A review of the US dollar's performance: Will historical crises repeat themselves?

2026-06-05 19:42:40

Recent complex news regarding the Middle East geopolitical situation has significantly impacted global foreign exchange market trends, providing strong support for the US dollar exchange rate. Meanwhile, the Federal Reserve's current monetary policy dilemma, inflationary environment, and external shocks are increasingly resembling the market and economic conditions of the 1970s, fueling ongoing discussions about a "history repeating itself."

Boosted by statements from US President Trump, the US dollar experienced a temporary rebound. Trump publicly stated that multiple rounds of negotiations between the US and Iran had entered their final stages, and that geopolitical tensions were expected to gradually ease. However, this statement contradicts statements from other parties. Iranian officials publicly denied any progress, explicitly stating that the negotiations between Iran and the US had not achieved any substantial breakthroughs. Furthermore, Hezbollah in Lebanon publicly refused to abide by the ceasefire agreement between Israel and Lebanon, which was led and enforced by the US. The multifaceted and contradictory developments in the Middle East have made the regional geopolitical situation increasingly unpredictable, significantly increasing market uncertainty and rapidly fueling global risk aversion. Large amounts of capital have flowed into traditional safe-haven assets such as the US dollar, further driving up demand for the dollar and stabilizing its exchange rate.

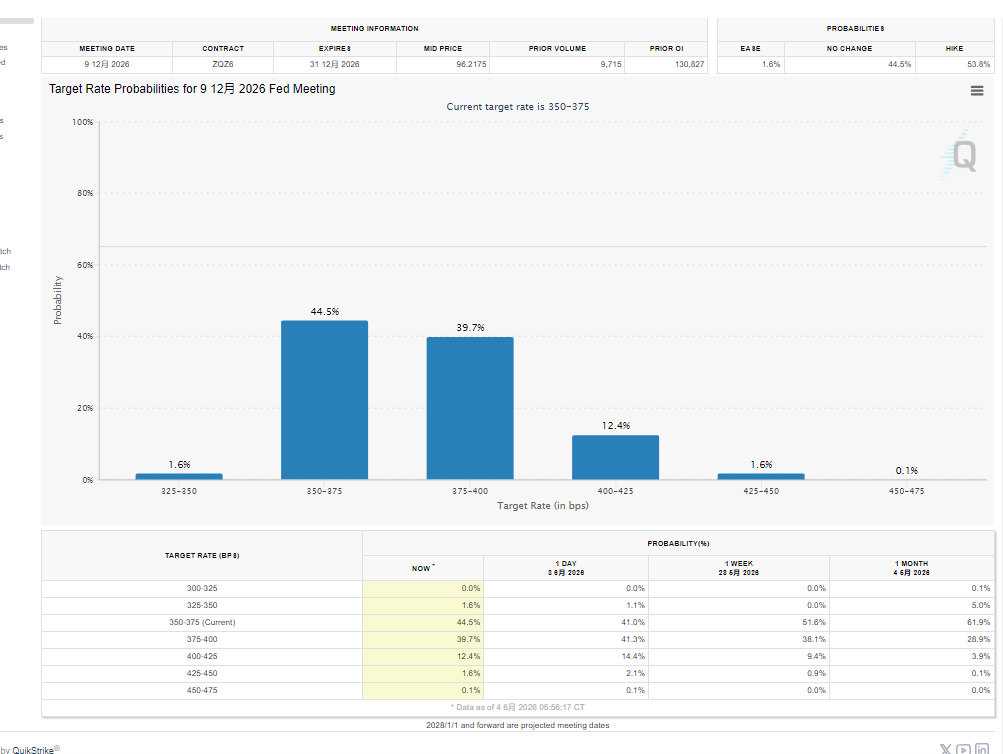

Market expectations for interest rate hikes have cooled, and the correlation between the US dollar and crude oil prices has changed.

(The probability of a year-end rate hike has fallen below 50% before the non-farm payrolls data is released)

Even though Brent crude oil prices have fallen in this round, leading to a corresponding decline in US Treasury yields, the US dollar exchange rate has remained stable, demonstrating strong resilience against declines.

