Why has gold failed to function as a safe-haven asset since the Iranian conflict?

2026-05-12 20:26:20

Since the outbreak of the conflict in Iran, gold prices have fallen by about 12%—a counterintuitive move for an asset widely regarded as a crisis hedge. This sell-off is not due to gold's failure as a safe haven, but rather a result of the macroeconomic ripple effects triggered by the shock. We remain optimistic about gold's future performance and expect prices to climb to $5,000 per ounce by the end of the year.

Why did gold experience a sell-off during the conflict?

Gold's safe-haven appeal is strongest during financial crises or economic shocks—when real yields decline and the dollar weakens. However, supply-side energy shocks have the opposite effect: rising oil prices push up inflation, forcing central banks to maintain existing policies and leading to a stronger dollar, all of which put downward pressure on gold prices. Furthermore, the current ample liquidity in the market makes gold a viable source of funds for investors to offset losses in other areas.

We saw similar market dynamics after the Russia-Ukraine conflict in 2022. Gold initially rose briefly before coming under pressure as inflationary effects from rising energy prices pushed up yields and the dollar exchange rate. The market reaction in this conflict is strikingly similar, only at a faster pace.

Downward pressure at the macro level

The Federal Reserve kept interest rates unchanged in April, and Chairman Powell's remarks were also cautious. Since the outbreak of war, inflation has accelerated again, significantly reducing the likelihood of a rate cut in the short term. Our US economists still expect a rate cut in the second half of this year, but the ongoing energy shock could delay this process. Real yields and the dollar exchange rate remain key factors constraining gold price increases.

Peace negotiations provided support for recovery, but the process stalled.

Gold gave back some of last week's gains after President Trump called Iran's latest peace proposal "completely unacceptable." This setback not only made the ceasefire timetable uncertain but also kept inflation risks high—further reinforcing market expectations of persistently high interest rates, an expectation that has weighed on gold prices throughout the conflict. The ability to reach a lasting peace solution remains a key catalyst for a sustained recovery in gold prices.

On the macro level, the non-farm payroll data released last Friday showed that employers added jobs for the second consecutive month in April, with the unemployment rate remaining stable at 4.3%. This gives the Federal Reserve no reason to rush into cutting interest rates, and yields and the dollar exchange rate will continue to exert downward pressure on gold in the short term. The Consumer Price Index (CPI) data scheduled for release on Tuesday will be the next key test—if inflation again exceeds expectations, it will further solidify the current market position. In addition, Powell's term will end this week, adding another layer of uncertainty to the Fed's independence.

Central bank gold purchases are a structural pillar of the gold market.

Demand from central banks around the world continues to support the gold market. The People's Bank of China resumed gold purchases in April, increasing its holdings by 8.1 tons—the largest monthly increase since December 2024—and extending its continuous purchase cycle to 15 months, bringing its total holdings to approximately 2,305 tons.

