Are the hawks about to pop the champagne after the Fed's most divided meeting minutes in 32 years?

2026-05-21 16:02:11

The Federal Reserve released the minutes of the FOMC's April policy meeting, which revealed the most serious internal divisions within the Fed in decades.

This also sends a clear signal to the market: inflation concerns have taken over, and policymakers are quietly paving the way for a potential interest rate hike.

This closing meeting, chaired by outgoing Chairman Jerome Powell, not only exposed the fierce power struggle between hawks and doves within the Federal Reserve, but also foreshadowed that incoming Chairman Kevin Warsh would take over a decision-making team with an increasingly hawkish stance.

Since last month, the ongoing geopolitical conflict in Iran has become a key variable driving up inflation, with international oil prices surging by more than 50% against this backdrop, and causing price pressures to spread beyond the energy sector.

This trend has alerted more and more Federal Reserve officials, who have stated that the central bank needs to prepare policy groundwork in advance so that it can start raising interest rates at any time if inflation remains high.

At the April 28-29 meeting, the vast majority of FOMC policymakers reached a consensus: if inflation data remains above the established 2% target for an extended period, moderate monetary tightening measures will be necessary.

Therefore, most participating officials explicitly advocated that the statements in the post-meeting statement that implied a possible future interest rate cut should be deleted, and the tendency toward loose monetary policy should be completely abandoned.

The minutes clearly show the division between the two major camps within the Federal Reserve: one is the ever-growing hawkish camp, which is extremely wary of the upside risks to inflation fueled by the conflict in Iran and firmly opposes any discussion of interest rate cuts;

On the other hand, the doves, whose influence is waning, still adhere to a loose monetary policy and advocate for lowering borrowing costs.

This disagreement was directly reflected in the voting results—the Federal Open Market Committee ultimately maintained the short-term interest rate range of 3.50% to 3.75% by a majority vote, but four officials cast dissenting votes, the highest number since 1992.

Dissenting opinions were polarized: Stephen Milan, Trump's nominee for Federal Reserve Governor (who is about to step down to make room for Warsh), voted against the rate cut again, while three other officials strongly opposed the statement that left open the possibility of a rate cut.

The rise of hawkish forces is primarily driven by the comprehensive escalation of inflationary pressures.

Latest data shows that the US inflation rate rose to a two-year high of 3.3% in March. The IMF and the OECD have raised their full-year inflation forecasts to 3.2% and 4.2% respectively, far exceeding the Federal Reserve's 2% target.

More alarmingly, inflationary pressures have spread from the energy sector to multiple industries such as food and transportation. Nitrogen fertilizer prices have risen by 30% since the outbreak of the war, and the pressure of rising truck transportation costs has been passed on to food companies.

At the same time, the strong resilience of the US job market provided support for hawks: the unemployment rate remained stable, and the 115,000 new non-farm jobs added in April far exceeded expectations, marking two consecutive months of strong performance, proving that the economy does not need to be propped up by interest rate cuts.

Newly appointed Chairman Walsh, who will chair the first interest rate meeting on June 16-17, is facing a complex policy dilemma.

Despite his previous statements supporting interest rate cuts, and despite Trump's (Wash's nominee) strong calls for significant rate cuts, the meeting minutes indicate that there is significant resistance to implementing easing policies. Combined with Trump's recent remarks, this suggests that Trump has lowered his expectations for interest rate cuts.

The market generally expects that Warsh's first meeting after taking office will keep interest rates unchanged, with no possibility of a rate cut.

Looking ahead, the Federal Reserve's policy path will be highly dependent on inflation data and geopolitical developments.

Morgan Stanley warns that U.S. inflation may peak in May or June due to the conflict with Iran, tariff adjustments, and the lagged effects of housing inflation, with little chance of a significant decline in the short term.

Against this backdrop, the Federal Reserve's policy will continue to lean hawkish, and maintaining stable interest rates at the June meeting remains the most likely outcome. The option of raising interest rates has shifted from "potential" to a "ready-to-go" backup tool.

If subsequent inflation data continues to rise beyond expectations, the possibility of the Federal Reserve starting a rate hike cycle in the second half of the year cannot be ruled out.

Conversely, if geopolitical conflicts ease, leading to a decline in energy prices, and inflation shows clear signs of cooling, the policy may maintain a neutral stance, but interest rate cuts will remain a long way off.

For the market, the Fed's "hawkish bias" has become the core pricing logic. In the future, we need to pay close attention to marginal changes in inflation data and geopolitical situation, as well as Warsh's final policy direction after taking office.

As mentioned in yesterday's article, Trump softened his stance and left interest rate decisions to Warsh and the Federal Reserve, but Treasury yields did not continue to rise. In the end, Treasury yields did indeed experience a sharp decline after the negative news was fully priced in.

