One chart: Baltic Dry Index falls, with all ship types experiencing declines.

2026-05-20 22:53:45

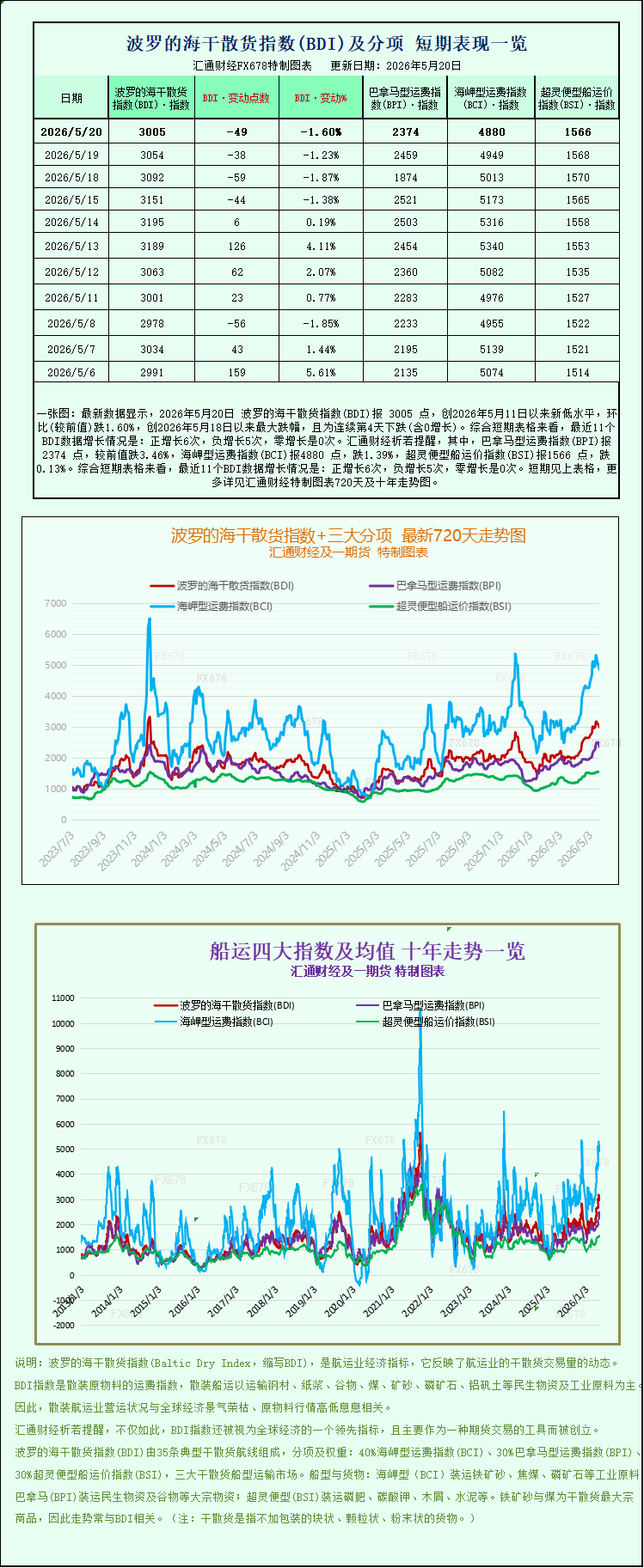

Latest data shows that on May 20, 2026, the Baltic Dry Index (BDI) stood at 3005 points, a new low since May 11, 2026, down 1.60% month-on-month, the largest drop since May 18, 2026, and marking the fourth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 6 positive increases, 5 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2374 points, down 3.46% from the previous value; the Capesize Freight Index (BCI) was 4880 points, down 1.39%; and the Supramax Freight Index (BSI) was 1566 points, down 0.13%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), which tracks global dry bulk shipping freight rates, saw a significant drop on Wednesday. This marks another downward adjustment in the index's recent fluctuating trend, affecting all major vessel types and reflecting the overall weakness in the global dry bulk shipping market. As a core indicator of the international dry bulk shipping market's health, changes in the Baltic Dry Index directly reflect the balance between global demand and supply for commodities such as iron ore, coal, and grains. Its across-the-board decline has drawn widespread attention to the future direction of the shipping market.

