A chart shows that the Baltic Dry Index (BDI) declined slightly, with Capesize freight rates weakening significantly and dragging down the overall market.

2026-06-11 01:30:00

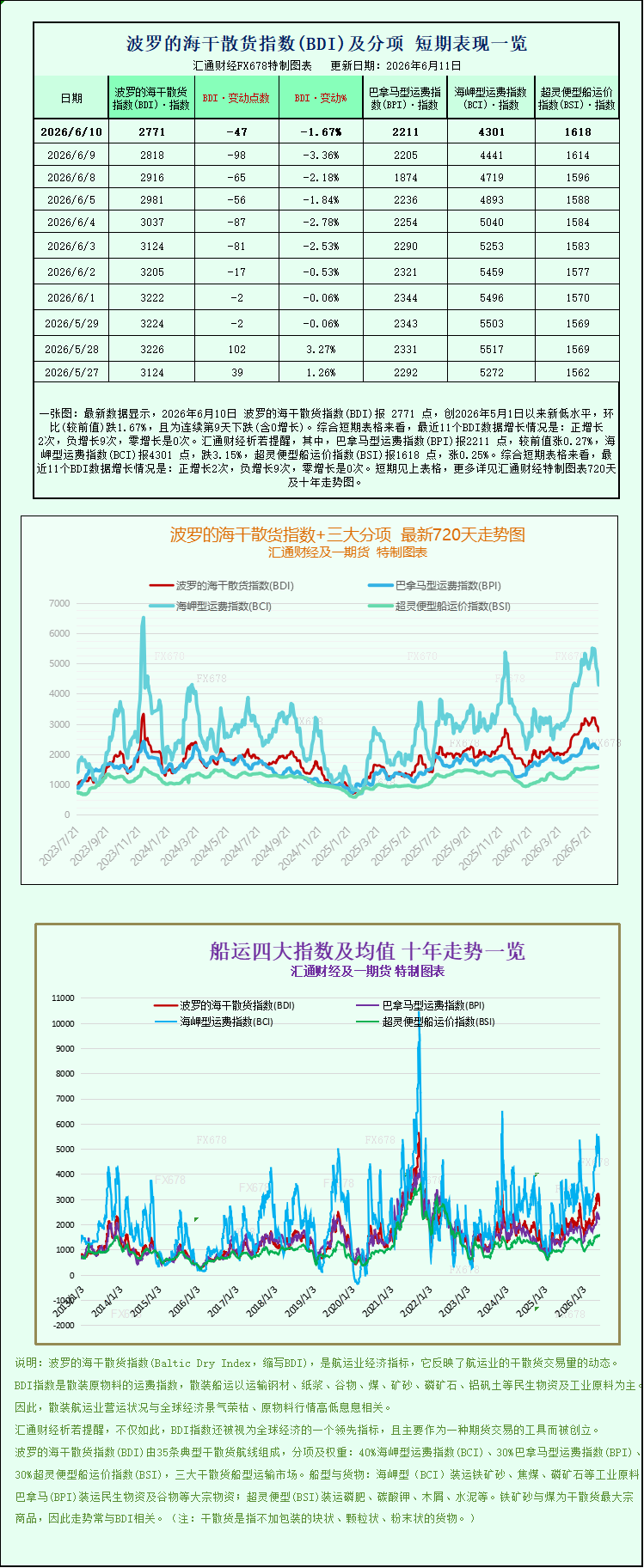

The latest data shows that the Baltic Dry Index (BDI) was 2771 points on June 10, 2026, a new low since May 1, 2026, down 1.67% month-on-month, marking the 9th consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 2 positive increases, 9 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2211 points, up 0.27% from the previous value; the Capesize Freight Index (BCI) was 4301 points, down 3.15%; and the Supramax Freight Index (BSI) was 1618 points, up 0.25%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