Although the current US employment data is not bad and inflation continues to rise, raising interest rates seems like an easy answer. However, looking back at these data, inflation is mainly constrained by oil prices. WTI crude oil futures show that oil prices are still in a backwadation structure, which means that oil prices will decline over time. Powell has also said before that war-induced inflation is a one-off event.

However, the increase in low-end employment and the decrease in high-end employment, along with the continued large-scale layoffs in technology companies, does not mean that there are no problems in the labor market.

Therefore, although the probability of an interest rate hike by the end of 2027 is over 50%, interest rate futures can change significantly as things progress. For example, if the US-Iran relations ease, the expectation of an interest rate hike may disappear instantly. So, although the possibility of an interest rate cut has been ruled out, it has not yet reached the point where an interest rate hike is necessary.

(CME interest rate futures, source: CME Futures Exchange)

Interest rate futures indicate that, as of September, there is a 70% probability that the Federal Reserve will keep the federal funds rate unchanged after two FOMC meetings.

This also sends a clear signal to the market: inflation concerns have taken over, and policymakers are quietly paving the way for a potential interest rate hike.

This closing meeting, chaired by outgoing Chairman Jerome Powell, not only exposed the fierce power struggle between hawks and doves within the Federal Reserve, but also foreshadowed that incoming Chairman Kevin Warsh would take over a decision-making team with an increasingly hawkish stance.

Geopolitical conflicts are driving up inflation, and a consensus on austerity is gradually forming.

Since last month, the ongoing geopolitical conflict in Iran has become a key variable driving up inflation, with international oil prices surging by more than 50% against this backdrop, and causing price pressures to spread beyond the energy sector.

This trend has alerted more and more Federal Reserve officials, who have stated that the central bank needs to prepare policy groundwork in advance so that it can start raising interest rates at any time if inflation remains high.

At the April 28-29 meeting, the vast majority of FOMC policymakers reached a consensus: if inflation data remains above the established 2% target for an extended period, moderate monetary tightening measures will be necessary.

Therefore, most participating officials explicitly advocated that the statements in the post-meeting statement that implied a possible future interest rate cut should be deleted, and the tendency toward loose monetary policy should be completely abandoned.

The divide between hawks and doves intensifies, with dissent votes reaching a 32-year high.

The minutes clearly show the division between the two major camps within the Federal Reserve: one is the ever-growing hawkish camp, which is extremely wary of the upside risks to inflation fueled by the conflict in Iran and firmly opposes any discussion of interest rate cuts;

On the other hand, the doves, whose influence is waning, still adhere to a loose monetary policy and advocate for lowering borrowing costs.

This disagreement was directly reflected in the voting results—the Federal Open Market Committee ultimately maintained the short-term interest rate range of 3.50% to 3.75% by a majority vote, but four officials cast dissenting votes, the highest number since 1992.

Dissenting opinions were polarized: Stephen Milan, Trump's nominee for Federal Reserve Governor (who is about to step down to make room for Warsh), voted against the rate cut again, while three other officials strongly opposed the statement that left open the possibility of a rate cut.

Broad-based inflation and strong employment provide double support for hawks.

The rise of hawkish forces is primarily driven by the comprehensive escalation of inflationary pressures.

Latest data shows that the US inflation rate rose to a two-year high of 3.3% in March. The IMF and the OECD have raised their full-year inflation forecasts to 3.2% and 4.2% respectively, far exceeding the Federal Reserve's 2% target.

More alarmingly, inflationary pressures have spread from the energy sector to multiple industries such as food and transportation. Nitrogen fertilizer prices have risen by 30% since the outbreak of the war, and the pressure of rising truck transportation costs has been passed on to food companies.

At the same time, the strong resilience of the US job market provided support for hawks: the unemployment rate remained stable, and the 115,000 new non-farm jobs added in April far exceeded expectations, marking two consecutive months of strong performance, proving that the economy does not need to be propped up by interest rate cuts.

Warsh faces policy hurdles upon taking office; rate cut unlikely at first meeting.

Newly appointed Chairman Walsh, who will chair the first interest rate meeting on June 16-17, is facing a complex policy dilemma.

Despite his previous statements supporting interest rate cuts, and despite Trump's (Wash's nominee) strong calls for significant rate cuts, the meeting minutes indicate that there is significant resistance to implementing easing policies. Combined with Trump's recent remarks, this suggests that Trump has lowered his expectations for interest rate cuts.

The market generally expects that Warsh's first meeting after taking office will keep interest rates unchanged, with no possibility of a rate cut.