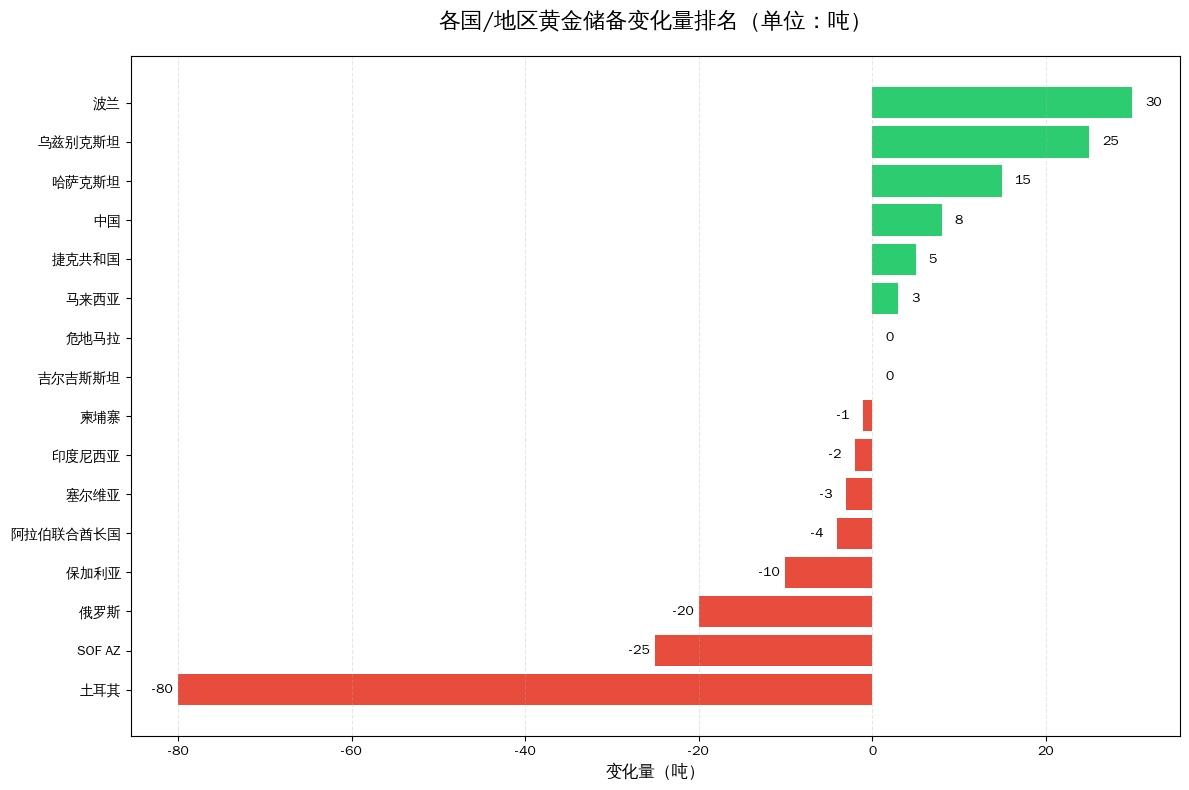

(Changes in gold reserve holdings since the beginning of the year)

Data from the World Gold Council (WGC) shows that although central banks turned into net sellers of gold in March, with net sales of approximately 30 tons, total purchases in the first quarter still reached 27 tons. Turkey was the main seller, reducing its gold holdings by 60 tons to support foreign exchange liquidity, bringing its net sales for the first quarter to 79 tons. Gold purchases remain concentrated in a few countries, with Poland increasing its holdings by 11 tons in March and a cumulative increase of 31 tons year-to-date.

In the first quarter, despite increased selling, central bank demand for gold rose 17% quarter-on-quarter, with Poland and Uzbekistan being the main buyers. The National Bank of Poland once again became the largest buyer, increasing its gold reserves by 31 tons to 582 tons during the quarter. Although the bank's governor, Adam Grapinski, recently mentioned the possibility of selling some gold, the central bank appears to remain focused on achieving its 700-ton gold reserve target.

Reports indicate that gold sales have also increased, primarily from Turkey, Russia, and Azerbaijan. According to published data, Turkey was the largest gold seller in the first quarter, with its official gold holdings decreasing by approximately 70 tons (about 10% of total official holdings). Most of the selling occurred in March, when the country's central bank used an additional 80 tons of gold through gold swaps to replenish foreign exchange and liquidity.

This indicates that while central bank demand for gold has slowed, it remains on a positive trend, and reserve diversification will continue to support gold in the medium term.

