A chart shows that the Baltic Dry Index continues to decline, with Capesize and Panamax freight rates dragging down the overall market.

2026-05-21 22:51:11

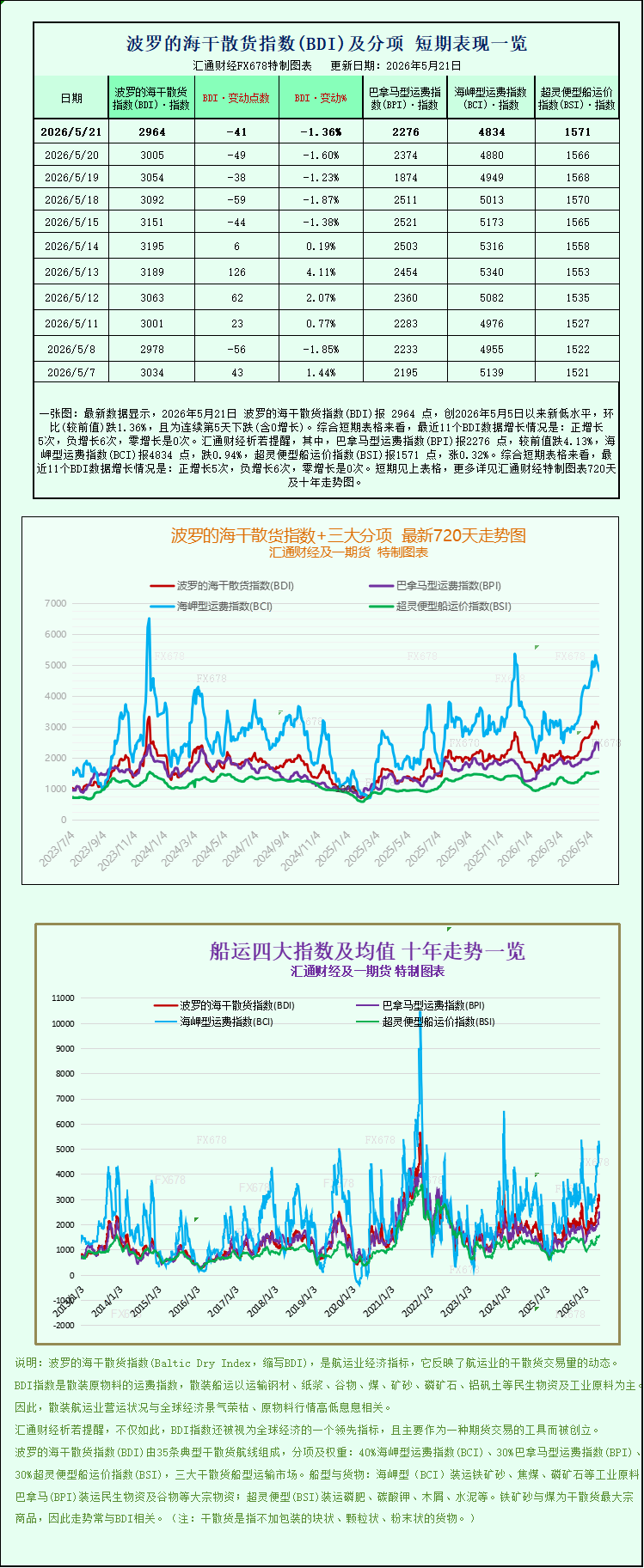

The latest data shows that the Baltic Dry Index (BDI) was 2964 points on May 21, 2026, a new low since May 5, 2026, down 1.36% month-on-month, marking the fifth consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2276 points, down 4.13% from the previous value; the Capesize Freight Index (BCI) was 4834 points, down 0.94%; and the Supramax Freight Index (BSI) was 1571 points, up 0.32%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The international dry bulk shipping market continued to weaken, with the Baltic Dry Index closing down again on Thursday, marking its fifth consecutive day of decline. This round of index decline was mainly dragged down by the simultaneous drop in freight rates for Capesize and Panamax vessels, the main types of vessels. The overall market is showing signs of weak freight demand and a loose supply-demand balance, while small and medium-sized vessels are showing a slight divergence against the trend, exhibiting a structural market.

Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—fell 41 points, or 1.4%, to close at 2,964 points, a more than two-week low and continuing to refresh short-term market lows, reflecting the continued cooling of the overall global dry bulk shipping market.

The market performance of Capesize vessels, the mainstay of large-scale ore and coal transportation, remained sluggish. The Capesize index also declined, falling 46 points, or 0.9%, to close at 4834 points, its lowest level in nearly half a month since May 5th. Corresponding market revenue data showed that the average daily earnings of Capesize vessels mainly transporting 150,000-ton iron ore, thermal coal, and other bulk industrial raw materials on spot routes fell by $425 to $40,335 per day, further narrowing the profit margins of large ocean-going dry bulk carriers.