The Baltic Dry Index, which tracks freight rates for the three core shipping categories—Capesize, Panamax, and Supramax—fell under pressure, falling 49 points, or 1.6%, to close at 3005. While this drop wasn't the largest single-day decline recently, combined with the slight fluctuations of the previous two days, it indicates a continuous downward trend, breaking the upward trend that had persisted since mid-May and highlighting the current weakness in demand in the dry bulk market. Industry analysts point out that this comprehensive decline is closely related to multiple factors, including a slowdown in global commodity purchasing and relatively ample shipping capacity, making a significant market rebound unlikely in the short term.

Specifically, the performance of Capesize vessels, the "mainstay" of the dry bulk shipping market, was a key factor dragging down the overall index. The Capesize index fell 69 points, or 1.4%, to close at 4880 points, continuing its downward trend in recent days. Capesize bulk carriers are among the world's largest dry bulk carriers, primarily responsible for transoceanic transport of bulk industrial raw materials such as iron ore and coal. Their freight rates are highly correlated with the global steel and energy markets. Specifically, Capesize bulk carriers with a carrying capacity of 150,000 tons saw their average daily revenue decrease by $625, ultimately falling to $40,760. Although still relatively high, the continuous decline in revenue over several days reflects a weakening of demand for their services.

It is worth noting that the iron ore market, which is closely related to the demand for Capesize vessels, saw a slight fluctuation on the day. On Wednesday, Dalian iron ore futures prices gradually rebounded from their morning decline, successfully ending a six-day losing streak and providing slight support to the sluggish dry bulk market. Market analysis suggests that this rebound in iron ore futures prices was mainly driven by news of the resumption of production at four domestic blast furnaces. The market generally expects China's pig iron production to increase accordingly, thereby boosting iron ore procurement demand and indirectly benefiting the demand for Capesize vessels. However, this has not yet reversed the downward trend in freight rates in the short term. According to data from Lange Research, as of May 20, the average daily pig iron output of 201 production enterprises nationwide had increased compared to the previous week, further confirming market expectations of increased pig iron production.

Besides Capesize vessels, Panamax vessels also faced significant downward pressure on freight rates. The Panamax index fell sharply by 85 points, a drop of 3.5%, closing at 2374 points, becoming the vessel type index with the largest decline that day, significantly exceeding the overall index and the Capesize index. Panamax vessels are mainly used to transport 60,000 to 70,000 tons of bulk commodities such as coal and grain. Their transportation demand is closely related to global food trade and energy supply. This sharp decline may be related to the slowdown in global grain exports and a short-term drop in demand for coal transportation. Correspondingly, the average daily revenue of Panamax vessels also declined, falling by $764 to $21,367, marking a relatively high level of single-day revenue decline in recent times.

In the small vessel sector, the Supramax index, while not experiencing a significant drop, was not immune, falling slightly by 2 points, a mere 0.1%, to close at 1566 points, making it the vessel type index with the smallest decline that day. Supramax vessels, due to their flexibility, primarily undertake short-haul, small-volume dry bulk cargo transportation tasks and are relatively less affected by fluctuations in the global commodity market, hence the relatively mild decline. Nevertheless, its decline indicates that the current weakness in the dry bulk shipping market has permeated all vessel types, with no clear safe haven. Previous data showed that secondhand trading prices for Supramax bulk carriers surged in early 2026, but recently, with declining freight rates, market activity has also decreased.

Industry insiders say the recent across-the-board decline in the Baltic Dry Index (BDI) directly reflects adjustments in the global dry bulk market's supply and demand. Currently, the global economic recovery is slowing, and the purchasing demand from major commodity-importing countries has failed to materialize. Meanwhile, relatively ample shipping capacity, coupled with a seasonal decline in demand on some routes, has led to the simultaneous drop in freight rates across all vessel types. Going forward, key factors to watch include changes in China's pig iron production, the pace of global grain and coal exports, and adjustments in shipping capacity, as these will directly impact the future trend of the BDI.