Gold ETF fund flows begin to shift

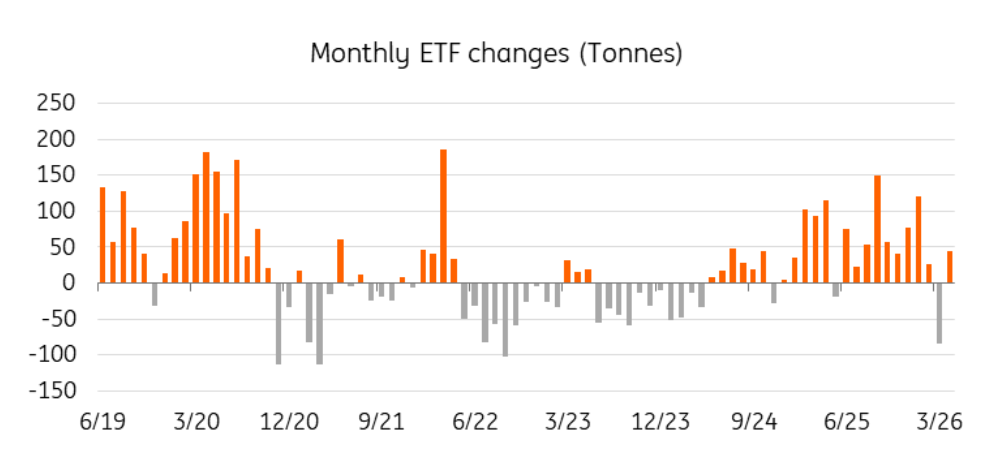

Since the outbreak of the conflict, outflows from gold ETFs have been suppressing gold prices, wiping out most of the inflows from earlier this year. However, early signs suggest that the positioning of funds is beginning to shift.

(In April, gold ETF inflows turned positive. Source: World Gold Council)

Data from the World Gold Council shows that global gold ETFs recorded inflows of approximately $6.6 billion in April, reversing the outflow trend of March. Europe was the main driving force – reflecting market concerns that the region would be more vulnerable to the closure of the Strait of Hormuz. Inflows into Asia and the United States that month were about one-third of those into Europe.

Currently, gold ETF holdings are still far below the peak in November 2020, leaving significant room for recovery. ETF fund flows are closely related to the Federal Reserve's policy expectations—a rate cut by the Fed in the second half of this year is expected to be a catalyst for renewed fund inflows.

Meanwhile, net long positions managed by funds on the New York Mercantile Exchange (COMEX) continue to indicate a positive investor sentiment, although positions have not yet reached crowded levels.

Short-term risks coexist with long-term support.

We remain optimistic about gold's performance, but the stalled peace talks have increased short-term uncertainty. Trump's rejection of Iran's latest proposal has left the ceasefire timetable unclear, and high inflation risks limit the Federal Reserve's room for interest rate cuts.

The upward path for gold prices depends on a decline in energy prices, cooling inflation, and interest rate cuts by the Federal Reserve in the second half of this year. Central bank purchases and a recovery in ETF inflows will provide additional support for gold.

We currently expect gold prices to climb to $5,000 per ounce by the end of the year. The main downside risk is that a breakdown in peace talks could lead to persistently high energy prices, forcing the Federal Reserve to maintain current interest rates until the end of the year.

Gold's safe-haven appeal is undeniable. However, recent market performance suggests that short-term price movements may still be dominated by macroeconomic factors—particularly real yields, the dollar exchange rate, and expectations regarding Federal Reserve policy. Once these downward pressures begin to ease, gold's own support will re-emerge.

Why did gold experience a sell-off during the conflict?

Gold's safe-haven appeal is strongest during financial crises or economic shocks—when real yields decline and the dollar weakens. However, supply-side energy shocks have the opposite effect: rising oil prices push up inflation, forcing central banks to maintain existing policies and leading to a stronger dollar, all of which put downward pressure on gold prices. Furthermore, the current ample liquidity in the market makes gold a viable source of funds for investors to offset losses in other areas.

We saw similar market dynamics after the Russia-Ukraine conflict in 2022. Gold initially rose briefly before coming under pressure as inflationary effects from rising energy prices pushed up yields and the dollar exchange rate. The market reaction in this conflict is strikingly similar, only at a faster pace.

Downward pressure at the macro level

The Federal Reserve kept interest rates unchanged in April, and Chairman Powell's remarks were also cautious. Since the outbreak of war, inflation has accelerated again, significantly reducing the likelihood of a rate cut in the short term. Our US economists still expect a rate cut in the second half of this year, but the ongoing energy shock could delay this process. Real yields and the dollar exchange rate remain key factors constraining gold price increases.

Peace negotiations provided support for recovery, but the process stalled.

Gold gave back some of last week's gains after President Trump called Iran's latest peace proposal "completely unacceptable." This setback not only made the ceasefire timetable uncertain but also kept inflation risks high—further reinforcing market expectations of persistently high interest rates, an expectation that has weighed on gold prices throughout the conflict. The ability to reach a lasting peace solution remains a key catalyst for a sustained recovery in gold prices.