Recently, the international dry bulk shipping market has seen a structural divergence, with overall market activity cooling down. On Wednesday, June 10, the Baltic Dry Index (BDI) released by the Baltic Exchange declined slightly, primarily due to a significant drop in freight rates for Capesize vessels. Meanwhile, freight rates for Panamax and Supramax vessels bucked the trend with slight increases, demonstrating a clear divergence in market conditions across different vessel sizes and reflecting a structural adjustment in global demand for bulk commodities via sea freight.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (BDI) comprehensively covers spot freight rates for the three major vessel types: Capesize, Panamax, and Supramax. It directly reflects the global demand for seaborne industrial raw materials, food, and energy bulk cargoes, as well as market sentiment, and is also an important reference indicator for predicting the activity of global trade and industrial economies. Data on the day showed that the core index fell 47 points, a drop of 1.7%, closing at 2771 points, ending its previous period of stability, with the overall market freight rate center shifting slightly downward.

The core drag on this index decline was large Capesize vessels. Data shows that the Capesize vessel-specific index fell sharply by 140 points that day, a drop of 3.2%, closing at 4301 points. This decline far exceeded the overall market level, becoming the main factor pulling down the BDI index. In terms of actual operating revenue, the profit margins of Capesize vessels mainly engaged in long-distance bulk industrial raw material transportation have shrunk significantly. The average daily revenue of mainstream 150,000-ton Capesize vessels (mainly carrying heavy industrial raw materials such as iron ore and thermal coal) decreased by $1267, with the latest average daily revenue at $35,504, indicating a significant weakening of demand in the large industrial bulk shipping market.

Industry analysts point out that the sharp decline in Capesize freight rates is mainly due to a short-term mismatch between supply and demand. On the one hand, after the concentrated release of global iron ore and coal ocean shipping orders in the early stages, the follow-up of new orders in the short term was insufficient, resulting in a temporary gap in demand for long-haul ocean shipping. On the other hand, the effective supply of large vessels in the international dry bulk market has been relatively abundant recently, with some idle vessels returning to the market, further exacerbating the loose supply and demand situation and compressing shipowners' profit margins. Nevertheless, this round of freight rate decline has not resulted in a precipitous drop, and overall rates remain within a relatively reasonable range for the year, without a collapse in the industry's overall prosperity.

It is noteworthy that the shipping market and the commodity futures market have shown a subtle divergence. On Wednesday, domestic iron ore futures ended their five-day losing streak, experiencing a temporary rebound. The improved market sentiment was mainly supported by positive domestic trade data, with strong monthly steel export figures effectively boosting market confidence across the steel industry chain. Simultaneously, domestic iron ore imports declined, improving the supply-demand balance and stabilizing iron ore prices. However, the recovery in commodity prices did not quickly translate into the shipping market, primarily because shipping orders have a lag effect. Short-term demand for industrial raw materials via sea freight has not yet recovered in tandem, creating a short-term misalignment where "shipping prices rise while freight rates fall."

In contrast to the weak performance of large Capesize vessels, the market for small and medium-sized dry bulk carriers remained stable, showing an independent upward trend and highlighting the resilience of demand for civilian bulk cargo transportation. The Panamax index rose slightly by 6 points, or 0.3%, to close at 2211 points. Panamax vessels of 60,000 to 70,000 tons, primarily carrying coal, grain, and other consumer and basic energy bulk cargoes, saw their average daily revenue rise by $51 to $19,897, maintaining a stable profit margin.

Smaller Supramax vessels also performed steadily, with the Supramax index rising 4 points, or 0.3%, to close at 1618. These vessels offer greater flexibility and cover a wider range of routes, primarily handling small- to medium-volume bulk cargo transport such as grains, fertilizers, and building materials. They are less affected by the cyclical fluctuations of heavy industry and, supported by global daily essential trade, their freight rates have remained stable, offsetting some of the market pressure from the decline in larger vessel sizes.

The current market divergence is essentially a reflection of the structural recovery in the global economy. While demand for seaborne raw materials from heavy industry is experiencing a short-term correction, demand for essential bulk cargo such as food, basic energy, and building materials remains stable, leading to a significant divergence in freight rates across different vessel types. Industry analysts predict that future market trends will largely depend on the recovery pace of the domestic steel industry chain. If demand for iron ore and coal imports continues to recover, Capesize freight rates are expected to stop falling and rebound, driving a recovery in the overall market index; while smaller vessel types are likely to continue their stable, fluctuating trend.

