Warsh's Fed strategy: Who benefits and who suffers, and why does it point to interest rate cuts?

2026-05-13 19:22:09

With Kevin Warsh set to take the helm of the Federal Reserve in 2026, global financial markets are undergoing a paradigm shift.

While mainstream economists are still debating whether he will succumb to pressure from the White House to cut interest rates, we find that Walsh is implementing a more far-sighted plan: to use the “steepened” yield curve to achieve a critical balance between protecting the dollar’s credit and resolving government debt.

While the Federal Reserve is primarily responsible to Congress for addressing employment and inflation, it appears that the core reason Trump has been pressuring the Fed is that excessively high government financing costs limit the White House's actions. Warsh's appointment may be subtly aimed at resolving this contradiction, which is likely why Trump recommended him.

Over the past decade, the Federal Reserve has tended to use quantitative easing (QE) to lower long-term interest rates in an attempt to stimulate the economy.

Walsh's operational logic is the complete opposite: he is leading a "reverse reversal"—suppressing the short end and letting the long end run free.

Warsh's first action after taking office was to guide short-term interest rates (Fed Funds Rate) downward, not simply to stimulate consumption, but for fiscal emergency relief.

The U.S. government is currently facing enormous pressure from rolling short-term debt. By lowering short-term interest rates, Walsh directly reduced the cost for the Treasury to issue Treasury bills (T-Bills), preventing interest payments from completely overwhelming the federal budget.

The market generally believes that this is Walsh compromising with political pressure, but he is actually carrying out systemic stability maintenance under "fiscal dominance".

Unlike his approach of suppressing short-term yields, Walsh showed a high degree of tolerance for long-term Treasury yields (such as 10-year and 30-year bonds), and even actively reduced his intervention.

Maintaining high long-term yields can provide global investors with sufficient "term premiums." When the US dollar faces depreciation risks, high-yield long-term bonds are the last anchor point for retaining international capital and preventing the collapse of the US dollar index.

However, this operation led to a sharp steepening of the yield curve, which would increase corporate financing costs and mortgage pressures. But here Walsh was very clever. Knowing that the government's financing costs were high, he still chose to shrink the balance sheet and let long-term interest rates continue to rise. His purpose was to maintain the independence of the Federal Reserve while making the government bear part of the long-term debt costs, but secretly protecting the government's ability to issue a large amount of low-interest bonds (T-Bills) at the short end without causing financial turmoil.

In Warsh's interest rate blueprint, steepening the curve is essentially a "directed sacrifice".

He ruthlessly reshaped wealth among different groups by artificially creating interest rate differentials between short-term and long-term markets:

Government reduces burden, depositors foot the bill: Warsh forcefully lowers short-term interest rates, allowing the Treasury to "extend life" for massive short-term debt at extremely low cost.

However, this directly dilutes the deposit returns for ordinary depositors, essentially using private interest income to "fill the hole" of the government deficit.

Banks profit, zombies are cleared out: Steep interest rate spreads provide commercial banks with lucrative profit margins, preserving the balance sheets of the financial system.

However, those "zombie companies" that rely on cheap leverage to survive will naturally perish due to blood loss under the pressure of strong long-term interest rates.

The dollar's preservation of value puts pressure on essential housing needs: In order to stabilize the dollar index and attract foreign investment, long-term interest rates must remain high as a "credibility anchor." This means that the dollar's international status is preserved, but domestic homebuyers with essential housing needs and long-term investment enterprises have to bear heavy mortgage and financing burdens, becoming the most direct price of maintaining the dollar's hegemony.

