Warsh's long-awaited inflation report: May US CPI data showed a significant cooling, and inflationary pressures eased considerably.

2026-06-11 02:54:53

In May 2026, US inflation data reached a crucial cooling turning point, with core CPI showing a significant month-on-month decline. Inflation in core goods and services also weakened, shifting the overall inflation pattern from widespread inflation during the pandemic to structural price fluctuations, perfectly aligning with Federal Reserve Chairman Warsh's policy expectations. However, abnormal seasonal adjustments in the data and geopolitical risks in the Middle East have added uncertainty to the subsequent inflation trend and monetary policy path.

On June 11, 2026, the latest US May Consumer Price Index (CPI) report was released, with several core inflation indicators falling more than expected, becoming a key positive signal for the Federal Reserve's current anti-inflation cycle. This data significantly alleviated market concerns about high US inflation stickiness, with both core inflation figures falling below market consensus expectations, clearly indicating a cooling inflation trend, and precisely aligning with the inflation recovery anticipated by Federal Reserve Chairman Warsh. However, the continued escalation of geopolitical conflicts has also made the market's reaction to this positive inflation news more cautious.

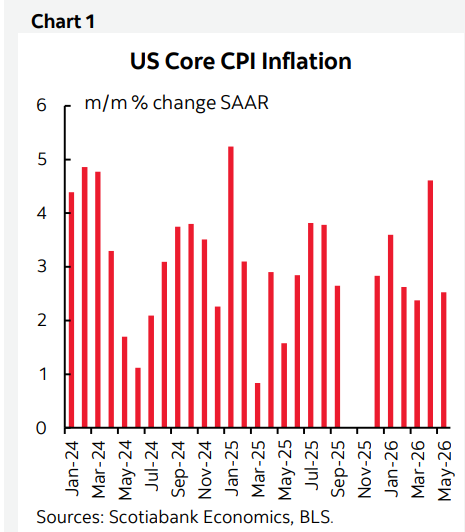

From a core data perspective, the US overall CPI rose 0.47% month-on-month in May, while the core CPI (excluding food and energy) increased by only 0.21%. Compared to market expectations, Scotia predicted overall and core CPI increases of 0.4% and 0.3% respectively, while the market consensus was 0.5% and 0.3%. The actual core CPI increase was significantly lower than the general market forecast, a strong performance. Meanwhile, the US overall and core CPI remained unchanged at 0.6% and 0.4% month-on-month in April, while the core CPI nearly halved in May, indicating a much stronger-than-expected decline in inflation, clearly reflecting a cooling trend in US inflation.

(US core CPI inflation trend)

The most significant change in this round of inflation data lies in the fundamental shift in the form of inflation. During the pandemic, US inflation exhibited a widespread and across-the-board rise, with prices for all categories of goods, services, energy, and food increasing simultaneously, resulting in comprehensive and persistent inflationary pressures. Currently, however, US inflation has completely transformed into a localized, relative price shock, no longer characterized by uncontrolled, widespread inflation. This is the core reason why this data has been recognized by the Federal Reserve.

