From 155 to 160: The underlying macroeconomic factors behind the USD/JPY correction.

2026-06-04 19:39:26

On Thursday, the USD/JPY pair remained near the psychological level of 160. During the European session, the pair traded around 159.85, experiencing a slight pullback but still remaining at higher levels. In terms of market context, oil price risks, interest rate constraints, expectations of a Bank of Japan rate hike, and technical overbought conditions are all weighing on the same trading chart. In the short term, the USD/JPY pair is no longer simply a carry trade, but rather a concentrated expression of macroeconomic tail risks.

160 is not simply a round number, but rather the overlapping area of a policy-sensitive zone, an option entry zone, and a congested trend trading zone. At its April meeting, the Bank of Japan maintained the interest rate at 0.75% by a 6-3 vote, but three members advocated raising it to 1.0%, citing rising price risks and still relatively loose financial conditions. This means that the current weakness of the yen cannot be simply explained by the Bank of Japan's lack of room for maneuver. The real issue is that the market has already priced in a higher probability of a rate hike; the marginal surprise comes from the wording of the policy decision, the pace of tapering bond purchases, and the tolerance for exchange rate fluctuations.

Kazuo Ueda's recent statements are not primarily about a one-time interest rate hike, but rather the sustainability of inflation. He stated that if core inflation follows the baseline scenario of 2%, the Bank of Japan will continue to raise policy rates and adjust the degree of easing, while still needing to observe the financial markets and price paths. Such statements provide support for the yen, but the strength of this support is diluted by two factors. First, the market has already priced in a June rate hike. Second, if the pace of tapering bond purchases is simultaneously slowed or paused, pressure on the Japanese bond market will ease, but the tightening signal received by the yen will also be diminished. In other words, the more the Bank of Japan emphasizes stabilizing the bond market, the harder it is for the exchange rate to receive unilateral support.

The latest Federal Reserve interest rate table shows that on June 2, the effective federal funds rate was 3.62%, the 10-year US Treasury yield was 4.46%, and the 10-year Japanese government bond yield was approximately 2.67%, resulting in a long-term interest rate spread of about 1.81 percentage points. Although this spread has narrowed compared to previous extreme periods, it is still sufficient to weaken the yen's rebound potential.

Oil prices are another key factor. Brent crude remains around $96 per barrel, a slight decrease from the previous trading day, but still up nearly 48% over the past year. For Japan, which is heavily reliant on energy imports, high oil prices will simultaneously increase import costs, compress real income, and worsen terms of trade. The Bank of Japan's April outlook has raised its CPI forecast for fiscal year 2026, excluding fresh food, to 2.5% to 3.0%, and explicitly highlighted the impact of the Middle East situation on financial and exchange rate markets. Therefore, the more volatile oil prices become, the harder it will be for the yen to reverse its trend with a single interest rate hike.

