Marginal improvement in the US-Iran conflict is unlikely to change the main trend of market interest rates.

2026-05-15 21:44:35

The recent conflict between the US and Iran presents a delicate situation of "negotiations stalled but the ceasefire continued": Iranian Foreign Minister Araqchi confirmed at the BRICS foreign ministers' meeting that he had received a letter from the US requesting continued mediation in the negotiations. Iran is maintaining the ceasefire to allow for diplomatic opportunities, but is also prepared to return to the battlefield. He emphasized that he has "no trust" in the US and criticized the US for releasing "contradictory messages" that have led to the stagnation of negotiations.

US President Trump set conditions, demanding that Iran suspend uranium enrichment for 20 years and "fully comply with the agreement," while vetoing Iran's proposed solution to the conflict and reiterating his position that "Iran will never acquire nuclear weapons."

Despite ongoing geopolitical tensions, market sensitivity to this conflict has significantly decreased, with funds gradually shifting back to global central bank policies and economic fundamentals. The Federal Reserve's interest rate decisions have become the core logic for current market pricing.

The market's focus has shifted to the core context of the Federal Reserve's policies, which is characterized by sticky inflation and relative stability in the US job market.

The latest data shows that the U.S. Consumer Price Index (CPI) rose 3.8% year-on-year in April, a new high since May 2023, while the core CPI also rose to 2.8% year-on-year. The New York Fed’s May manufacturing report shows that the price paid index jumped to 62.6, the peak of this cycle, reflecting a sharp rise in corporate cost pressures.

Although the employment situation has slowed slightly—the manufacturing employment index fell from 9.8 to 8.3—the unemployment rate remained stable at 4.3%, and the number of new jobs created far exceeded market expectations, presenting an overall combination of "high inflation and stable employment."

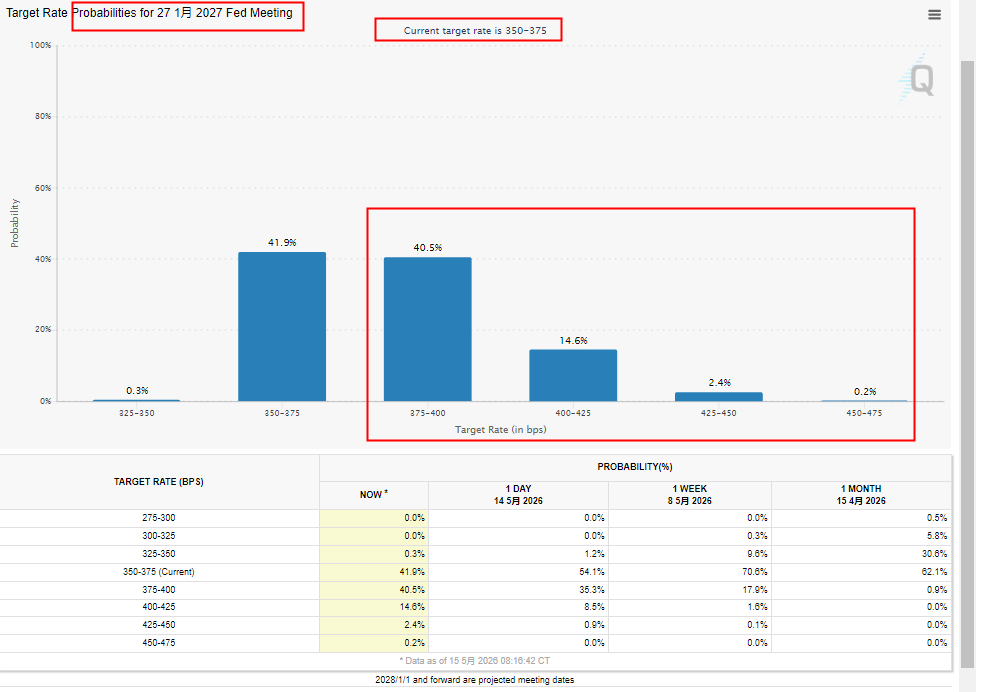

Against this backdrop, data from U.S. federal funds rate futures show that the market expects a greater than 50% probability of a Fed rate hike in January, completely reversing the easing expectations at the beginning of the year.

(CME interest rate futures, source: CME Group)

Inflationary pressures and expectations of interest rate hikes directly push up US Treasury yields and exacerbate their volatility.

The benchmark 10-year Treasury yield had previously risen to 4.548%, while the 30-year Treasury yield remained above 5% for three consecutive days, once reaching a high of 5.046%, mainly supported by the term premium pushed up by the pressure of the US fiscal deficit.

