A chart shows that the Baltic Dry Index has stopped falling and rebounded slightly, with changes in Capesize vessel capacity driving a rebound in freight rates.

2026-05-23 00:24:32

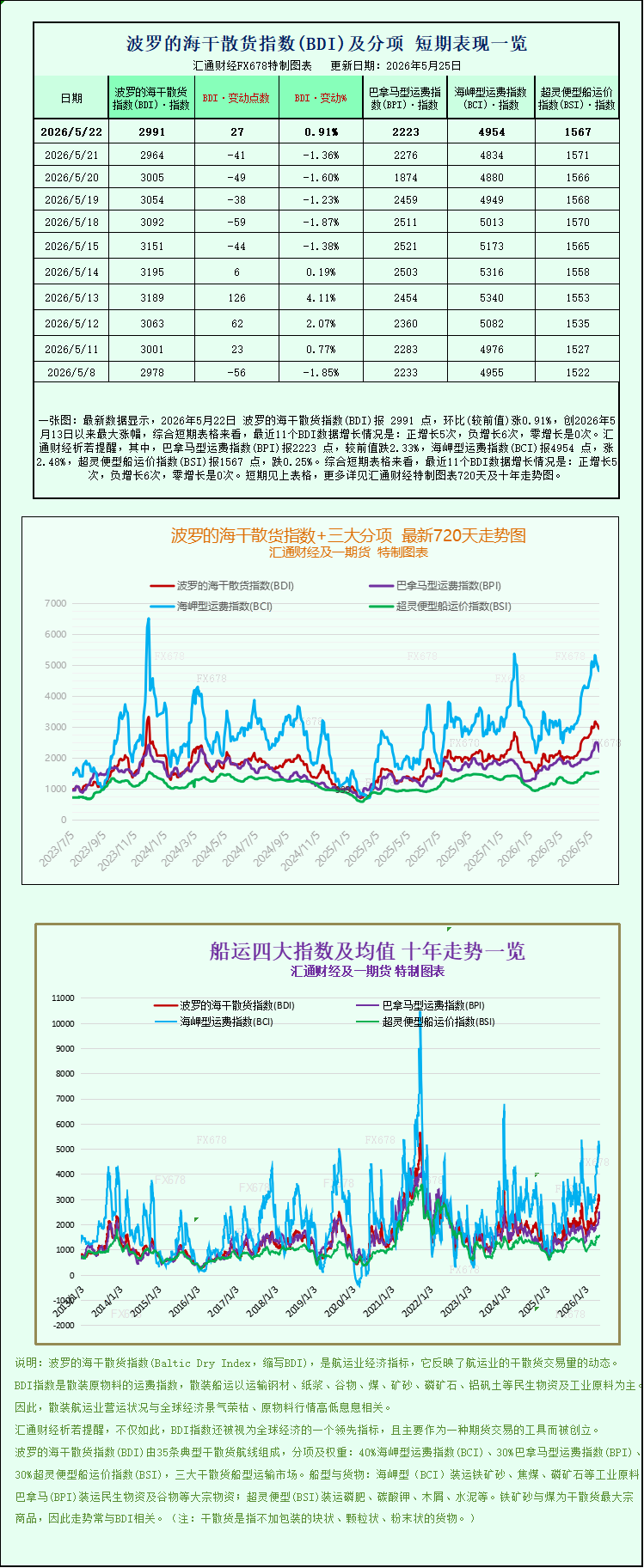

The latest data shows that on May 22, 2026, the Baltic Dry Index (BDI) was 2991 points, up 0.91% from the previous week, marking the largest increase since May 13, 2026. Looking at the short-term charts, the BDI has seen positive growth 5 times, negative growth 6 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 2223 points, down 2.33% from the previous week; the Capesize Freight Index (BCI) was 4954 points, up 2.48%; and the Supramax Freight Index (BSI) was 1567 points, down 0.25%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The international dry bulk shipping market has seen a temporary rebound. The Baltic Dry Index (BDI) reversed its previous downward trend and rose slightly on Friday, ending a five-day losing streak. The main driver of this rebound was the significant increase in Capesize freight rates, which offset the market pressure from the weakening freight rates of smaller vessels, allowing the overall index to stop falling and rise.

