize sector was particularly strong, serving as the core engine of the index's rise. The Capesize index surged 256 points, a 5.8% increase, closing at 4703 points, its highest point in five months, becoming a key driver of the overall index's upward movement. Capesize vessels, among the world's largest bulk carriers, primarily transport dry bulk cargo of 150,000 tons and above. Their core cargoes include basic industrial raw materials such as iron ore and coal, making them a crucial link in the global steel and energy supply chains. Correspondingly, the average daily revenue of Capesize vessels (.BATCA) carrying 150,000 tons of cargo (mainly iron ore and coal) also climbed, increasing by $2,318 to reach $39,146. This revenue level represents a nearly 60% increase from the low point in early March, reflecting a significant recovery in market demand for large bulk cargo transportation.

Besides the Capesize sector, the Panamax sector also showed a steady upward trend, providing strong support for the overall index. The Panamax index rose 52 points, or 2.6%, to close at 2054 points, continuing its recent upward trend. Panamax bulk carriers are bulk carriers with a deadweight tonnage between 60,000 and 80,000 tons that meet the navigation requirements of the Panama Canal. Their design dimensions are strictly adapted to the maximum throughput limits of the old Panama Canal locks. They are mainly used to transport bulk commodities such as coal or grain with a capacity of 60,000 to 70,000 tons, and are the main vessel type for medium- and long-haul dry bulk trade, combining route flexibility and cargo capacity advantages. Driven by market demand, the average daily revenue of Panamax vessels also increased in tandem, rising by $472 to $18,490 on the day, an increase of about 12% compared to the same period last month, demonstrating the resilience of demand in niche transportation markets such as grain and coal.

It is worth noting that the current upward trend in the dry bulk market is closely related to the complex geopolitical situation. Philippe Guvia, shipping analysis manager at the Baltic International Maritime Council (BIMCO), stated explicitly in last week's "Shipping Market Outlook": "The Iranian war and the resulting disruption of shipping through the Strait of Hormuz have exacerbated uncertainty in the global economy and the dry bulk market." While the Strait of Hormuz is not as crucial to dry bulk shipping as oil tankers, it still handles approximately 4% of global dry bulk trade (by volume and ton-miles), involving the transport of various key commodities such as grains, iron ore, and limestone. Of this, 52% of the world's limestone is shipped from the UAE through this strait, primarily to India and Bangladesh, serving local cement and steel production.

Guvia further explained that 210 ships are currently stranded in the Persian Gulf region, representing approximately 1% of the global bulk carrier fleet. This stranding has not only strained capacity on some routes but has also further increased freight rates. According to the latest news, direct military conflict erupted between the US and Iran on May 4th, with Iran attacking ships near the Strait of Hormuz. The US retaliated immediately. Although the US military claims to have assisted some ships in navigating the strait, most ship owners are unwilling to risk passage due to lingering security risks. Currently, traffic volume in the strait is far below pre-war levels, with significantly fewer than the 130 ships passing through daily. Clearing the hundreds of stranded ships could take months.

Among the three major ship types, the Supramax sector was the only one to decline on the day, in stark contrast to the strong performance of Capesize and Panamax vessels. Specifically, the Very Large Vessels Index fell 12 points, a drop of 0.8%, closing at 1508 points. Analysts pointed out that Supramax vessels mainly undertake short-haul transportation of small dry bulk cargoes, and their transportation demand is greatly affected by regional markets. This decline was mainly due to a temporary slowdown in short-haul transportation demand in some regions, while also being less affected by the situation in the Strait of Hormuz and failing to benefit from the tight capacity of larger vessels, thus resulting in relatively weak performance.

Furthermore, volatility in the dry bulk market has also triggered related disputes within the industry. According to court documents from the London High Court, Mercuria, a globally renowned commodities trader, is suing the Baltic Exchange, alleging that it continued to publish the TD3C VLCC freight benchmark from the Middle East Gulf to China despite the near closure of the Strait of Hormuz and the inability of related shipping routes to operate normally. This allegedly caused significant distortion of the index, resulting in hundreds of millions of dollars in losses for Mercuria in physical freight contracts and freight derivatives contracts. Mercuria argues in its complaint that the Baltic Exchange should have suspended the TD3C index or recalculated the index using comparable routes that are still in operation. The Baltic Exchange, however, maintains full confidence in its index compilation process and will fight the case vigorously. This lawsuit has become another focal point amidst the current volatility in the dry bulk market.

Market analysts say that in the short term, the navigation situation in the Strait of Hormuz will remain the core variable affecting the dry bulk market. If the situation remains tense and the tight shipping capacity is difficult to alleviate, freight rates for Capesize and Panamax vessels are expected to remain high. However, in the long term, it is necessary to pay close attention to the pace of global industrial demand recovery, new ship deliveries, and changes in the geopolitical situation, as these factors will have a profound impact on the trend of the dry bulk market.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a significant surge on Tuesday, reaching its highest level in five months. This strong rise was mainly driven by the continued strength of the two core bulk carrier sectors, Capesize and Panamax, reflecting the structural recovery in the current global dry bulk shipping market and also profoundly influenced by recent geopolitical events. As a core indicator of the global dry bulk shipping market, the index directly monitors fluctuations in freight rates for ships transporting dry bulk commodities such as iron ore, coal, and grains worldwide, and its trends have historically been regarded as a "barometer" of global industrial demand and international trade activity.