On the macro level, the non-farm payroll data released last Friday showed that employers added jobs for the second consecutive month in April, with the unemployment rate remaining stable at 4.3%. This gives the Federal Reserve no reason to rush into cutting interest rates, and yields and the dollar exchange rate will continue to exert downward pressure on gold in the short term. The Consumer Price Index (CPI) data scheduled for release on Tuesday will be the next key test—if inflation again exceeds expectations, it will further solidify the current market position. In addition, Powell's term will end this week, adding another layer of uncertainty to the Fed's independence.

Central bank gold purchases are a structural pillar of the gold market.

Demand from central banks around the world continues to support the gold market. The People's Bank of China resumed gold purchases in April, increasing its holdings by 8.1 tons—the largest monthly increase since December 2024—and extending its continuous purchase cycle to 15 months, bringing its total holdings to approximately 2,305 tons.

(Changes in gold reserve holdings since the beginning of the year)

Data from the World Gold Council (WGC) shows that although central banks turned into net sellers of gold in March, with net sales of approximately 30 tons, total purchases in the first quarter still reached 27 tons. Turkey was the main seller, reducing its gold holdings by 60 tons to support foreign exchange liquidity, bringing its net sales for the first quarter to 79 tons. Gold purchases remain concentrated in a few countries, with Poland increasing its holdings by 11 tons in March and a cumulative increase of 31 tons year-to-date.

In the first quarter, despite increased selling, central bank demand for gold rose 17% quarter-on-quarter, with Poland and Uzbekistan being the main buyers. The National Bank of Poland once again became the largest buyer, increasing its gold reserves by 31 tons to 582 tons during the quarter. Although the bank's governor, Adam Grapinski, recently mentioned the possibility of selling some gold, the central bank appears to remain focused on achieving its 700-ton gold reserve target.

Reports indicate that gold sales have also increased, primarily from Turkey, Russia, and Azerbaijan. According to published data, Turkey was the largest gold seller in the first quarter, with its official gold holdings decreasing by approximately 70 tons (about 10% of total official holdings). Most of the selling occurred in March, when the country's central bank used an additional 80 tons of gold through gold swaps to replenish foreign exchange and liquidity.

This indicates that while central bank demand for gold has slowed, it remains on a positive trend, and reserve diversification will continue to support gold in the medium term.

Gold ETF fund flows begin to shift

Since the outbreak of the conflict, outflows from gold ETFs have been suppressing gold prices, wiping out most of the inflows from earlier this year. However, early signs suggest that the positioning of funds is beginning to shift.

(In April, gold ETF inflows turned positive. Source: World Gold Council)

Data from the World Gold Council shows that global gold ETFs recorded inflows of approximately $6.6 billion in April, reversing the outflow trend of March. Europe was the main driving force – reflecting market concerns that the region would be more vulnerable to the closure of the Strait of Hormuz. Inflows into Asia and the United States that month were about one-third of those into Europe.

Currently, gold ETF holdings are still far below the peak in November 2020, leaving significant room for recovery. ETF fund flows are closely related to the Federal Reserve's policy expectations—a rate cut by the Fed in the second half of this year is expected to be a catalyst for renewed fund inflows.

Meanwhile, net long positions managed by funds on the New York Mercantile Exchange (COMEX) continue to indicate a positive investor sentiment, although positions have not yet reached crowded levels.

Short-term risks coexist with long-term support.

We remain optimistic about gold's performance, but the stalled peace talks have increased short-term uncertainty. Trump's rejection of Iran's latest proposal has left the ceasefire timetable unclear, and high inflation risks limit the Federal Reserve's room for interest rate cuts.

The upward path for gold prices depends on a decline in energy prices, cooling inflation, and interest rate cuts by the Federal Reserve in the second half of this year. Central bank purchases and a recovery in ETF inflows will provide additional support for gold.

We currently expect gold prices to climb to $5,000 per ounce by the end of the year. The main downside risk is that a breakdown in peace talks could lead to persistently high energy prices, forcing the Federal Reserve to maintain current interest rates until the end of the year.

Gold's safe-haven appeal is undeniable. However, recent market performance suggests that short-term price movements may still be dominated by macroeconomic factors—particularly real yields, the dollar exchange rate, and expectations regarding Federal Reserve policy. Once these downward pressures begin to ease, gold's own support will re-emerge.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.