Despite the New York manufacturing sentiment index recording its strongest performance in recent times at +19.6 and the new orders index rising to +22.7 indicating expanding demand, soaring oil prices and safe-haven demand triggered by Trump's tariff rhetoric continue to constrain the US Treasury market. Strong economic data may keep yields high, further increasing the risk of two-way volatility in the future.

Regarding the current direction of monetary policy, Federal Reserve official Williams gave a neutral statement, believing that the current monetary policy is "slightly tight but in good shape overall," and clearly stated that "there is no reason to raise or lower interest rates."

At the same time, Williams understands the market's optimism about the future of the economy, pointing out that the stock market's high level is not surprising given investor expectations, and expects productivity growth to remain strong.

This statement reflects the Federal Reserve's recognition of the current economic fundamentals and also suggests that policy will remain stable in the short term to avoid hasty adjustments.

Several institutions have raised their expectations for Federal Reserve rate hikes. Carol Kong, a foreign exchange strategist at the Commonwealth Bank of Australia, explicitly stated that the high inflation data released this week is unlikely to gain the approval of FOMC officials and incoming Fed Chairman Warsh. Kong predicts that the Fed will begin a new rate hike cycle in December 2026, with this cycle expected to involve three rate hikes.

It is worth noting that although the newly appointed Federal Reserve Chairman Warsh had supported interest rate cuts, he emphasized at his nomination hearing that "the Fed's independence needs to be fought for" and did not promise to cut interest rates as Trump demanded. Moreover, the current stickiness of inflation and the supply shock brought about by geopolitical conflicts have significantly compressed the Fed's room for easing policies, further strengthening institutions' expectations for interest rate hikes.

Rising expectations of a Federal Reserve rate hike are becoming a significant support for the US dollar. Previously, the market widely bet on a Fed rate cut this year, but with high inflation and a reversal in rate hike expectations, the dollar index is expected to gain sustained momentum—the high-interest-rate environment will enhance the attractiveness of dollar assets, attracting global funds back to the US, thereby putting pressure on non-US currencies.

As mentioned in previous articles, with Warsh being the Fed chairman with the most split vote in history, and the previous chairman Powell unusually remaining in office, the Fed's independence is highly guaranteed . For global assets, the Fed's tone of "maintaining high interest rates for longer" and the start of the interest rate hike cycle mean that the global asset pricing system will usher in a new round of revaluation. Stock, bond, and foreign exchange markets will all need to readjust to a higher cost of capital environment, and the strength of the US dollar will be one of the core clues running through this round of asset revaluation.

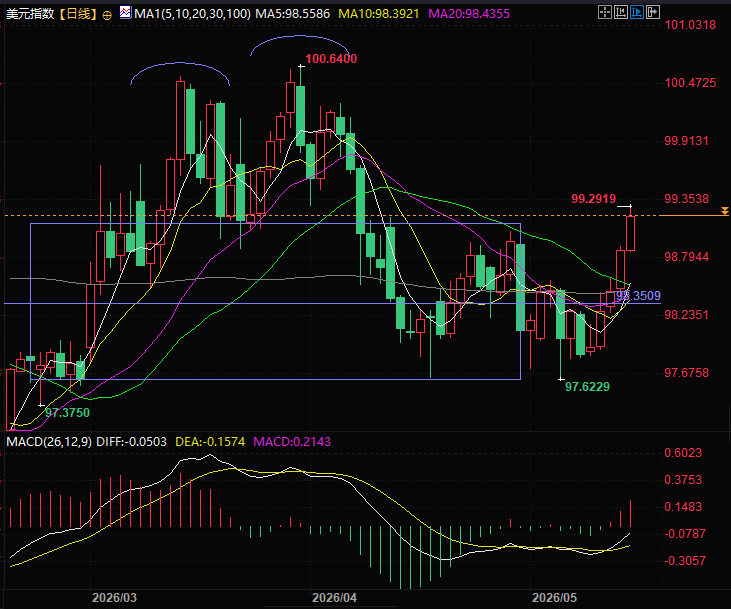

From a technical perspective, the US dollar index rebounded rapidly after touching the bottom of its trading range and has continued to rise. It has now broken through the top of the range. It must be acknowledged that the US dollar has consistently shown resilience in areas where the market is not optimistic.

(US Dollar Index Daily Chart, Source: EasyForex)

At 21:42 Beijing time, the US dollar index is currently at 99.22.

US President Trump set conditions, demanding that Iran suspend uranium enrichment for 20 years and "fully comply with the agreement," while vetoing Iran's proposed solution to the conflict and reiterating his position that "Iran will never acquire nuclear weapons."

Despite ongoing geopolitical tensions, market sensitivity to this conflict has significantly decreased, with funds gradually shifting back to global central bank policies and economic fundamentals. The Federal Reserve's interest rate decisions have become the core logic for current market pricing.

