US and Japanese stocks stabilized at two-month highs, nearing the threshold for Japanese intervention at the end of April.

2026-06-08 11:42:51

On Monday (June 8), the global foreign exchange market witnessed a significant shift. Better-than-expected US non-farm payroll data completely reversed market expectations for monetary policy, pushing the US dollar to continue its upward trend and firmly establishing itself at a two-month high. Non-US currencies generally came under downward pressure, with the Japanese yen continuing its decline and gradually approaching the Bank of Japan's intervention range.

With the Australian market closed for the day, trading in the global currency market was relatively quiet in the morning session, but the US dollar continued its strong performance following the release of the non-farm payroll data, with its gains remaining solid.

The latest U.S. employment data for May showed that non-farm payrolls increased by 172,000, significantly exceeding market expectations and fully demonstrating the strong resilience of the U.S. labor market. Even in the face of continued energy price shocks, the job market has continued to expand.

Affected by the strengthening of the US dollar, major non-US currencies weakened across the board. The euro fell to a two-month low, the pound hit a three-week low, and the Australian dollar and New Zealand dollar also fell in tandem, hitting two-month lows.

Jonas Goltermann, chief market economist at Capital Economics, said that the U.S. labor market's counter-trend strength, coupled with inflationary pressures from energy supply shocks, has significantly increased the probability of the Federal Reserve tightening monetary policy this year . He predicts that the Fed will raise interest rates twice by 25 basis points later this year to hedge against inflation risks and balance the overheated job market.

In terms of geopolitics, the situation in the Middle East continues to disrupt global energy and financial markets. Reports indicate that US President Trump stated on Sunday that he would persuade Israeli Prime Minister Netanyahu to exercise restraint and refrain from retaliating following the Iranian missile strikes. This anticipated temporary easing of geopolitical tensions has further strengthened market expectations for a Federal Reserve interest rate hike.

Data from the CME FedWatch Tool shows that the market is currently pricing in a greater than 70% probability of a Fed rate hike in December, a significant increase from 45% a week ago.

The continued strengthening of the US dollar has intensified the pressure on the Japanese yen, with the exchange rate hovering in a high-risk zone and gradually approaching the Bank of Japan's intervention threshold. Currently, the yen has completely reversed all the gains made by the central bank's intervention last month. Previously, the Bank of Japan injected 11.7 trillion yen to stabilize the exchange rate, briefly halting the yen's decline, but failing to reverse its long-term weakness.

Julius Baer economist David Meier stated that the global shift towards hawkish monetary policies by major central banks, coupled with the Bank of Japan's slow progress in normalizing its policy and its persistent interest rate disadvantage, are the core reasons for the long-term pressure on the yen. He believes that official exchange rate intervention can only stabilize the market in the short term, and the yen's long-term trend ultimately depends on the Bank of Japan's monetary policy adjustments.

Market sources indicate that unless the Middle East conflict escalates significantly and disrupts global markets, the Bank of Japan is highly likely to raise interest rates this month.

Overall, strong US employment data has reshaped global monetary policy expectations, making a strong dollar unlikely to reverse in the short term, and non-US currencies will continue to face pressure. The pace of future Fed rate hikes, Bank of Japan policy adjustments, and the Middle East geopolitical situation will be the core factors driving global foreign exchange and capital market trends.

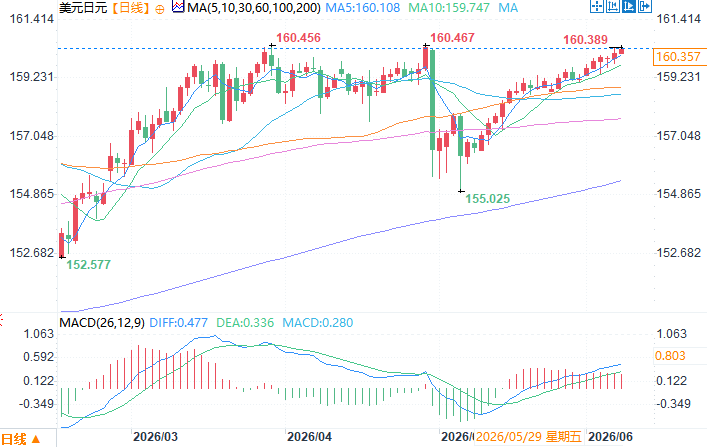

USD/JPY Daily Chart Source: EasyForex

At 11:42 AM Beijing time on June 8, the USD/JPY exchange rate was 160.35/36.

US non-farm payroll data for May exceeded expectations, causing the US dollar index to rise sharply.

With the Australian market closed for the day, trading in the global currency market was relatively quiet in the morning session, but the US dollar continued its strong performance following the release of the non-farm payroll data, with its gains remaining solid.

The latest U.S. employment data for May showed that non-farm payrolls increased by 172,000, significantly exceeding market expectations and fully demonstrating the strong resilience of the U.S. labor market. Even in the face of continued energy price shocks, the job market has continued to expand.

Affected by the strengthening of the US dollar, major non-US currencies weakened across the board. The euro fell to a two-month low, the pound hit a three-week low, and the Australian dollar and New Zealand dollar also fell in tandem, hitting two-month lows.

Jonas Goltermann, chief market economist at Capital Economics, said that the U.S. labor market's counter-trend strength, coupled with inflationary pressures from energy supply shocks, has significantly increased the probability of the Federal Reserve tightening monetary policy this year . He predicts that the Fed will raise interest rates twice by 25 basis points later this year to hedge against inflation risks and balance the overheated job market.

In terms of geopolitics, the situation in the Middle East continues to disrupt global energy and financial markets. Reports indicate that US President Trump stated on Sunday that he would persuade Israeli Prime Minister Netanyahu to exercise restraint and refrain from retaliating following the Iranian missile strikes. This anticipated temporary easing of geopolitical tensions has further strengthened market expectations for a Federal Reserve interest rate hike.

Data from the CME FedWatch Tool shows that the market is currently pricing in a greater than 70% probability of a Fed rate hike in December, a significant increase from 45% a week ago.

The yen remains under deep pressure as expectations for a Bank of Japan interest rate hike rise.

The continued strengthening of the US dollar has intensified the pressure on the Japanese yen, with the exchange rate hovering in a high-risk zone and gradually approaching the Bank of Japan's intervention threshold. Currently, the yen has completely reversed all the gains made by the central bank's intervention last month. Previously, the Bank of Japan injected 11.7 trillion yen to stabilize the exchange rate, briefly halting the yen's decline, but failing to reverse its long-term weakness.

Julius Baer economist David Meier stated that the global shift towards hawkish monetary policies by major central banks, coupled with the Bank of Japan's slow progress in normalizing its policy and its persistent interest rate disadvantage, are the core reasons for the long-term pressure on the yen. He believes that official exchange rate intervention can only stabilize the market in the short term, and the yen's long-term trend ultimately depends on the Bank of Japan's monetary policy adjustments.

Market sources indicate that unless the Middle East conflict escalates significantly and disrupts global markets, the Bank of Japan is highly likely to raise interest rates this month.

Summarize

Overall, strong US employment data has reshaped global monetary policy expectations, making a strong dollar unlikely to reverse in the short term, and non-US currencies will continue to face pressure. The pace of future Fed rate hikes, Bank of Japan policy adjustments, and the Middle East geopolitical situation will be the core factors driving global foreign exchange and capital market trends.

USD/JPY Daily Chart Source: EasyForex

At 11:42 AM Beijing time on June 8, the USD/JPY exchange rate was 160.35/36.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.