From the perspective of market interest rate expectations, the probability of investors betting that the Federal Reserve will tighten monetary policy and raise interest rates while reducing its balance sheet in 2026 has fallen below 50%, and the likelihood of monetary policy tightening this year has decreased significantly. The latest market survey data from Bloomberg MLIV Pulse clearly shows the market divergence: among the professional investors surveyed, 45% believe that the US federal funds rate will remain at its current level throughout 2026 without adjustment; 35% of investors expect interest rate hikes and predict that the Federal Reserve will slightly tighten monetary policy; and another 15% of investors are optimistic about interest rate cuts this year. In addition, more than half of the market participants believe that the price linkage between the US dollar and international oil prices will continue to strengthen, and the correlation between their trends will further increase; meanwhile, more than one-third of investors predict that in the medium term, the US dollar index and Brent crude oil prices are likely to decline in tandem, and the market as a whole is cautious about the medium- to long-term trend of the US dollar.

Institutions predict a stronger euro, and expectations for a White House interest rate cut are rising.

Market consensus aligns with the aforementioned survey findings. Global mainstream institutions unanimously predict that the euro will continue to appreciate against the US dollar, exhibiting a steady upward trend in the short, medium, and long term, with target exchange rates of 1.18, 1.19, and 1.20 for 1 month, 3 months, and 12 months, respectively. The currently accepted baseline macroeconomic scenario is that the escalating Middle East geopolitical conflict will gradually subside and come to an end, at which point the Trump administration's focus will shift from complex overseas diplomatic affairs back to domestic economic governance. The market generally anticipates that the White House will then resume policy pressure on the Federal Reserve, continuously forcing the central bank to ease monetary policy and implement interest rate cuts to stimulate domestic economic growth.

A retrospective of the predicament of the 1970s: The oil crisis triggered stagflation and policy chaos.

Looking at the current global financial market trends and macroeconomic conditions, many core characteristics are highly consistent with the economic and financial environment of the 1970s, making the signal of historical recurrence increasingly clear. In the 1970s, a large-scale global oil crisis erupted, causing international oil prices to soar, directly triggering runaway inflation in the United States, with price levels rising continuously. However, at that time, under political pressure from the White House, the Federal Reserve did not take measures to curb inflation by raising interest rates and tightening monetary policy. Instead, it started a cycle of interest rate cuts against the trend. The continuous loose monetary policy further exacerbated the supply and demand imbalance, ultimately leading to a complete loss of control over US prices and persistently high inflation. In order to suppress hyperinflation, the Federal Reserve subsequently had to launch multiple rounds of aggressive and strong monetary tightening policies, raising interest rates sharply and tightening market liquidity. The drastic policy fluctuations severely impacted the real economy, ultimately plunging the US economy into a double-dip recession with two consecutive recessions.

The current economy is resilient enough to avoid the risk of history repeating itself.

However, compared to the dire situation of the 1970s, the current US economy possesses a stronger resilience and is highly likely to avoid a repeat of the stagflation crisis of that era. A special research report released by the Federal Reserve Bank of Boston provides a detailed argument for this: In recent years, US domestic crude oil production has continued to grow significantly, and energy self-sufficiency has increased substantially, completely changing the previous pattern of heavy reliance on imported crude oil. This has greatly enhanced the US economy's ability to withstand fluctuations in international oil prices and external oil shocks. Data comparison shows that the oil crisis of the 1970s directly pushed up US inflation by 2.2 percentage points, having a severe impact on prices; while at present, even if oil prices fluctuate significantly, it is expected to only increase US inflation by 1.5 percentage points, with price pressures clearly under control. Regarding employment, after the economic turmoil triggered by the oil crisis of the 1970s, the US unemployment rate soared by 1.8 percentage points, severely damaging the job market; while the current US labor market is resilient and continues to maintain a good momentum of continuous job creation. At least in the short term, the employment fundamentals have not shown signs of deterioration, providing solid support for stable economic operation.

Boosted by statements from US President Trump, the US dollar experienced a temporary rebound. Trump publicly stated that multiple rounds of negotiations between the US and Iran had entered their final stages, and that geopolitical tensions were expected to gradually ease. However, this statement contradicts statements from other parties. Iranian officials publicly denied any progress, explicitly stating that the negotiations between Iran and the US had not achieved any substantial breakthroughs. Furthermore, Hezbollah in Lebanon publicly refused to abide by the ceasefire agreement between Israel and Lebanon, which was led and enforced by the US. The multifaceted and contradictory developments in the Middle East have made the regional geopolitical situation increasingly unpredictable, significantly increasing market uncertainty and rapidly fueling global risk aversion. Large amounts of capital have flowed into traditional safe-haven assets such as the US dollar, further driving up demand for the dollar and stabilizing its exchange rate.