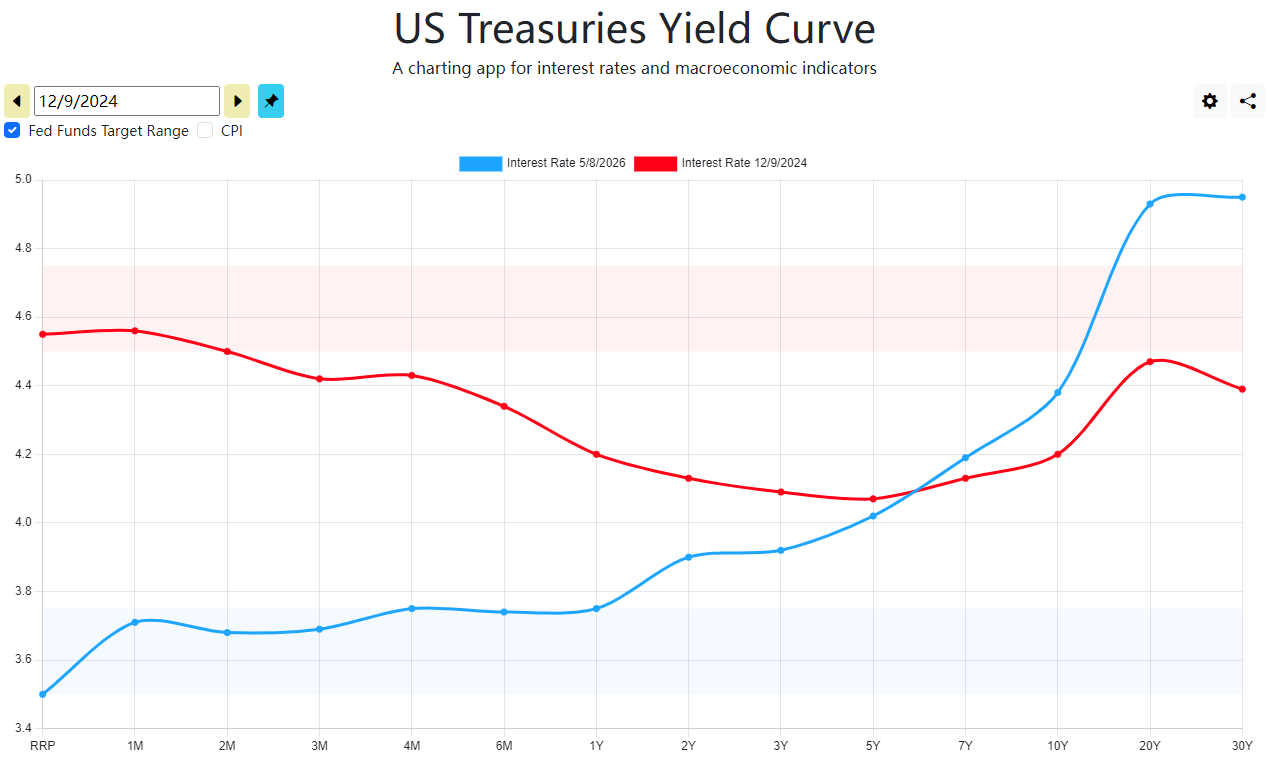

(The U.S. Treasury yield curve continues to steepen. Source: Federal Reserve)

Faced with the potential economic drain caused by high long-term borrowing costs, Walsh did not choose to resort to massive quantitative easing, but instead played two entirely new cards:

The AI productivity narrative: Walsh vigorously promotes the role of AI in boosting productivity. His logic is that even if corporate borrowing costs are 6%, if AI can bring a 10% efficiency improvement, then high interest rates are "healthy," which provides a legitimate explanation for maintaining a high-interest environment.

Administrative cost replacement: In line with the Republican-backed "deregulation" wave, Walsh advocated offsetting rising interest expenses by reducing compliance and entry costs for businesses.

Mainstream economists are concerned with whether Warsh undermined the Fed's independence, but what we see is an extremely pragmatic "financial engineer."

Under Warsh's leadership, the interest rate trajectory will no longer be driven by a single inflation data point (he himself will also change the data the Fed tracks, instead of traditional data such as PCE), but will take into account government financing costs, interest rate levels, and independence.

In this model, a steeper yield curve may become the norm, and the Federal Reserve will no longer try to save every borrower. Instead, it will sacrifice some interest rate-sensitive sectors (such as real estate and traditional manufacturing) in exchange for the continuation of the US government debt system and the last vestige of dignity of the dollar as the global reserve currency.

Meanwhile, within this framework, given the US's balance sheet reduction and the change in the PCE index that the Federal Reserve previously tracked, its argument for interest rate cuts has already offset the market liquidity losses caused by the balance sheet reduction. Furthermore, by tracking the new cut-off average PCE inflation rate (which has been declining recently), it demonstrates that the interest rate cut is based on data. Therefore, the conclusion to cut interest rates is justifiable, which may be one of the most important conclusions of this article.

While mainstream economists are still debating whether he will succumb to pressure from the White House to cut interest rates, we find that Walsh is implementing a more far-sighted plan: to use the “steepened” yield curve to achieve a critical balance between protecting the dollar’s credit and resolving government debt.

While the Federal Reserve is primarily responsible to Congress for addressing employment and inflation, it appears that the core reason Trump has been pressuring the Fed is that excessively high government financing costs limit the White House's actions. Warsh's appointment may be subtly aimed at resolving this contradiction, which is likely why Trump recommended him.

Policy Core: A Strategic Shift from "Smooth" to "Steep"

Over the past decade, the Federal Reserve has tended to use quantitative easing (QE) to lower long-term interest rates in an attempt to stimulate the economy.