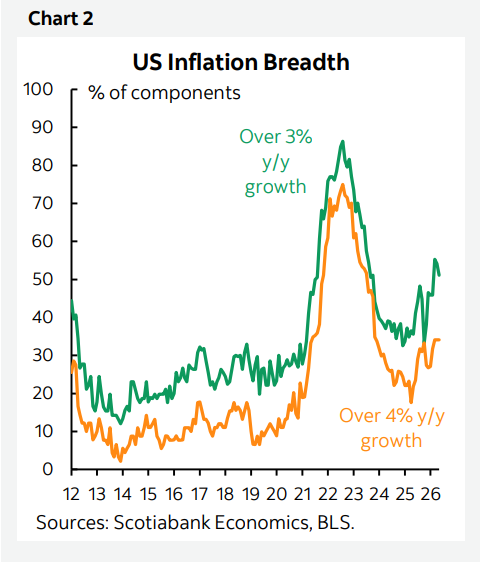

Inflation diffusion data clearly reflects the changes in the current inflation pattern, which is significantly different from the overall inflation during the pandemic. Data shows that currently, among the various categories of goods and services in the US CPI, only about one-third saw year-on-year price increases exceeding 4%, and less than half of the categories saw increases exceeding 3%. Compared to the widespread inflation during the pandemic, current inflationary pressures have significantly eased, the number of categories experiencing price increases has decreased markedly, and inflation is much more controllable. This is the core reason why Warsh is optimistic about the current inflation situation.

(Structure of inflation diffusion in the United States)

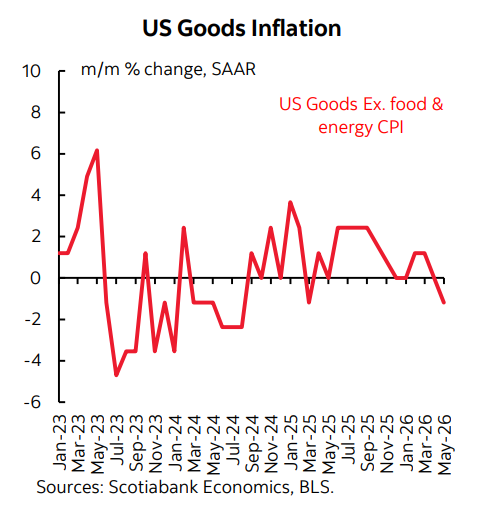

Looking at the breakdown of inflation, the weak performance of core commodity inflation is key to the current slowdown in inflation. In May, US core commodity prices fell 0.1% month-on-month. Excluding volatile categories such as food and energy, inflationary pressures on the commodity side have completely subsided. Over the past four months, US core commodity prices have remained generally stable, without any significant upward trend, completely resolving the previous problem of commodity inflation dragging down overall prices and becoming an important support for the decline in inflation.

(US core commodity inflation trend)

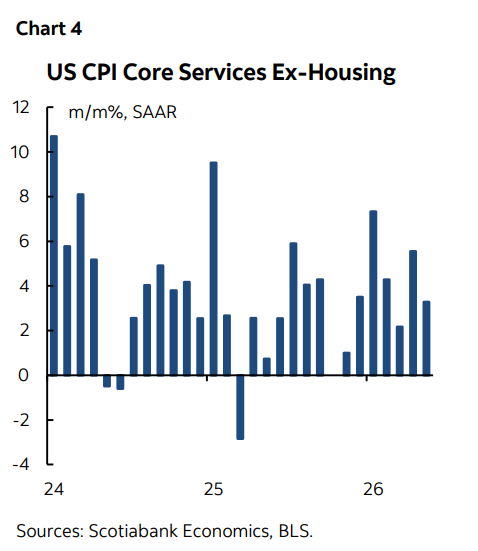

Inflation in core services also eased, further solidifying the cooling trend in inflation. Excluding housing and energy costs, the month-on-month increase in core service prices in the United States fell to 0.26% in May. While core service inflation has fluctuated significantly this year, overall, the increase this month was at a relatively stable and reasonable level, effectively alleviating the sticky pressure of inflation on the service sector.

(Inflation trends for core services excluding housing)

However, a significant anomaly exists in this inflation data, sparking controversy regarding its accuracy. Looking at the raw data, the unadjusted core CPI increase in May was relatively high compared to the historical average for May. Normally, May is a month of slight price increases due to seasonal fluctuations. However, the seasonal adjustment coefficient used this month was the lowest in modern history, only slightly lower than the historical extreme in May 1969. This extremely low adjustment coefficient artificially suppressed the final core CPI data, to some extent "beautifying" the effect of cooling inflation. This anomaly has raised questions about the accuracy and objectivity of official US inflation statistics, and the risk of subsequent revisions to inflation data cannot be ignored.