Specifically, the Baltic Dry Index, which tracks freight rates for the three major bulk carrier categories—Capesize, Panamax, and Supramax—performed strongly on the day, rising 102 points, or 3.7%, to close at 2832 points. This closing level not only marked the highest point since early December 2025 but also signifies a two-month consecutive rebound since the index bottomed out in early March, with a cumulative increase of over 40%, highlighting the strong recovery momentum in the dry bulk market. Historically, the index fell to a low of 1919 points on March 10, 2026, before gradually stabilizing and rebounding, accelerating its rise since April and demonstrating a clear upward trend.

The Capesize sector was particularly strong, serving as the core engine of the index's rise. The Capesize index surged 256 points, a 5.8% increase, closing at 4703 points, its highest point in five months, becoming a key driver of the overall index's upward movement. Capesize vessels, among the world's largest bulk carriers, primarily transport dry bulk cargo of 150,000 tons and above. Their core cargoes include basic industrial raw materials such as iron ore and coal, making them a crucial link in the global steel and energy supply chains. Correspondingly, the average daily revenue of Capesize vessels (.BATCA) carrying 150,000 tons of cargo (mainly iron ore and coal) also climbed, increasing by $2,318 to reach $39,146. This revenue level represents a nearly 60% increase from the low point in early March, reflecting a significant recovery in market demand for large bulk cargo transportation.

Besides the Capesize sector, the Panamax sector also showed a steady upward trend, providing strong support for the overall index. The Panamax index rose 52 points, or 2.6%, to close at 2054 points, continuing its recent upward trend. Panamax bulk carriers are bulk carriers with a deadweight tonnage between 60,000 and 80,000 tons that meet the navigation requirements of the Panama Canal. Their design dimensions are strictly adapted to the maximum throughput limits of the old Panama Canal locks. They are mainly used to transport bulk commodities such as coal or grain with a capacity of 60,000 to 70,000 tons, and are the main vessel type for medium- and long-haul dry bulk trade, combining route flexibility and cargo capacity advantages. Driven by market demand, the average daily revenue of Panamax vessels also increased in tandem, rising by $472 to $18,490 on the day, an increase of about 12% compared to the same period last month, demonstrating the resilience of demand in niche transportation markets such as grain and coal.

It is worth noting that the current upward trend in the dry bulk market is closely related to the complex geopolitical situation. Philippe Guvia, shipping analysis manager at the Baltic International Maritime Council (BIMCO), stated explicitly in last week's "Shipping Market Outlook": "The Iranian war and the resulting disruption of shipping through the Strait of Hormuz have exacerbated uncertainty in the global economy and the dry bulk market." While the Strait of Hormuz is not as crucial to dry bulk shipping as oil tankers, it still handles approximately 4% of global dry bulk trade (by volume and ton-miles), involving the transport of various key commodities such as grains, iron ore, and limestone. Of this, 52% of the world's limestone is shipped from the UAE through this strait, primarily to India and Bangladesh, serving local cement and steel production.

Guvia further explained that 210 ships are currently stranded in the Persian Gulf region, representing approximately 1% of the global bulk carrier fleet. This stranding has not only strained capacity on some routes but has also further increased freight rates. According to the latest news, direct military conflict erupted between the US and Iran on May 4th, with Iran attacking ships near the Strait of Hormuz. The US retaliated immediately. Although the US military claims to have assisted some ships in navigating the strait, most ship owners are unwilling to risk passage due to lingering security risks. Currently, traffic volume in the strait is far below pre-war levels, with significantly fewer than the 130 ships passing through daily. Clearing the hundreds of stranded ships could take months.

Among the three major ship types, the Supramax sector was the only one to decline on the day, in stark contrast to the strong performance of Capesize and Panamax vessels. Specifically, the Very Large Vessels Index fell 12 points, a drop of 0.8%, closing at 1508 points. Analysts pointed out that Supramax vessels mainly undertake short-haul transportation of small dry bulk cargoes, and their transportation demand is greatly affected by regional markets. This decline was mainly due to a temporary slowdown in short-haul transportation demand in some regions, while also being less affected by the situation in the Strait of Hormuz and failing to benefit from the tight capacity of larger vessels, thus resulting in relatively weak performance.

Furthermore, volatility in the dry bulk market has also triggered related disputes within the industry. According to court documents from the London High Court, Mercuria, a globally renowned commodities trader, is suing the Baltic Exchange, alleging that it continued to publish the TD3C VLCC freight benchmark from the Middle East Gulf to China despite the near closure of the Strait of Hormuz and the inability of related shipping routes to operate normally. This allegedly caused significant distortion of the index, resulting in hundreds of millions of dollars in losses for Mercuria in physical freight contracts and freight derivatives contracts. Mercuria argues in its complaint that the Baltic Exchange should have suspended the TD3C index or recalculated the index using comparable routes that are still in operation. The Baltic Exchange, however, maintains full confidence in its index compilation process and will fight the case vigorously. This lawsuit has become another focal point amidst the current volatility in the dry bulk market.

Market analysts say that in the short term, the navigation situation in the Strait of Hormuz will remain the core variable affecting the dry bulk market. If the situation remains tense and the tight shipping capacity is difficult to alleviate, freight rates for Capesize and Panamax vessels are expected to remain high. However, in the long term, it is necessary to pay close attention to the pace of global industrial demand recovery, new ship deliveries, and changes in the geopolitical situation, as these factors will have a profound impact on the trend of the dry bulk market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.