Warsh at the helm of the Federal Reserve: Key shifts in the bond market and investment strategies

2026-05-19 21:24:11

Kevin Warsh's official appointment as Chairman of the Federal Reserve marks a profound shift in the monetary policy framework of the world's largest economy.

For bond investors, this leadership change is not only about the direction of the Federal Reserve's policy independence, but will also reshape the bond pricing logic from three dimensions: inflation measurement, policy communication, and crisis response, thereby affecting the risk-return structure of asset allocation.

While Warsh explicitly pledged to maintain the operational independence of the Federal Open Market Committee (FOMC) and emphasized that interest rate decisions would be free from political interference, his consistent criticism of the Fed's current policy framework echoed some of President Donald Trump's policy concerns, raising market anxieties about the risks of "fiscal dominance."

This concern is not unfounded—if monetary policy ultimately tilts toward government spending plans, growth targets, and trade priorities, bond investors may demand a higher risk premium to compensate for the uncertainty.

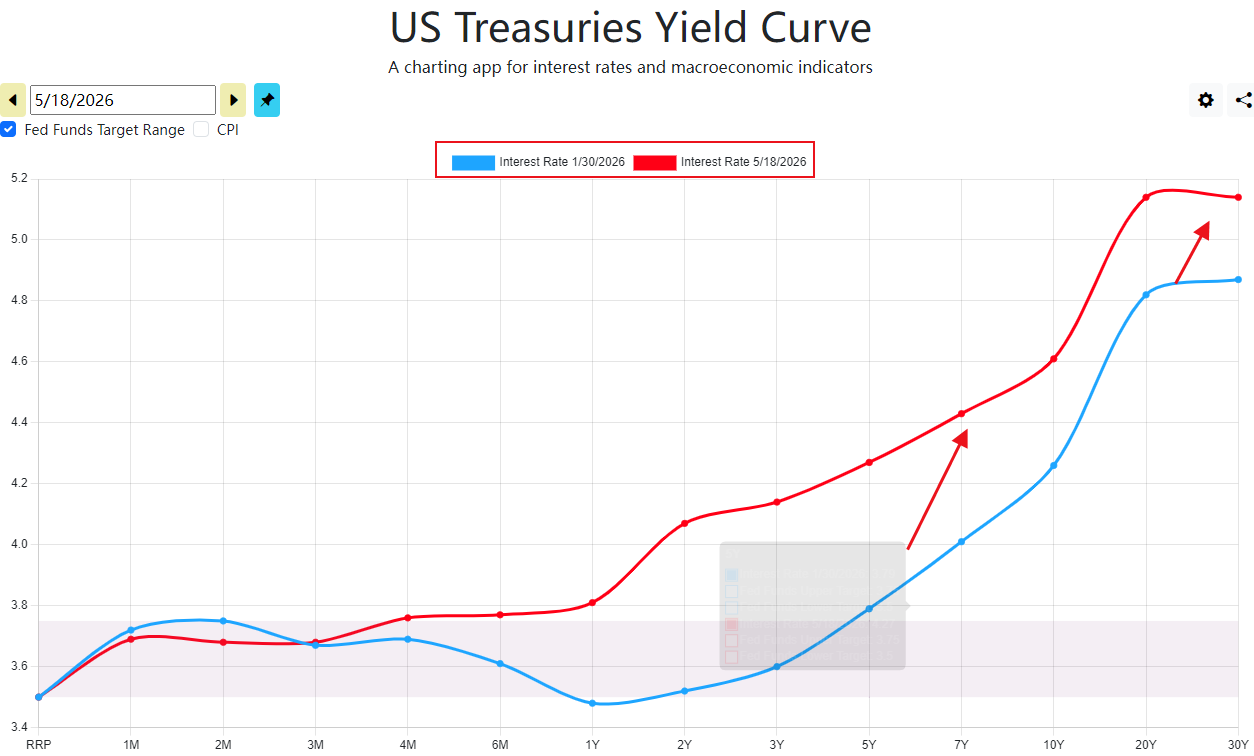

This expectation has already begun to spread to the market and may trigger a chain reaction, such as rising US Treasury term premiums, a steeper yield curve, and increased volatility in the US dollar exchange rate. Long-term bonds will be the first to bear the valuation pressure.

(The US Treasury yield curve has been steepening year-to-date. Source: Federal Reserve)

Warsh's reforms to inflation metrics are a key variable influencing the path of interest rates.

He plans to abandon the Federal Reserve's current Personal Consumption Expenditures (PCE) price index and instead adopt a "cut-off mean inflation" or "median inflation" indicator.

This indicator, by removing inflation data with extreme volatility, can effectively smooth out short-term disturbances. It currently records a reading of 2.3%, which is more than 0.5 percentage points lower than the core PCE, marking the largest difference since the pandemic and bringing it closer to the policy target of 2%.

Judging solely from the characteristics of the indicators, this shift itself implies that the Federal Reserve may maintain a lower interest rate level, providing theoretical support for interest rate cuts.