Following the release of inflation data, financial markets reacted simultaneously, with US Treasury yields declining sharply, particularly the 2-year Treasury yield. This signal of cooling inflation reflected the market's anticipation of further easing by the Federal Reserve, reigniting expectations of interest rate cuts. However, the market reaction was generally cautious and restrained, without significant volatility. The core constraint stemmed from geopolitical factors. The ongoing tensions in the Middle East and escalating geopolitical risks could not only disrupt the global energy supply landscape but also impact the global supply chain, posing new upward risks to future US inflation.

Geopolitical uncertainties have offset the positive impact of cooling inflation, leaving the market in a tug-of-war between "cooling data and rising risks." On the one hand, persistently weak short-term inflation data provides ample data support for the Federal Reserve to slow its tightening policy and begin a rate-cutting cycle. On the other hand, external risks such as the situation in the Middle East and potential disruptions to supply chains could reverse the current downward trend in inflation at any time, leading to repeated rebounds. With these mixed factors, the market is choosing to remain on the sidelines in the short term, limiting overall volatility.

Overall, the May CPI report is the most favorable data the Federal Reserve has released since its anti-inflation campaign began. Core inflation, goods inflation, and services inflation all improved simultaneously, and the inflation structure continued to optimize, completely reversing market concerns about sticky inflation. After removing the interference from statistical anomalies, the core trend of steady decline in US inflation remains unchanged, and overall inflationary pressure has shifted from "out of control" to "structurally manageable."

Looking ahead, the market will focus on two key variables: first, whether US inflation data will rebound as seasonal factors return to normal, and the authenticity and sustainability of the inflation slowdown remain to be verified; second, the evolution of the Middle East geopolitical situation, where a continued escalation of conflict could lead to a rebound in energy prices, potentially pushing up overall inflation again. For the Federal Reserve, this much-anticipated inflation data provides ample room for flexible adjustments to monetary policy, but geopolitical risks and data uncertainties also mean that the Fed is unlikely to quickly initiate a rate-cutting cycle in the short term, and will likely maintain a cautious and wait-and-see approach to its subsequent policy pace.

On June 11, 2026, the latest US May Consumer Price Index (CPI) report was released, with several core inflation indicators falling more than expected, becoming a key positive signal for the Federal Reserve's current anti-inflation cycle. This data significantly alleviated market concerns about high US inflation stickiness, with both core inflation figures falling below market consensus expectations, clearly indicating a cooling inflation trend, and precisely aligning with the inflation recovery anticipated by Federal Reserve Chairman Warsh. However, the continued escalation of geopolitical conflicts has also made the market's reaction to this positive inflation news more cautious.

From a core data perspective, the US overall CPI rose 0.47% month-on-month in May, while the core CPI (excluding food and energy) increased by only 0.21%. Compared to market expectations, Scotia predicted overall and core CPI increases of 0.4% and 0.3% respectively, while the market consensus was 0.5% and 0.3%. The actual core CPI increase was significantly lower than the general market forecast, a strong performance. Meanwhile, the US overall and core CPI remained unchanged at 0.6% and 0.4% month-on-month in April, while the core CPI nearly halved in May, indicating a much stronger-than-expected decline in inflation, clearly reflecting a cooling trend in US inflation.

(US core CPI inflation trend)

The most significant change in this round of inflation data lies in the fundamental shift in the form of inflation. During the pandemic, US inflation exhibited a widespread and across-the-board rise, with prices for all categories of goods, services, energy, and food increasing simultaneously, resulting in comprehensive and persistent inflationary pressures. Currently, however, US inflation has completely transformed into a localized, relative price shock, no longer characterized by uncontrolled, widespread inflation. This is the core reason why this data has been recognized by the Federal Reserve.

