Is being number one on paper a sweet trap? Gold reserves surpass US Treasury bonds, yet the country is facing a double whammy of interest rates and gold sales.

2026-06-03 16:34:38

On Wednesday (June 3), spot gold continued to weaken under pressure during the Asian and European sessions, with the price hovering around $4,460.

The ongoing geopolitical tensions in the Middle East are the source of factors influencing crude oil prices and inflation expectations, and also a significant factor contributing to the short-term weakness in gold prices.

The 60-day ceasefire agreement between the US and Iran is like a mirage. The US Central Command previously launched a self-defense military strike against Iran's Qeshm Island, and Iran immediately retaliated with missiles and drones against US military bases in Kuwait and Bahrain. Meanwhile, the ground conflict between Israel and Hezbollah in Lebanon escalated simultaneously.

Negotiations between the US and Iran over Iran's uranium enrichment program and the opening of the Strait of Hormuz have reached a deep stalemate. US Secretary of State Marco Rubio has made it clear that the US will not use the full opening of the Strait of Hormuz as a condition for lifting sanctions against Iran, and any sanctions waiver would require Iran to abandon its highly enriched uranium production.

Although the US and Iran are currently in a ceasefire and the US military continues to maintain a naval blockade against Iran, the ceasefire will remain in effect until bilateral negotiations are finalized.

However, affected by the uncertain prospects for cross-strait navigation and repeated skirmishes between the two countries, international crude oil prices rose for the third consecutive trading day, continuing to rebound from the monthly low of last Friday.

Rising oil prices have reignited the risk of global inflation, forcing major central banks around the world to maintain hawkish monetary policies, leading to a consensus in the market that "high interest rates will continue for a long time."

As a zero-interest asset, gold's price is initially pressured downwards due to increased holding costs in a high-interest-rate environment.

The rising pricing of Fed rate hikes and the concentrated reduction of US Treasury holdings by multiple countries have jointly pushed up US Treasury yields, creating a double pressure on gold prices from both the dollar and opportunity cost perspectives.

Cleveland Federal Reserve President Beth Hammark publicly reiterated that the Fed remains committed to its 2% inflation target and will quickly implement tightening measures if inflation falls less than expected.

According to data from the CME Group's FedWatch Tool, although the market believed in a 98% probability of maintaining the current interest rate of 3.5%-3.75% in June, the market bet on a 25 basis point rate hike at the Fed's December meeting exceeded 50%. Coupled with the market's continued rise in bets on another Fed rate hike in 2026, the fundamentals of the US dollar received strong support.

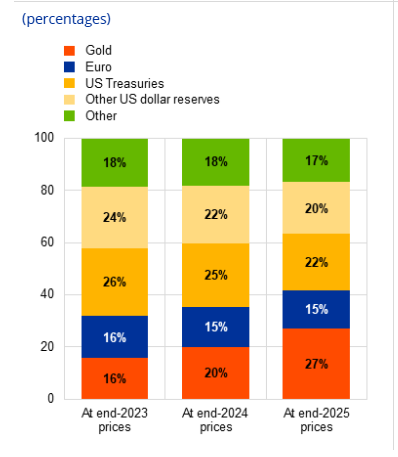

A recent research report from the European Central Bank revealed a significant shift in the structure of global foreign exchange reserves, with gold officially surpassing US Treasury bonds to become the world's largest reserve asset on paper.

By the end of 2025, gold will account for 27% of global official reserves, higher than the 22% allocation to US Treasury bonds and 15% to euro-denominated assets.

However, the increase in this proportion is mostly due to the book changes brought about by the rise in gold price valuation. International gold prices will rise by 30% and 60% in 2024 and 2025, respectively. If we recalculate based on the gold price at the end of 2023 after removing price disturbances, the proportion of gold and euro reserves will both be 16% (the proportion of gold will only increase slightly), while US Treasury bonds will still remain the largest allocation with a 26% allocation.