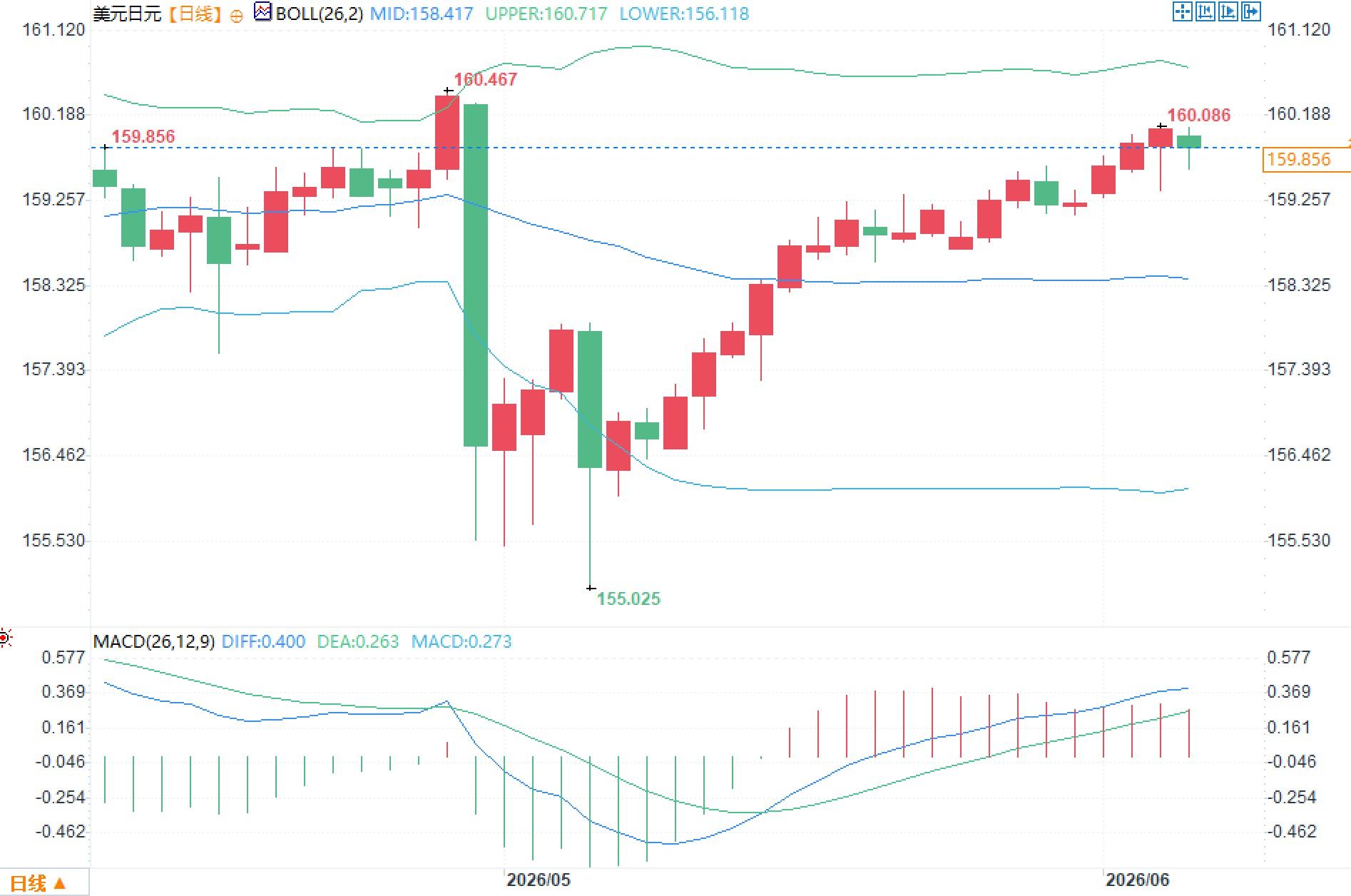

From the daily chart, the exchange rate rebounded quickly after a sharp drop to 155.025 and is currently trading above the Bollinger Middle Band at 158.417, near the Upper Band at 160.717. The MACD indicator shows the DIFF at 0.400 and the DEA at 0.263, with the histogram still positive, indicating that the recovery trend remains intact, but momentum has not expanded significantly.

Traders are truly focused on structural contradictions. If the exchange rate continues to approach 160, policy statements, liquidity, and option positions could amplify intraday volatility. A drop back to around 158.40 would mean the Bollinger Middle Band has once again become a balance line between bulls and bears, at which point the market will reassess whether the Bank of Japan's rate hike has been fully priced in. Currently, it's more like an event-pricing phase within a high-level trading range, rather than a one-way macroeconomic narrative.

Question 1: If the Bank of Japan raises interest rates in June, will the USD/JPY exchange rate necessarily fall?

A: Not necessarily. If interest rate hikes have already been fully priced in, and there are simultaneous signals of a slowdown in bond purchases, the yen may receive limited support. The key lies in whether the subsequent interest rate path becomes clearer.

Question 2: Why is the 160 mark so sensitive?

A: It reflects policy attention, option positions, and the crowding of trend trading. Once the price repeatedly touches the level, volatility is usually amplified, but this does not necessarily mean that a one-sided market trend will occur.

Question 3: Why do oil prices affect the USD/JPY exchange rate?

A: High oil prices will increase Japan's import costs, compress corporate profits and residents' real income, and may also increase global inflation stickiness, prompting the Federal Reserve to remain cautious, ultimately affecting exchange rates through interest rate differentials and risk appetite.