According to comprehensive market data, the Baltic Dry Index (BDI), which covers freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 27 points, or 0.9%, to close at 2991 points. However, looking at the overall weekly trend, the shipping market was under significant pressure. The index fell by 5% this week, marking its worst weekly performance since early March, reflecting the recent increased volatility and significant divergence in the dry bulk shipping market.

The Capesize bulk carrier market showed a significant recovery, serving as the core support for this index rebound. The Capesize index, which tracks freight rates for large ocean-going dry bulk carriers, surged 120 points, a 2.5% increase, closing at 4954 points. Despite the substantial single-day rebound, the index still recorded a weekly decline of approximately 4.2% due to the earlier correction during the week. It is understood that this round of Capesize freight rate increases was mainly driven by an increase in the number of available vessels on core global routes, coupled with a temporary release of freight demand on major iron ore shipping routes, leading to a marginal improvement in the supply-demand relationship and directly boosting the operating profits of large bulk carriers.

Specific operational data shows that Capesize vessels, primarily engaged in the transportation of 150,000-ton bulk raw materials and mainly carrying industrial raw materials such as iron ore and coal, have seen a significant increase in their average daily earnings on their benchmark routes. The average daily earnings of Capesize vessels increased by $1,093 on the day, reaching a latest average daily earnings of $41,428. The profitability of large dry bulk carriers has recovered significantly, making it one of the few sectors showing positive growth in the market this week.

The iron ore spot market, linked to ocean freight rates, exhibited a volatile and divergent trend. On May 22nd, iron ore prices fluctuated wildly after opening. Initially, the market was generally concerned that increased global supply, coupled with the arrival of the traditional off-season overseas, would lead to weak seasonal demand and potentially drag down prices. Iron ore prices were under pressure, nearing a second consecutive week of decline. However, thanks to an unexpectedly strong recovery in end-user consumption in China, the world's largest iron ore consumer, and increased activity in domestic steel mills' purchasing activities, the market was effectively supported. This significantly offset the negative pressures of ample supply and weak off-season demand, ultimately limiting the overall decline in iron ore prices and providing fundamental support for Capesize vessel freight demand.

In contrast to the strong rebound of large Capesize vessels, the market for medium and small dry bulk carriers remained weak, with a clear divergence in market performance between vessel types. Panamax freight rates weakened significantly, with the Panamax index falling 53 points, or 2.3%, to close at 2223 points. The weekly decline widened further, accumulating a drop of nearly 12%, becoming the main factor dragging down the overall index performance this week.

Correspondingly, ship operating revenue declined as well. Panamax vessels, which mainly transport coal, grain and other food and energy materials in the 60,000 to 70,000 ton range, saw their average daily revenue decrease by $481 on that day, with the latest average daily revenue dropping to $20,004. The medium-sized bulk carrier shipping market experienced weak demand and continued freight rate declines, indicating a significant lack of market activity.

The market for small dry bulk carriers remained relatively stable, with significantly smaller fluctuations than that of medium and large vessels. The Supramax vessel index fell slightly by 4 points, a mere 0.3%, closing at 1567 points. It showed relatively strong resilience, posting a slight increase for the week, with a weekly gain of approximately 0.1%. Among all vessel types, it performed the most steadily, primarily benefiting from the rigid demand for short-haul regional general cargo transportation, and was relatively less affected by fluctuations in the international bulk commodity market.

Overall, the current dry bulk shipping market is showing a clear structural differentiation pattern. Large mining vessels have rebounded due to marginal improvements in demand, while medium- and short-haul grain and coal vessels continue to weaken due to the drag of off-season demand. The market as a whole has not yet escaped the phase of adjustment.