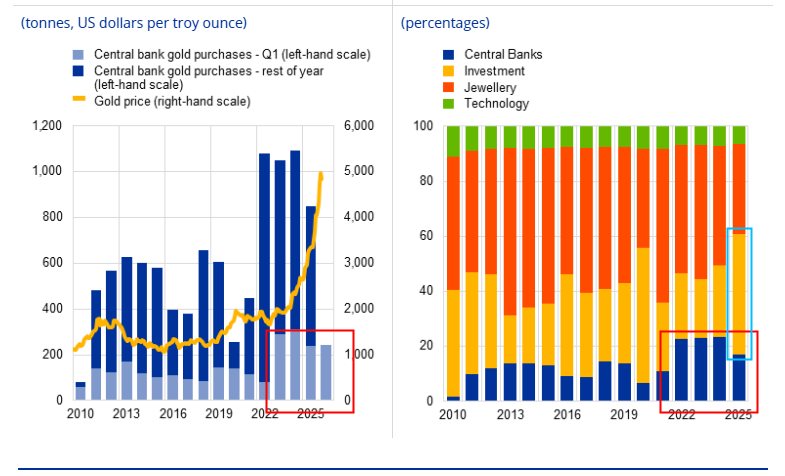

Dragged down by historically high gold prices, global central banks' annual net gold purchases fell to 850 tons in 2025, a significant slowdown compared to the average annual purchases of over 1,000 tons from 2022 to 2024. High gold prices have reduced the willingness of central banks to increase their gold purchases, but the total amount of gold purchased throughout the year still far exceeded the historical average before the outbreak of the Russia-Ukraine conflict.

(Gold market capitalization as a percentage of global official reserves, Source: European Central Bank)

While the central bank slowed its gold purchases, private gold investment demand experienced explosive growth, impacting gold prices from the demand side.

Global private physical gold demand is expected to climb to nearly 2,200 tons in 2025, almost doubling year-on-year, accounting for nearly half of the total global physical gold demand; gold ETFs saw a net inflow of US$89 billion throughout the year, with physical purchases of about 800 tons, which is the core driving force for private gold purchases.

However, these funds tend to be less disciplined and often chase rising prices and sell falling ones, leading to significant fluctuations in gold prices. At the same time, due to rising gold prices, sales of gold jewelry have dropped sharply, and central banks have clearly begun to slow down their gold purchases during the surge in gold prices, which is consistent with the analysis in the previous paragraph. Fortunately, demand from the technology sector remains stable, and there is an expectation of high growth in gold usage for technology in the future.

(A chart showing changes in central bank gold purchases and key players in gold demand; source: European Central Bank)

In an environment of normalized geopolitical conflicts, global central bank gold operations have shown a clear polarization, with some countries hoarding gold and some energy exporting countries passively selling gold, directly exacerbating short-term gold price volatility.

Since the outbreak of the Russia-Ukraine conflict in 2022, China has accumulated more than 350 tons of gold, followed by Poland, Turkey and India with 320 tons, 220 tons and 130 tons respectively. In 2025, Poland will become the world's number one official gold buyer with a purchase volume of 100 tons, followed by Kazakhstan, Brazil, China and Turkey.

Economies with high geopolitical risks continue to hoard gold, primarily to hedge against geopolitical black swan risks and optimize their balance sheets' resilience.

Conversely, some energy-exporting countries have experienced disruptions to energy trade and a sharp decline in dollar revenue due to the war. In order to support their economies and stabilize their currencies, they have chosen to liquidate their gold reserves, which has become a significant negative factor for gold prices in the short term.

Turkey has sold or lent out approximately 130 tons of gold in the past two years to hedge against high energy import costs and stabilize the lira's exchange rate. Market news in 2026 indicated that Russia also began monetizing its gold reserves to supplement frontline war expenses.

At the same time, central banks around the world continued to reduce their holdings of U.S. Treasury assets held in custody accounts at the Federal Reserve Bank of New York. In March 2026, overseas official holdings of U.S. Treasury bonds shrank by $82 billion in a single month, bringing the total to $2.7 trillion, the lowest level since 2012.

A widespread sell-off of US Treasuries pushed down bond prices and helped US Treasury yields rise steadily. The US dollar held onto its weekly gains, supported by high yields and expectations of interest rate hikes. The strengthening dollar, coupled with rising US Treasury yields, continued to suppress the price of gold, which is denominated in US dollars.

Central bank gold purchases are the main reason supporting gold prices, but excessively high gold prices can also curb central bank gold purchases. Although the total market value of gold held by all countries exceeds that of US Treasury bonds, making it the world's largest reserve asset, this result is jointly determined by gold purchases and gold prices. This means that rising gold prices have to some extent fulfilled the central bank's goal of accumulating gold reserves, which is actually not conducive to central banks continuing to increase their gold holdings. Furthermore, due to declining energy revenues, some countries have had to sell gold. At the same time, to meet the demand for US dollars from various countries, US Treasury bonds have been sold off, which has suppressed real interest rates and is not conducive to a rebound in gold prices.