I. Pricing Logic Around the 160 Mark

160 is not simply a round number, but rather the overlapping area of a policy-sensitive zone, an option entry zone, and a congested trend trading zone. At its April meeting, the Bank of Japan maintained the interest rate at 0.75% by a 6-3 vote, but three members advocated raising it to 1.0%, citing rising price risks and still relatively loose financial conditions. This means that the current weakness of the yen cannot be simply explained by the Bank of Japan's lack of room for maneuver. The real issue is that the market has already priced in a higher probability of a rate hike; the marginal surprise comes from the wording of the policy decision, the pace of tapering bond purchases, and the tolerance for exchange rate fluctuations.

II. Why the Bank of Japan's hawkish shift failed to suppress the USD/JPY exchange rate.

Kazuo Ueda's recent statements are not primarily about a one-time interest rate hike, but rather the sustainability of inflation. He stated that if core inflation follows the baseline scenario of 2%, the Bank of Japan will continue to raise policy rates and adjust the degree of easing, while still needing to observe the financial markets and price paths. Such statements provide support for the yen, but the strength of this support is diluted by two factors. First, the market has already priced in a June rate hike. Second, if the pace of tapering bond purchases is simultaneously slowed or paused, pressure on the Japanese bond market will ease, but the tightening signal received by the yen will also be diminished. In other words, the more the Bank of Japan emphasizes stabilizing the bond market, the harder it is for the exchange rate to receive unilateral support.

III. Interest rate spreads and oil prices remain the core constraints.

The latest Federal Reserve interest rate table shows that on June 2, the effective federal funds rate was 3.62%, the 10-year US Treasury yield was 4.46%, and the 10-year Japanese government bond yield was approximately 2.67%, resulting in a long-term interest rate spread of about 1.81 percentage points. Although this spread has narrowed compared to previous extreme periods, it is still sufficient to weaken the yen's rebound potential.

Oil prices are another key factor. Brent crude remains around $96 per barrel, a slight decrease from the previous trading day, but still up nearly 48% over the past year. For Japan, which is heavily reliant on energy imports, high oil prices will simultaneously increase import costs, compress real income, and worsen terms of trade. The Bank of Japan's April outlook has raised its CPI forecast for fiscal year 2026, excluding fresh food, to 2.5% to 3.0%, and explicitly highlighted the impact of the Middle East situation on financial and exchange rate markets. Therefore, the more volatile oil prices become, the harder it will be for the yen to reverse its trend with a single interest rate hike.

IV. Technical structure indicates high-level consolidation rather than trend failure.

From the daily chart, the exchange rate rebounded quickly after a sharp drop to 155.025 and is currently trading above the Bollinger Middle Band at 158.417, near the Upper Band at 160.717. The MACD indicator shows the DIFF at 0.400 and the DEA at 0.263, with the histogram still positive, indicating that the recovery trend remains intact, but momentum has not expanded significantly.

Traders are truly focused on structural contradictions. If the exchange rate continues to approach 160, policy statements, liquidity, and option positions could amplify intraday volatility. A drop back to around 158.40 would mean the Bollinger Middle Band has once again become a balance line between bulls and bears, at which point the market will reassess whether the Bank of Japan's rate hike has been fully priced in. Currently, it's more like an event-pricing phase within a high-level trading range, rather than a one-way macroeconomic narrative.

Frequently Asked Questions

Question 1: If the Bank of Japan raises interest rates in June, will the USD/JPY exchange rate necessarily fall?

A: Not necessarily. If interest rate hikes have already been fully priced in, and there are simultaneous signals of a slowdown in bond purchases, the yen may receive limited support. The key lies in whether the subsequent interest rate path becomes clearer.

Question 2: Why is the 160 mark so sensitive?

A: It reflects policy attention, option positions, and the crowding of trend trading. Once the price repeatedly touches the level, volatility is usually amplified, but this does not necessarily mean that a one-sided market trend will occur.

Question 3: Why do oil prices affect the USD/JPY exchange rate?

A: High oil prices will increase Japan's import costs, compress corporate profits and residents' real income, and may also increase global inflation stickiness, prompting the Federal Reserve to remain cautious, ultimately affecting exchange rates through interest rate differentials and risk appetite.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.