Inflation diffusion data clearly reflects the changes in the current inflation pattern, which is significantly different from the overall inflation during the pandemic. Data shows that currently, among the various categories of goods and services in the US CPI, only about one-third saw year-on-year price increases exceeding 4%, and less than half of the categories saw increases exceeding 3%. Compared to the widespread inflation during the pandemic, current inflationary pressures have significantly eased, the number of categories experiencing price increases has decreased markedly, and inflation is much more controllable. This is the core reason why Warsh is optimistic about the current inflation situation.

(Structure of inflation diffusion in the United States)

Looking at the breakdown of inflation, the weak performance of core commodity inflation is key to the current slowdown in inflation. In May, US core commodity prices fell 0.1% month-on-month. Excluding volatile categories such as food and energy, inflationary pressures on the commodity side have completely subsided. Over the past four months, US core commodity prices have remained generally stable, without any significant upward trend, completely resolving the previous problem of commodity inflation dragging down overall prices and becoming an important support for the decline in inflation.

(US core commodity inflation trend)

Inflation in core services also eased, further solidifying the cooling trend in inflation. Excluding housing and energy costs, the month-on-month increase in core service prices in the United States fell to 0.26% in May. While core service inflation has fluctuated significantly this year, overall, the increase this month was at a relatively stable and reasonable level, effectively alleviating the sticky pressure of inflation on the service sector.

(Inflation trends for core services excluding housing)

However, a significant anomaly exists in this inflation data, sparking controversy regarding its accuracy. Looking at the raw data, the unadjusted core CPI increase in May was relatively high compared to the historical average for May. Normally, May is a month of slight price increases due to seasonal fluctuations. However, the seasonal adjustment coefficient used this month was the lowest in modern history, only slightly lower than the historical extreme in May 1969. This extremely low adjustment coefficient artificially suppressed the final core CPI data, to some extent "beautifying" the effect of cooling inflation. This anomaly has raised questions about the accuracy and objectivity of official US inflation statistics, and the risk of subsequent revisions to inflation data cannot be ignored.

Following the release of inflation data, financial markets reacted simultaneously, with US Treasury yields declining sharply, particularly the 2-year Treasury yield. This signal of cooling inflation reflected the market's anticipation of further easing by the Federal Reserve, reigniting expectations of interest rate cuts. However, the market reaction was generally cautious and restrained, without significant volatility. The core constraint stemmed from geopolitical factors. The ongoing tensions in the Middle East and escalating geopolitical risks could not only disrupt the global energy supply landscape but also impact the global supply chain, posing new upward risks to future US inflation.

Geopolitical uncertainties have offset the positive impact of cooling inflation, leaving the market in a tug-of-war between "cooling data and rising risks." On the one hand, persistently weak short-term inflation data provides ample data support for the Federal Reserve to slow its tightening policy and begin a rate-cutting cycle. On the other hand, external risks such as the situation in the Middle East and potential disruptions to supply chains could reverse the current downward trend in inflation at any time, leading to repeated rebounds. With these mixed factors, the market is choosing to remain on the sidelines in the short term, limiting overall volatility.

Overall, the May CPI report is the most favorable data the Federal Reserve has released since its anti-inflation campaign began. Core inflation, goods inflation, and services inflation all improved simultaneously, and the inflation structure continued to optimize, completely reversing market concerns about sticky inflation. After removing the interference from statistical anomalies, the core trend of steady decline in US inflation remains unchanged, and overall inflationary pressure has shifted from "out of control" to "structurally manageable."

Looking ahead, the market will focus on two key variables: first, whether US inflation data will rebound as seasonal factors return to normal, and the authenticity and sustainability of the inflation slowdown remain to be verified; second, the evolution of the Middle East geopolitical situation, where a continued escalation of conflict could lead to a rebound in energy prices, potentially pushing up overall inflation again. For the Federal Reserve, this much-anticipated inflation data provides ample room for flexible adjustments to monetary policy, but geopolitical risks and data uncertainties also mean that the Fed is unlikely to quickly initiate a rate-cutting cycle in the short term, and will likely maintain a cautious and wait-and-see approach to its subsequent policy pace.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.