Market expectations for interest rate hikes have cooled, and the correlation between the US dollar and crude oil prices has changed.

(The probability of a year-end rate hike has fallen below 50% before the non-farm payrolls data is released)

Even though Brent crude oil prices have fallen in this round, leading to a corresponding decline in US Treasury yields, the US dollar exchange rate has remained stable, demonstrating strong resilience against declines.

From the perspective of market interest rate expectations, the probability of investors betting that the Federal Reserve will tighten monetary policy and raise interest rates while reducing its balance sheet in 2026 has fallen below 50%, and the likelihood of monetary policy tightening this year has decreased significantly. The latest market survey data from Bloomberg MLIV Pulse clearly shows the market divergence: among the professional investors surveyed, 45% believe that the US federal funds rate will remain at its current level throughout 2026 without adjustment; 35% of investors expect interest rate hikes and predict that the Federal Reserve will slightly tighten monetary policy; and another 15% of investors are optimistic about interest rate cuts this year. In addition, more than half of the market participants believe that the price linkage between the US dollar and international oil prices will continue to strengthen, and the correlation between their trends will further increase; meanwhile, more than one-third of investors predict that in the medium term, the US dollar index and Brent crude oil prices are likely to decline in tandem, and the market as a whole is cautious about the medium- to long-term trend of the US dollar.

Institutions predict a stronger euro, and expectations for a White House interest rate cut are rising.

Market consensus aligns with the aforementioned survey findings. Global mainstream institutions unanimously predict that the euro will continue to appreciate against the US dollar, exhibiting a steady upward trend in the short, medium, and long term, with target exchange rates of 1.18, 1.19, and 1.20 for 1 month, 3 months, and 12 months, respectively. The currently accepted baseline macroeconomic scenario is that the escalating Middle East geopolitical conflict will gradually subside and come to an end, at which point the Trump administration's focus will shift from complex overseas diplomatic affairs back to domestic economic governance. The market generally anticipates that the White House will then resume policy pressure on the Federal Reserve, continuously forcing the central bank to ease monetary policy and implement interest rate cuts to stimulate domestic economic growth.

A retrospective of the predicament of the 1970s: The oil crisis triggered stagflation and policy chaos.

Looking at the current global financial market trends and macroeconomic conditions, many core characteristics are highly consistent with the economic and financial environment of the 1970s, making the signal of historical recurrence increasingly clear. In the 1970s, a large-scale global oil crisis erupted, causing international oil prices to soar, directly triggering runaway inflation in the United States, with price levels rising continuously. However, at that time, under political pressure from the White House, the Federal Reserve did not take measures to curb inflation by raising interest rates and tightening monetary policy. Instead, it started a cycle of interest rate cuts against the trend. The continuous loose monetary policy further exacerbated the supply and demand imbalance, ultimately leading to a complete loss of control over US prices and persistently high inflation. In order to suppress hyperinflation, the Federal Reserve subsequently had to launch multiple rounds of aggressive and strong monetary tightening policies, raising interest rates sharply and tightening market liquidity. The drastic policy fluctuations severely impacted the real economy, ultimately plunging the US economy into a double-dip recession with two consecutive recessions.

The current economy is resilient enough to avoid the risk of history repeating itself.

However, compared to the dire situation of the 1970s, the current US economy possesses a stronger resilience and is highly likely to avoid a repeat of the stagflation crisis of that era. A special research report released by the Federal Reserve Bank of Boston provides a detailed argument for this: In recent years, US domestic crude oil production has continued to grow significantly, and energy self-sufficiency has increased substantially, completely changing the previous pattern of heavy reliance on imported crude oil. This has greatly enhanced the US economy's ability to withstand fluctuations in international oil prices and external oil shocks. Data comparison shows that the oil crisis of the 1970s directly pushed up US inflation by 2.2 percentage points, having a severe impact on prices; while at present, even if oil prices fluctuate significantly, it is expected to only increase US inflation by 1.5 percentage points, with price pressures clearly under control. Regarding employment, after the economic turmoil triggered by the oil crisis of the 1970s, the US unemployment rate soared by 1.8 percentage points, severely damaging the job market; while the current US labor market is resilient and continues to maintain a good momentum of continuous job creation. At least in the short term, the employment fundamentals have not shown signs of deterioration, providing solid support for stable economic operation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.