However, the market should not simply anticipate the arrival of a large-scale interest rate cut wave.

Warsh also advocated abandoning the "average inflation targeting" approach and implementing a stricter inflation control framework—the Fed would be more inclined to raise interest rates once inflation deviates from the 2% target ceiling.

Given the current macroeconomic backdrop of rising energy prices, the most likely scenario is that the Federal Reserve will maintain high real interest rates for an extended period, which will continue to drive bond yields and the dollar exchange rate upward, further amplifying the interest rate risk of long-term bonds.

Another core argument of Warsh's is to abolish the "forward guidance" mechanism, ending the communication model since the 2008 financial crisis in which the Federal Reserve clearly conveys the path of interest rates through tools such as the "dot plot".

In his view, this “over-communication” would restrict policy flexibility and make it difficult to respond quickly when new economic data calls for adjustments to policy direction.

This reform will significantly change the pricing logic of the bond market: the uncertainty of the policy path during the interval between FOMC interest rate decisions will increase significantly, and the volatility of interest rates for short-term fixed-income products with a maturity of less than two years will rise significantly.

With the Federal Reserve reducing the frequency of its communications and decreasing the clarity of its statements, every economic data release and FOMC meeting will become a key information juncture, significantly increasing the risk of sudden market fluctuations.

Historical experience shows that the three to six months following a change of Federal Reserve chair is a period of high volatility, with the S&P 500 index experiencing an average maximum drawdown of 13.14%. The vulnerability of the bond market is also worth noting – the US Treasury market has recently experienced several sharp fluctuations, and the removal of forward guidance may further exacerbate this trend.

Warsh is explicitly critical of the Federal Reserve's current $7 trillion holding of Treasury bonds, advocates for accelerating the balance sheet reduction process, and is lukewarm towards unconventional policy tools such as quantitative easing.

This means that the "central bank bailout" safety net that the bond market has relied on since 2008 may be substantially weakened, and the Federal Reserve's willingness and strength to provide liquidity support will decrease when the market experiences severe turmoil.

In the long run, the balance sheet reduction process, coupled with liquidity rules requiring banks to increase their holdings of treasury bills and reduce reserves, will force private investors to take on more fixed-income securities with longer maturities and greater risk exposure.

This trend will drive the term premium of US bonds into a structural upward channel. The yield on 30-year US Treasury bonds has already broken through 5.15%, and Barclays strategists warn that it may further rise to a new high of 5.5% since 2004. A steeper yield curve will become the new normal in the market.

Faced with Warsh's new Fed policies and doubts about the Fed's independence (which could also lead to steeper Treasury yields), bond investors holding diversified portfolios of sovereign, corporate, and emerging market bonds do not need to make radical adjustments to their portfolios. However, they need to manage risks and seize opportunities through sophisticated operations. At the same time, fluctuations in bond yields will also affect the performance of major asset classes.

Investors need to proactively reduce their exposure to interest rate risk and focus on short-duration bonds. Duration is a core indicator for measuring the sensitivity of bond prices to interest rate changes; the longer the duration, the higher the risk. Against the backdrop of controversies surrounding central bank independence and rising risks associated with fiscal dominance, long-duration bonds will bear the most direct negative impact.

Shifting to shorter-duration instruments can effectively mitigate the risk of valuation declines caused by rising interest rates, while also improving the efficiency of capital inflows.

At the same time, a steep yield curve will also affect long-term assets such as gold and technology stocks, and the recent correction is partly due to the influence of Walsh's appointment.

In summary, the Federal Reserve under Warsh's leadership is pushing for a comprehensive restructuring of its monetary policy framework, and the bond market will face multiple changes, including uncertainty about the interest rate path, increased volatility, and rising term premiums.

Investors should base their portfolios on a short-duration, defensive, and well-structured approach, seizing structural opportunities in the market while controlling risk.

(Daily chart of the yield on 30-year US Treasury bonds, source: EasyTrade)

For bond investors, this leadership change is not only about the direction of the Federal Reserve's policy independence, but will also reshape the bond pricing logic from three dimensions: inflation measurement, policy communication, and crisis response, thereby affecting the risk-return structure of asset allocation.

Policy independence controversy: Implicit risks in interest rate pricing

While Warsh explicitly pledged to maintain the operational independence of the Federal Open Market Committee (FOMC) and emphasized that interest rate decisions would be free from political interference, his consistent criticism of the Fed's current policy framework echoed some of President Donald Trump's policy concerns, raising market anxieties about the risks of "fiscal dominance."

This concern is not unfounded—if monetary policy ultimately tilts toward government spending plans, growth targets, and trade priorities, bond investors may demand a higher risk premium to compensate for the uncertainty.

This expectation has already begun to spread to the market and may trigger a chain reaction, such as rising US Treasury term premiums, a steeper yield curve, and increased volatility in the US dollar exchange rate. Long-term bonds will be the first to bear the valuation pressure.