Walsh's operational logic is the complete opposite: he is leading a "reverse reversal"—suppressing the short end and letting the long end run free.

Warsh's first action after taking office was to guide short-term interest rates (Fed Funds Rate) downward, not simply to stimulate consumption, but for fiscal emergency relief.

The U.S. government is currently facing enormous pressure from rolling short-term debt. By lowering short-term interest rates, Walsh directly reduced the cost for the Treasury to issue Treasury bills (T-Bills), preventing interest payments from completely overwhelming the federal budget.

The market generally believes that this is Walsh compromising with political pressure, but he is actually carrying out systemic stability maintenance under "fiscal dominance".

Long-term interest rates: the "moat" protecting the dollar's creditworthiness.

Unlike his approach of suppressing short-term yields, Walsh showed a high degree of tolerance for long-term Treasury yields (such as 10-year and 30-year bonds), and even actively reduced his intervention.

Maintaining high long-term yields can provide global investors with sufficient "term premiums." When the US dollar faces depreciation risks, high-yield long-term bonds are the last anchor point for retaining international capital and preventing the collapse of the US dollar index.

However, this operation led to a sharp steepening of the yield curve, which would increase corporate financing costs and mortgage pressures. But here Walsh was very clever. Knowing that the government's financing costs were high, he still chose to shrink the balance sheet and let long-term interest rates continue to rise. His purpose was to maintain the independence of the Federal Reserve while making the government bear part of the long-term debt costs, but secretly protecting the government's ability to issue a large amount of low-interest bonds (T-Bills) at the short end without causing financial turmoil.

The “cost exchange” under the Walsh logic: A precise financial reshuffle

In Warsh's interest rate blueprint, steepening the curve is essentially a "directed sacrifice".

He ruthlessly reshaped wealth among different groups by artificially creating interest rate differentials between short-term and long-term markets:

Government reduces burden, depositors foot the bill: Warsh forcefully lowers short-term interest rates, allowing the Treasury to "extend life" for massive short-term debt at extremely low cost.

However, this directly dilutes the deposit returns for ordinary depositors, essentially using private interest income to "fill the hole" of the government deficit.

Banks profit, zombies are cleared out: Steep interest rate spreads provide commercial banks with lucrative profit margins, preserving the balance sheets of the financial system.

However, those "zombie companies" that rely on cheap leverage to survive will naturally perish due to blood loss under the pressure of strong long-term interest rates.

The dollar's preservation of value puts pressure on essential housing needs: In order to stabilize the dollar index and attract foreign investment, long-term interest rates must remain high as a "credibility anchor." This means that the dollar's international status is preserved, but domestic homebuyers with essential housing needs and long-term investment enterprises have to bear heavy mortgage and financing burdens, becoming the most direct price of maintaining the dollar's hegemony.

(The U.S. Treasury yield curve continues to steepen. Source: Federal Reserve)

Remedying the Situation: AI Productivity and Regulatory Dividends

Faced with the potential economic drain caused by high long-term borrowing costs, Walsh did not choose to resort to massive quantitative easing, but instead played two entirely new cards:

The AI productivity narrative: Walsh vigorously promotes the role of AI in boosting productivity. His logic is that even if corporate borrowing costs are 6%, if AI can bring a 10% efficiency improvement, then high interest rates are "healthy," which provides a legitimate explanation for maintaining a high-interest environment.

Administrative cost replacement: In line with the Republican-backed "deregulation" wave, Walsh advocated offsetting rising interest expenses by reducing compliance and entry costs for businesses.

Conclusion: An Opaque "Soft Landing"

Mainstream economists are concerned with whether Warsh undermined the Fed's independence, but what we see is an extremely pragmatic "financial engineer."

Under Warsh's leadership, the interest rate trajectory will no longer be driven by a single inflation data point (he himself will also change the data the Fed tracks, instead of traditional data such as PCE), but will take into account government financing costs, interest rate levels, and independence.

In this model, a steeper yield curve may become the norm, and the Federal Reserve will no longer try to save every borrower. Instead, it will sacrifice some interest rate-sensitive sectors (such as real estate and traditional manufacturing) in exchange for the continuation of the US government debt system and the last vestige of dignity of the dollar as the global reserve currency.

Meanwhile, within this framework, given the US's balance sheet reduction and the change in the PCE index that the Federal Reserve previously tracked, its argument for interest rate cuts has already offset the market liquidity losses caused by the balance sheet reduction. Furthermore, by tracking the new cut-off average PCE inflation rate (which has been declining recently), it demonstrates that the interest rate cut is based on data. Therefore, the conclusion to cut interest rates is justifiable, which may be one of the most important conclusions of this article.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.