Institutional View: Hawkish Faction Dominates, Interest Rate Hike a Potential Option

Looking ahead, the Federal Reserve's policy path will be highly dependent on inflation data and geopolitical developments.

Morgan Stanley warns that U.S. inflation may peak in May or June due to the conflict with Iran, tariff adjustments, and the lagged effects of housing inflation, with little chance of a significant decline in the short term.

Against this backdrop, the Federal Reserve's policy will continue to lean hawkish, and maintaining stable interest rates at the June meeting remains the most likely outcome. The option of raising interest rates has shifted from "potential" to a "ready-to-go" backup tool.

If subsequent inflation data continues to rise beyond expectations, the possibility of the Federal Reserve starting a rate hike cycle in the second half of the year cannot be ruled out.

Conversely, if geopolitical conflicts ease, leading to a decline in energy prices, and inflation shows clear signs of cooling, the policy may maintain a neutral stance, but interest rate cuts will remain a long way off.

For the market, the Fed's "hawkish bias" has become the core pricing logic. In the future, we need to pay close attention to marginal changes in inflation data and geopolitical situation, as well as Warsh's final policy direction after taking office.

Viewpoints and Summary:

As mentioned in yesterday's article, Trump softened his stance and left interest rate decisions to Warsh and the Federal Reserve, but Treasury yields did not continue to rise. In the end, Treasury yields did indeed experience a sharp decline after the negative news was fully priced in.

Although the current US employment data is not bad and inflation continues to rise, raising interest rates seems like an easy answer. However, looking back at these data, inflation is mainly constrained by oil prices. WTI crude oil futures show that oil prices are still in a backwadation structure, which means that oil prices will decline over time. Powell has also said before that war-induced inflation is a one-off event.

However, the increase in low-end employment and the decrease in high-end employment, along with the continued large-scale layoffs in technology companies, does not mean that there are no problems in the labor market.

Therefore, although the probability of an interest rate hike by the end of 2027 is over 50%, interest rate futures can change significantly as things progress. For example, if the US-Iran relations ease, the expectation of an interest rate hike may disappear instantly. So, although the possibility of an interest rate cut has been ruled out, it has not yet reached the point where an interest rate hike is necessary.

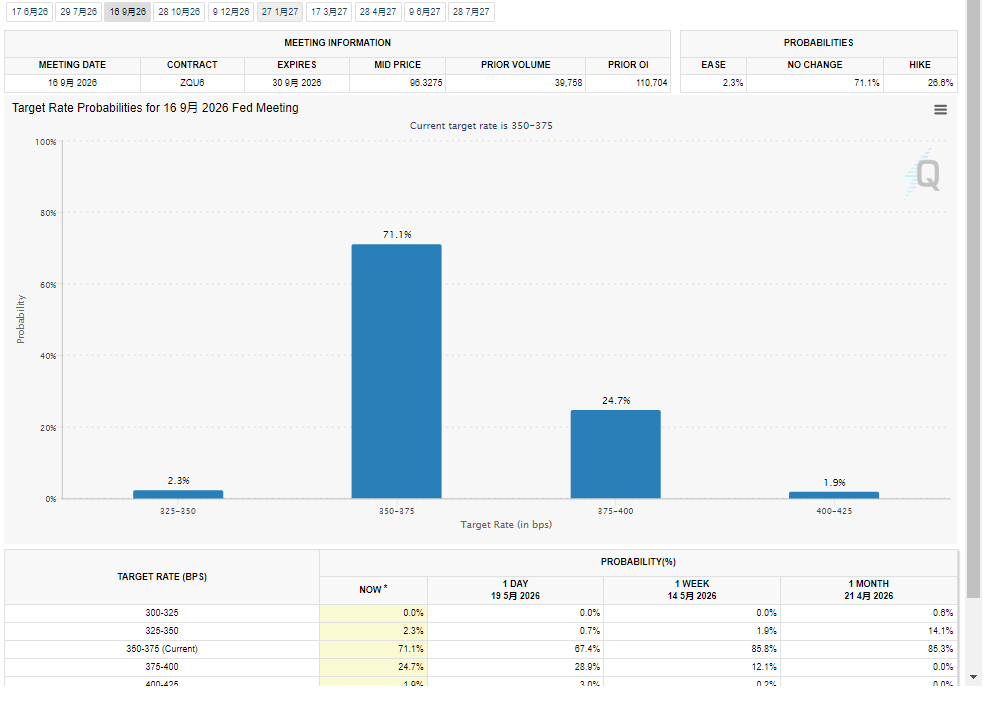

(CME interest rate futures, source: CME Futures Exchange)

Interest rate futures indicate that, as of September, there is a 70% probability that the Federal Reserve will keep the federal funds rate unchanged after two FOMC meetings.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.