The Baltic Dry Index (BDI), which tracks global dry bulk shipping freight rates, saw a significant drop on Wednesday. This marks another downward adjustment in the index's recent fluctuating trend, affecting all major vessel types and reflecting the overall weakness in the global dry bulk shipping market. As a core indicator of the international dry bulk shipping market's health, changes in the Baltic Dry Index directly reflect the balance between global demand and supply for commodities such as iron ore, coal, and grains. Its across-the-board decline has drawn widespread attention to the future direction of the shipping market.

The Baltic Dry Index, which tracks freight rates for the three core shipping categories—Capesize, Panamax, and Supramax—fell under pressure, falling 49 points, or 1.6%, to close at 3005. While this drop wasn't the largest single-day decline recently, combined with the slight fluctuations of the previous two days, it indicates a continuous downward trend, breaking the upward trend that had persisted since mid-May and highlighting the current weakness in demand in the dry bulk market. Industry analysts point out that this comprehensive decline is closely related to multiple factors, including a slowdown in global commodity purchasing and relatively ample shipping capacity, making a significant market rebound unlikely in the short term.

Specifically, the performance of Capesize vessels, the "mainstay" of the dry bulk shipping market, was a key factor dragging down the overall index. The Capesize index fell 69 points, or 1.4%, to close at 4880 points, continuing its downward trend in recent days. Capesize bulk carriers are among the world's largest dry bulk carriers, primarily responsible for transoceanic transport of bulk industrial raw materials such as iron ore and coal. Their freight rates are highly correlated with the global steel and energy markets. Specifically, Capesize bulk carriers with a carrying capacity of 150,000 tons saw their average daily revenue decrease by $625, ultimately falling to $40,760. Although still relatively high, the continuous decline in revenue over several days reflects a weakening of demand for their services.

It is worth noting that the iron ore market, which is closely related to the demand for Capesize vessels, saw a slight fluctuation on the day. On Wednesday, Dalian iron ore futures prices gradually rebounded from their morning decline, successfully ending a six-day losing streak and providing slight support to the sluggish dry bulk market. Market analysis suggests that this rebound in iron ore futures prices was mainly driven by news of the resumption of production at four domestic blast furnaces. The market generally expects China's pig iron production to increase accordingly, thereby boosting iron ore procurement demand and indirectly benefiting the demand for Capesize vessels. However, this has not yet reversed the downward trend in freight rates in the short term. According to data from Lange Research, as of May 20, the average daily pig iron output of 201 production enterprises nationwide had increased compared to the previous week, further confirming market expectations of increased pig iron production.

Besides Capesize vessels, Panamax vessels also faced significant downward pressure on freight rates. The Panamax index fell sharply by 85 points, a drop of 3.5%, closing at 2374 points, becoming the vessel type index with the largest decline that day, significantly exceeding the overall index and the Capesize index. Panamax vessels are mainly used to transport 60,000 to 70,000 tons of bulk commodities such as coal and grain. Their transportation demand is closely related to global food trade and energy supply. This sharp decline may be related to the slowdown in global grain exports and a short-term drop in demand for coal transportation. Correspondingly, the average daily revenue of Panamax vessels also declined, falling by $764 to $21,367, marking a relatively high level of single-day revenue decline in recent times.

In the small vessel sector, the Supramax index, while not experiencing a significant drop, was not immune, falling slightly by 2 points, a mere 0.1%, to close at 1566 points, making it the vessel type index with the smallest decline that day. Supramax vessels, due to their flexibility, primarily undertake short-haul, small-volume dry bulk cargo transportation tasks and are relatively less affected by fluctuations in the global commodity market, hence the relatively mild decline. Nevertheless, its decline indicates that the current weakness in the dry bulk shipping market has permeated all vessel types, with no clear safe haven. Previous data showed that secondhand trading prices for Supramax bulk carriers surged in early 2026, but recently, with declining freight rates, market activity has also decreased.

Industry insiders say the recent across-the-board decline in the Baltic Dry Index (BDI) directly reflects adjustments in the global dry bulk market's supply and demand. Currently, the global economic recovery is slowing, and the purchasing demand from major commodity-importing countries has failed to materialize. Meanwhile, relatively ample shipping capacity, coupled with a seasonal decline in demand on some routes, has led to the simultaneous drop in freight rates across all vessel types. Going forward, key factors to watch include changes in China's pig iron production, the pace of global grain and coal exports, and adjustments in shipping capacity, as these will directly impact the future trend of the BDI.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.