The international dry bulk shipping market has seen a temporary rebound. The Baltic Dry Index (BDI) reversed its previous downward trend and rose slightly on Friday, ending a five-day losing streak. The main driver of this rebound was the significant increase in Capesize freight rates, which offset the market pressure from the weakening freight rates of smaller vessels, allowing the overall index to stop falling and rise.

According to comprehensive market data, the Baltic Dry Index (BDI), which covers freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—rose 27 points, or 0.9%, to close at 2991 points. However, looking at the overall weekly trend, the shipping market was under significant pressure. The index fell by 5% this week, marking its worst weekly performance since early March, reflecting the recent increased volatility and significant divergence in the dry bulk shipping market.

The Capesize bulk carrier market showed a significant recovery, serving as the core support for this index rebound. The Capesize index, which tracks freight rates for large ocean-going dry bulk carriers, surged 120 points, a 2.5% increase, closing at 4954 points. Despite the substantial single-day rebound, the index still recorded a weekly decline of approximately 4.2% due to the earlier correction during the week. It is understood that this round of Capesize freight rate increases was mainly driven by an increase in the number of available vessels on core global routes, coupled with a temporary release of freight demand on major iron ore shipping routes, leading to a marginal improvement in the supply-demand relationship and directly boosting the operating profits of large bulk carriers.

Specific operational data shows that Capesize vessels, primarily engaged in the transportation of 150,000-ton bulk raw materials and mainly carrying industrial raw materials such as iron ore and coal, have seen a significant increase in their average daily earnings on their benchmark routes. The average daily earnings of Capesize vessels increased by $1,093 on the day, reaching a latest average daily earnings of $41,428. The profitability of large dry bulk carriers has recovered significantly, making it one of the few sectors showing positive growth in the market this week.

The iron ore spot market, linked to ocean freight rates, exhibited a volatile and divergent trend. On May 22nd, iron ore prices fluctuated wildly after opening. Initially, the market was generally concerned that increased global supply, coupled with the arrival of the traditional off-season overseas, would lead to weak seasonal demand and potentially drag down prices. Iron ore prices were under pressure, nearing a second consecutive week of decline. However, thanks to an unexpectedly strong recovery in end-user consumption in China, the world's largest iron ore consumer, and increased activity in domestic steel mills' purchasing activities, the market was effectively supported. This significantly offset the negative pressures of ample supply and weak off-season demand, ultimately limiting the overall decline in iron ore prices and providing fundamental support for Capesize vessel freight demand.

In contrast to the strong rebound of large Capesize vessels, the market for medium and small dry bulk carriers remained weak, with a clear divergence in market performance between vessel types. Panamax freight rates weakened significantly, with the Panamax index falling 53 points, or 2.3%, to close at 2223 points. The weekly decline widened further, accumulating a drop of nearly 12%, becoming the main factor dragging down the overall index performance this week.

Correspondingly, ship operating revenue declined as well. Panamax vessels, which mainly transport coal, grain and other food and energy materials in the 60,000 to 70,000 ton range, saw their average daily revenue decrease by $481 on that day, with the latest average daily revenue dropping to $20,004. The medium-sized bulk carrier shipping market experienced weak demand and continued freight rate declines, indicating a significant lack of market activity.

The market for small dry bulk carriers remained relatively stable, with significantly smaller fluctuations than that of medium and large vessels. The Supramax vessel index fell slightly by 4 points, a mere 0.3%, closing at 1567 points. It showed relatively strong resilience, posting a slight increase for the week, with a weekly gain of approximately 0.1%. Among all vessel types, it performed the most steadily, primarily benefiting from the rigid demand for short-haul regional general cargo transportation, and was relatively less affected by fluctuations in the international bulk commodity market.

Overall, the current dry bulk shipping market is showing a clear structural differentiation pattern. Large mining vessels have rebounded due to marginal improvements in demand, while medium- and short-haul grain and coal vessels continue to weaken due to the drag of off-season demand. The market as a whole has not yet escaped the phase of adjustment.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.