Rising real interest rates will lead to a rapid depreciation of many assets. When stock prices fall in Middle Eastern countries, people tend to sell gold, which has fallen less or has unrealized gains, first.

On the surface, the US and Iran claim they are close to reaching an agreement, but in reality, there is no sign of compromise on core issues such as passage through the Taiwan Strait and enriched uranium. The US is facing the midterm elections and is unable to afford an agreement that is unfavorable to it, while Iran seems to be able to afford the delays, even though its oil production cuts have led to insufficient storage space.

In conclusion, considering the downward trend in gold prices, any significant rebound in gold prices may present an opportunity to reduce positions or short sell. Conversely, a sharp decline could lead to a mean-reversion rebound.

(Spot gold daily chart, source: EasyForex subsidiary)

At 16:27 Beijing time, spot gold was trading at $4454.50 per ounce.

The ongoing geopolitical tensions in the Middle East are the source of factors influencing crude oil prices and inflation expectations, and also a significant factor contributing to the short-term weakness in gold prices.

The 60-day ceasefire agreement between the US and Iran is like a mirage. The US Central Command previously launched a self-defense military strike against Iran's Qeshm Island, and Iran immediately retaliated with missiles and drones against US military bases in Kuwait and Bahrain. Meanwhile, the ground conflict between Israel and Hezbollah in Lebanon escalated simultaneously.

Negotiations between the US and Iran over Iran's uranium enrichment program and the opening of the Strait of Hormuz have reached a deep stalemate. US Secretary of State Marco Rubio has made it clear that the US will not use the full opening of the Strait of Hormuz as a condition for lifting sanctions against Iran, and any sanctions waiver would require Iran to abandon its highly enriched uranium production.

Although the US and Iran are currently in a ceasefire and the US military continues to maintain a naval blockade against Iran, the ceasefire will remain in effect until bilateral negotiations are finalized.

However, affected by the uncertain prospects for cross-strait navigation and repeated skirmishes between the two countries, international crude oil prices rose for the third consecutive trading day, continuing to rebound from the monthly low of last Friday.

Rising oil prices have reignited the risk of global inflation, forcing major central banks around the world to maintain hawkish monetary policies, leading to a consensus in the market that "high interest rates will continue for a long time."

As a zero-interest asset, gold's price is initially pressured downwards due to increased holding costs in a high-interest-rate environment.

As expectations of a Federal Reserve rate hike intensify, a global sell-off of US Treasury bonds has pushed up yields and put downward pressure on gold prices.

The rising pricing of Fed rate hikes and the concentrated reduction of US Treasury holdings by multiple countries have jointly pushed up US Treasury yields, creating a double pressure on gold prices from both the dollar and opportunity cost perspectives.

Cleveland Federal Reserve President Beth Hammark publicly reiterated that the Fed remains committed to its 2% inflation target and will quickly implement tightening measures if inflation falls less than expected.

According to data from the CME Group's FedWatch Tool, although the market believed in a 98% probability of maintaining the current interest rate of 3.5%-3.75% in June, the market bet on a 25 basis point rate hike at the Fed's December meeting exceeded 50%. Coupled with the market's continued rise in bets on another Fed rate hike in 2026, the fundamentals of the US dollar received strong support.

ECB research reveals a major shift in reserve dynamics, with gold's share of total assets surpassing that of US Treasury bonds for the first time.

A recent research report from the European Central Bank revealed a significant shift in the structure of global foreign exchange reserves, with gold officially surpassing US Treasury bonds to become the world's largest reserve asset on paper.

By the end of 2025, gold will account for 27% of global official reserves, higher than the 22% allocation to US Treasury bonds and 15% to euro-denominated assets.

However, the increase in this proportion is mostly due to the book changes brought about by the rise in gold price valuation. International gold prices will rise by 30% and 60% in 2024 and 2025, respectively. If we recalculate based on the gold price at the end of 2023 after removing price disturbances, the proportion of gold and euro reserves will both be 16% (the proportion of gold will only increase slightly), while US Treasury bonds will still remain the largest allocation with a 26% allocation.

Dragged down by historically high gold prices, global central banks' annual net gold purchases fell to 850 tons in 2025, a significant slowdown compared to the average annual purchases of over 1,000 tons from 2022 to 2024. High gold prices have reduced the willingness of central banks to increase their gold purchases, but the total amount of gold purchased throughout the year still far exceeded the historical average before the outbreak of the Russia-Ukraine conflict.

(Gold market capitalization as a percentage of global official reserves, Source: European Central Bank)

The surge in private investment demand has become a significant factor influencing marginal changes in gold prices.