The core reason for the pressure on Capesize freight rates stems from the weakening of the commodity market. International iron ore futures prices fell sharply on Thursday, hitting a three-week low. Currently, the two major iron ore producing countries, Australia and Brazil, continue to release their exports to China and globally. Coupled with high iron ore inventories at major domestic ports and cautious purchasing demand from downstream steel mills, market activity is insufficient, directly leading to a decrease in ocean-going iron ore shipping orders and a looser matching of ships and cargoes, thus suppressing the continued decline in large Capesize freight rates.

The decline in Panamax vessels, the main medium-sized vessel type, was even more significant, becoming a major drag on the overall market. The Panamax index fell sharply by 98 points, a drop of 4.1%, closing at 2276 points, a decline far exceeding that of other vessel types. The average daily earnings for the main routes of this vessel type decreased by $882, to $20458 per day. It is understood that Panamax vessels mainly carry 60,000 to 70,000 tons of bulk cargo such as thermal coal and grain, and are widely used in regional energy and agricultural product trade. This round of sharp drop in freight rates highlights the phased decline in global seaborne demand for coal and grain, further exacerbating the supply-demand imbalance of too many vessels and too little cargo in the market.

Unlike the general decline in freight rates for medium and large vessels, the market for smaller vessels showed a relatively independent and rebounding trend. The Supramax index rose slightly by 5 points, or 0.3%, to close at 1571 points. The slight recovery in freight rates for smaller vessels mainly benefited from relatively stable demand for short-haul regional bulk cargo transportation, which filled the demand gap in ocean-going bulk cargo transportation, resulting in a market characterized by overall weakness and structural differentiation.

Overall, the current dry bulk shipping market is in an adjustment period characterized by a temporary weakness in demand and relatively ample shipping capacity. Fluctuations in bulk raw material prices and a slowdown in downstream industrial procurement are continuing to impact shipping rates. In the short term, the Baltic Dry Index may continue its weak and volatile pattern. Market trends will still need to be closely monitored in light of the pace of global commodity trade and changes in the supply and demand of major vessel types.

The international dry bulk shipping market continued to weaken, with the Baltic Dry Index closing down again on Thursday, marking its fifth consecutive day of decline. This round of index decline was mainly dragged down by the simultaneous drop in freight rates for Capesize and Panamax vessels, the main types of vessels. The overall market is showing signs of weak freight demand and a loose supply-demand balance, while small and medium-sized vessels are showing a slight divergence against the trend, exhibiting a structural market.

Data shows that the Baltic Dry Index, which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—fell 41 points, or 1.4%, to close at 2,964 points, a more than two-week low and continuing to refresh short-term market lows, reflecting the continued cooling of the overall global dry bulk shipping market.

The market performance of Capesize vessels, the mainstay of large-scale ore and coal transportation, remained sluggish. The Capesize index also declined, falling 46 points, or 0.9%, to close at 4834 points, its lowest level in nearly half a month since May 5th. Corresponding market revenue data showed that the average daily earnings of Capesize vessels mainly transporting 150,000-ton iron ore, thermal coal, and other bulk industrial raw materials on spot routes fell by $425 to $40,335 per day, further narrowing the profit margins of large ocean-going dry bulk carriers.

The core reason for the pressure on Capesize freight rates stems from the weakening of the commodity market. International iron ore futures prices fell sharply on Thursday, hitting a three-week low. Currently, the two major iron ore producing countries, Australia and Brazil, continue to release their exports to China and globally. Coupled with high iron ore inventories at major domestic ports and cautious purchasing demand from downstream steel mills, market activity is insufficient, directly leading to a decrease in ocean-going iron ore shipping orders and a looser matching of ships and cargoes, thus suppressing the continued decline in large Capesize freight rates.

The decline in Panamax vessels, the main medium-sized vessel type, was even more significant, becoming a major drag on the overall market. The Panamax index fell sharply by 98 points, a drop of 4.1%, closing at 2276 points, a decline far exceeding that of other vessel types. The average daily earnings for the main routes of this vessel type decreased by $882, to $20458 per day. It is understood that Panamax vessels mainly carry 60,000 to 70,000 tons of bulk cargo such as thermal coal and grain, and are widely used in regional energy and agricultural product trade. This round of sharp drop in freight rates highlights the phased decline in global seaborne demand for coal and grain, further exacerbating the supply-demand imbalance of too many vessels and too little cargo in the market.

Unlike the general decline in freight rates for medium and large vessels, the market for smaller vessels showed a relatively independent and rebounding trend. The Supramax index rose slightly by 5 points, or 0.3%, to close at 1571 points. The slight recovery in freight rates for smaller vessels mainly benefited from relatively stable demand for short-haul regional bulk cargo transportation, which filled the demand gap in ocean-going bulk cargo transportation, resulting in a market characterized by overall weakness and structural differentiation.

Overall, the current dry bulk shipping market is in an adjustment period characterized by a temporary weakness in demand and relatively ample shipping capacity. Fluctuations in bulk raw material prices and a slowdown in downstream industrial procurement are continuing to impact shipping rates. In the short term, the Baltic Dry Index may continue its weak and volatile pattern. Market trends will still need to be closely monitored in light of the pace of global commodity trade and changes in the supply and demand of major vessel types.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.