(The US Treasury yield curve has been steepening year-to-date. Source: Federal Reserve)

Shifting Inflation Metrics: A Dual Game Between Interest Rate Cut Expectations and Interest Rate Hike Risks

Warsh's reforms to inflation metrics are a key variable influencing the path of interest rates.

He plans to abandon the Federal Reserve's current Personal Consumption Expenditures (PCE) price index and instead adopt a "cut-off mean inflation" or "median inflation" indicator.

This indicator, by removing inflation data with extreme volatility, can effectively smooth out short-term disturbances. It currently records a reading of 2.3%, which is more than 0.5 percentage points lower than the core PCE, marking the largest difference since the pandemic and bringing it closer to the policy target of 2%.

Judging solely from the characteristics of the indicators, this shift itself implies that the Federal Reserve may maintain a lower interest rate level, providing theoretical support for interest rate cuts.

However, the market should not simply anticipate the arrival of a large-scale interest rate cut wave.

Warsh also advocated abandoning the "average inflation targeting" approach and implementing a stricter inflation control framework—the Fed would be more inclined to raise interest rates once inflation deviates from the 2% target ceiling.

Given the current macroeconomic backdrop of rising energy prices, the most likely scenario is that the Federal Reserve will maintain high real interest rates for an extended period, which will continue to drive bond yields and the dollar exchange rate upward, further amplifying the interest rate risk of long-term bonds.

Communication mechanism reform: the "amplifier" effect of market fluctuations

Another core argument of Warsh's is to abolish the "forward guidance" mechanism, ending the communication model since the 2008 financial crisis in which the Federal Reserve clearly conveys the path of interest rates through tools such as the "dot plot".

In his view, this “over-communication” would restrict policy flexibility and make it difficult to respond quickly when new economic data calls for adjustments to policy direction.

This reform will significantly change the pricing logic of the bond market: the uncertainty of the policy path during the interval between FOMC interest rate decisions will increase significantly, and the volatility of interest rates for short-term fixed-income products with a maturity of less than two years will rise significantly.

With the Federal Reserve reducing the frequency of its communications and decreasing the clarity of its statements, every economic data release and FOMC meeting will become a key information juncture, significantly increasing the risk of sudden market fluctuations.

Historical experience shows that the three to six months following a change of Federal Reserve chair is a period of high volatility, with the S&P 500 index experiencing an average maximum drawdown of 13.14%. The vulnerability of the bond market is also worth noting – the US Treasury market has recently experienced several sharp fluctuations, and the removal of forward guidance may further exacerbate this trend.

Balance Sheet Reduction and Crisis Response: Reconstructing the "Safety Net" for the Bond Market

Warsh is explicitly critical of the Federal Reserve's current $7 trillion holding of Treasury bonds, advocates for accelerating the balance sheet reduction process, and is lukewarm towards unconventional policy tools such as quantitative easing.

This means that the "central bank bailout" safety net that the bond market has relied on since 2008 may be substantially weakened, and the Federal Reserve's willingness and strength to provide liquidity support will decrease when the market experiences severe turmoil.

In the long run, the balance sheet reduction process, coupled with liquidity rules requiring banks to increase their holdings of treasury bills and reduce reserves, will force private investors to take on more fixed-income securities with longer maturities and greater risk exposure.

This trend will drive the term premium of US bonds into a structural upward channel. The yield on 30-year US Treasury bonds has already broken through 5.15%, and Barclays strategists warn that it may further rise to a new high of 5.5% since 2004. A steeper yield curve will become the new normal in the market.

Summary of major categories

Faced with Warsh's new Fed policies and doubts about the Fed's independence (which could also lead to steeper Treasury yields), bond investors holding diversified portfolios of sovereign, corporate, and emerging market bonds do not need to make radical adjustments to their portfolios. However, they need to manage risks and seize opportunities through sophisticated operations. At the same time, fluctuations in bond yields will also affect the performance of major asset classes.

Investors need to proactively reduce their exposure to interest rate risk and focus on short-duration bonds. Duration is a core indicator for measuring the sensitivity of bond prices to interest rate changes; the longer the duration, the higher the risk. Against the backdrop of controversies surrounding central bank independence and rising risks associated with fiscal dominance, long-duration bonds will bear the most direct negative impact.

Shifting to shorter-duration instruments can effectively mitigate the risk of valuation declines caused by rising interest rates, while also improving the efficiency of capital inflows.

At the same time, a steep yield curve will also affect long-term assets such as gold and technology stocks, and the recent correction is partly due to the influence of Walsh's appointment.

In summary, the Federal Reserve under Warsh's leadership is pushing for a comprehensive restructuring of its monetary policy framework, and the bond market will face multiple changes, including uncertainty about the interest rate path, increased volatility, and rising term premiums.

Investors should base their portfolios on a short-duration, defensive, and well-structured approach, seizing structural opportunities in the market while controlling risk.

(Daily chart of the yield on 30-year US Treasury bonds, source: EasyTrade)

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.