Inflation and employment are driving growth simultaneously, with the probability of a January rate hike exceeding 50%.

The market's focus has shifted to the core context of the Federal Reserve's policies, which is characterized by sticky inflation and relative stability in the US job market.

The latest data shows that the U.S. Consumer Price Index (CPI) rose 3.8% year-on-year in April, a new high since May 2023, while the core CPI also rose to 2.8% year-on-year. The New York Fed’s May manufacturing report shows that the price paid index jumped to 62.6, the peak of this cycle, reflecting a sharp rise in corporate cost pressures.

Although the employment situation has slowed slightly—the manufacturing employment index fell from 9.8 to 8.3—the unemployment rate remained stable at 4.3%, and the number of new jobs created far exceeded market expectations, presenting an overall combination of "high inflation and stable employment."

Against this backdrop, data from U.S. federal funds rate futures show that the market expects a greater than 50% probability of a Fed rate hike in January, completely reversing the easing expectations at the beginning of the year.

(CME interest rate futures, source: CME Group)

US Treasury yields are fluctuating at high levels, increasing the risk of two-way volatility.

Inflationary pressures and expectations of interest rate hikes directly push up US Treasury yields and exacerbate their volatility.

The benchmark 10-year Treasury yield had previously risen to 4.548%, while the 30-year Treasury yield remained above 5% for three consecutive days, once reaching a high of 5.046%, mainly supported by the term premium pushed up by the pressure of the US fiscal deficit.

Despite the New York manufacturing sentiment index recording its strongest performance in recent times at +19.6 and the new orders index rising to +22.7 indicating expanding demand, soaring oil prices and safe-haven demand triggered by Trump's tariff rhetoric continue to constrain the US Treasury market. Strong economic data may keep yields high, further increasing the risk of two-way volatility in the future.

Federal Reserve officials adopted a neutral stance, emphasizing that policy is in a "good state."

Regarding the current direction of monetary policy, Federal Reserve official Williams gave a neutral statement, believing that the current monetary policy is "slightly tight but in good shape overall," and clearly stated that "there is no reason to raise or lower interest rates."

At the same time, Williams understands the market's optimism about the future of the economy, pointing out that the stock market's high level is not surprising given investor expectations, and expects productivity growth to remain strong.

This statement reflects the Federal Reserve's recognition of the current economic fundamentals and also suggests that policy will remain stable in the short term to avoid hasty adjustments.

Institutions are bullish on the interest rate hike cycle, predicting three rate hikes will begin in December.

Several institutions have raised their expectations for Federal Reserve rate hikes. Carol Kong, a foreign exchange strategist at the Commonwealth Bank of Australia, explicitly stated that the high inflation data released this week is unlikely to gain the approval of FOMC officials and incoming Fed Chairman Warsh. Kong predicts that the Fed will begin a new rate hike cycle in December 2026, with this cycle expected to involve three rate hikes.

It is worth noting that although the newly appointed Federal Reserve Chairman Warsh had supported interest rate cuts, he emphasized at his nomination hearing that "the Fed's independence needs to be fought for" and did not promise to cut interest rates as Trump demanded. Moreover, the current stickiness of inflation and the supply shock brought about by geopolitical conflicts have significantly compressed the Fed's room for easing policies, further strengthening institutions' expectations for interest rate hikes.

Summary and Technical Analysis:

Rising expectations of a Federal Reserve rate hike are becoming a significant support for the US dollar. Previously, the market widely bet on a Fed rate cut this year, but with high inflation and a reversal in rate hike expectations, the dollar index is expected to gain sustained momentum—the high-interest-rate environment will enhance the attractiveness of dollar assets, attracting global funds back to the US, thereby putting pressure on non-US currencies.

As mentioned in previous articles, with Warsh being the Fed chairman with the most split vote in history, and the previous chairman Powell unusually remaining in office, the Fed's independence is highly guaranteed . For global assets, the Fed's tone of "maintaining high interest rates for longer" and the start of the interest rate hike cycle mean that the global asset pricing system will usher in a new round of revaluation. Stock, bond, and foreign exchange markets will all need to readjust to a higher cost of capital environment, and the strength of the US dollar will be one of the core clues running through this round of asset revaluation.

From a technical perspective, the US dollar index rebounded rapidly after touching the bottom of its trading range and has continued to rise. It has now broken through the top of the range. It must be acknowledged that the US dollar has consistently shown resilience in areas where the market is not optimistic.

(US Dollar Index Daily Chart, Source: EasyForex)

At 21:42 Beijing time, the US dollar index is currently at 99.22.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.