While the central bank slowed its gold purchases, private gold investment demand experienced explosive growth, impacting gold prices from the demand side.

Global private physical gold demand is expected to climb to nearly 2,200 tons in 2025, almost doubling year-on-year, accounting for nearly half of the total global physical gold demand; gold ETFs saw a net inflow of US$89 billion throughout the year, with physical purchases of about 800 tons, which is the core driving force for private gold purchases.

However, these funds tend to be less disciplined and often chase rising prices and sell falling ones, leading to significant fluctuations in gold prices. At the same time, due to rising gold prices, sales of gold jewelry have dropped sharply, and central banks have clearly begun to slow down their gold purchases during the surge in gold prices, which is consistent with the analysis in the previous paragraph. Fortunately, demand from the technology sector remains stable, and there is an expectation of high growth in gold usage for technology in the future.

(A chart showing changes in central bank gold purchases and key players in gold demand; source: European Central Bank)

Central bank gold purchases and sales diverged, with some energy-producing countries selling off their gold reserves, creating short-term selling pressure.

In an environment of normalized geopolitical conflicts, global central bank gold operations have shown a clear polarization, with some countries hoarding gold and some energy exporting countries passively selling gold, directly exacerbating short-term gold price volatility.

Since the outbreak of the Russia-Ukraine conflict in 2022, China has accumulated more than 350 tons of gold, followed by Poland, Turkey and India with 320 tons, 220 tons and 130 tons respectively. In 2025, Poland will become the world's number one official gold buyer with a purchase volume of 100 tons, followed by Kazakhstan, Brazil, China and Turkey.

Economies with high geopolitical risks continue to hoard gold, primarily to hedge against geopolitical black swan risks and optimize their balance sheets' resilience.

Conversely, some energy-exporting countries have experienced disruptions to energy trade and a sharp decline in dollar revenue due to the war. In order to support their economies and stabilize their currencies, they have chosen to liquidate their gold reserves, which has become a significant negative factor for gold prices in the short term.

Turkey has sold or lent out approximately 130 tons of gold in the past two years to hedge against high energy import costs and stabilize the lira's exchange rate. Market news in 2026 indicated that Russia also began monetizing its gold reserves to supplement frontline war expenses.

The combined effect of energy-related countries' centralized gold sales and global sell-offs of US Treasury bonds, which raised yields, created a double negative factor, putting downward pressure on gold prices.

At the same time, central banks around the world continued to reduce their holdings of U.S. Treasury assets held in custody accounts at the Federal Reserve Bank of New York. In March 2026, overseas official holdings of U.S. Treasury bonds shrank by $82 billion in a single month, bringing the total to $2.7 trillion, the lowest level since 2012.

A widespread sell-off of US Treasuries pushed down bond prices and helped US Treasury yields rise steadily. The US dollar held onto its weekly gains, supported by high yields and expectations of interest rate hikes. The strengthening dollar, coupled with rising US Treasury yields, continued to suppress the price of gold, which is denominated in US dollars.

Summary and Technical Analysis:

Central bank gold purchases are the main reason supporting gold prices, but excessively high gold prices can also curb central bank gold purchases. Although the total market value of gold held by all countries exceeds that of US Treasury bonds, making it the world's largest reserve asset, this result is jointly determined by gold purchases and gold prices. This means that rising gold prices have to some extent fulfilled the central bank's goal of accumulating gold reserves, which is actually not conducive to central banks continuing to increase their gold holdings. Furthermore, due to declining energy revenues, some countries have had to sell gold. At the same time, to meet the demand for US dollars from various countries, US Treasury bonds have been sold off, which has suppressed real interest rates and is not conducive to a rebound in gold prices.

Rising real interest rates will lead to a rapid depreciation of many assets. When stock prices fall in Middle Eastern countries, people tend to sell gold, which has fallen less or has unrealized gains, first.

On the surface, the US and Iran claim they are close to reaching an agreement, but in reality, there is no sign of compromise on core issues such as passage through the Taiwan Strait and enriched uranium. The US is facing the midterm elections and is unable to afford an agreement that is unfavorable to it, while Iran seems to be able to afford the delays, even though its oil production cuts have led to insufficient storage space.

In conclusion, considering the downward trend in gold prices, any significant rebound in gold prices may present an opportunity to reduce positions or short sell. Conversely, a sharp decline could lead to a mean-reversion rebound.

(Spot gold daily chart, source: EasyForex subsidiary)

At 16:27 Beijing time, spot gold was trading at $4454.50 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.