Overall, the dry bulk shipping market cooled slightly on June 10, highlighting structural characteristics. In the short term, the market will remain in a state of supply and demand interplay. Going forward, continued attention should be paid to the pace of global commodity trade, domestic industrial operating rates, and changes in international shipping capacity, as these factors will dominate the trend of dry bulk freight rates in the next phase.

Recently, the international dry bulk shipping market has seen a structural divergence, with overall market activity cooling down. On Wednesday, June 10, the Baltic Dry Index (BDI) released by the Baltic Exchange declined slightly, primarily due to a significant drop in freight rates for Capesize vessels. Meanwhile, freight rates for Panamax and Supramax vessels bucked the trend with slight increases, demonstrating a clear divergence in market conditions across different vessel sizes and reflecting a structural adjustment in global demand for bulk commodities via sea freight.

As a core indicator of the global dry bulk shipping market, the Baltic Dry Index (BDI) comprehensively covers spot freight rates for the three major vessel types: Capesize, Panamax, and Supramax. It directly reflects the global demand for seaborne industrial raw materials, food, and energy bulk cargoes, as well as market sentiment, and is also an important reference indicator for predicting the activity of global trade and industrial economies. Data on the day showed that the core index fell 47 points, a drop of 1.7%, closing at 2771 points, ending its previous period of stability, with the overall market freight rate center shifting slightly downward.

The core drag on this index decline was large Capesize vessels. Data shows that the Capesize vessel-specific index fell sharply by 140 points that day, a drop of 3.2%, closing at 4301 points. This decline far exceeded the overall market level, becoming the main factor pulling down the BDI index. In terms of actual operating revenue, the profit margins of Capesize vessels mainly engaged in long-distance bulk industrial raw material transportation have shrunk significantly. The average daily revenue of mainstream 150,000-ton Capesize vessels (mainly carrying heavy industrial raw materials such as iron ore and thermal coal) decreased by $1267, with the latest average daily revenue at $35,504, indicating a significant weakening of demand in the large industrial bulk shipping market.

Industry analysts point out that the sharp decline in Capesize freight rates is mainly due to a short-term mismatch between supply and demand. On the one hand, after the concentrated release of global iron ore and coal ocean shipping orders in the early stages, the follow-up of new orders in the short term was insufficient, resulting in a temporary gap in demand for long-haul ocean shipping. On the other hand, the effective supply of large vessels in the international dry bulk market has been relatively abundant recently, with some idle vessels returning to the market, further exacerbating the loose supply and demand situation and compressing shipowners' profit margins. Nevertheless, this round of freight rate decline has not resulted in a precipitous drop, and overall rates remain within a relatively reasonable range for the year, without a collapse in the industry's overall prosperity.

It is noteworthy that the shipping market and the commodity futures market have shown a subtle divergence. On Wednesday, domestic iron ore futures ended their five-day losing streak, experiencing a temporary rebound. The improved market sentiment was mainly supported by positive domestic trade data, with strong monthly steel export figures effectively boosting market confidence across the steel industry chain. Simultaneously, domestic iron ore imports declined, improving the supply-demand balance and stabilizing iron ore prices. However, the recovery in commodity prices did not quickly translate into the shipping market, primarily because shipping orders have a lag effect. Short-term demand for industrial raw materials via sea freight has not yet recovered in tandem, creating a short-term misalignment where "shipping prices rise while freight rates fall."

In contrast to the weak performance of large Capesize vessels, the market for small and medium-sized dry bulk carriers remained stable, showing an independent upward trend and highlighting the resilience of demand for civilian bulk cargo transportation. The Panamax index rose slightly by 6 points, or 0.3%, to close at 2211 points. Panamax vessels of 60,000 to 70,000 tons, primarily carrying coal, grain, and other consumer and basic energy bulk cargoes, saw their average daily revenue rise by $51 to $19,897, maintaining a stable profit margin.

Smaller Supramax vessels also performed steadily, with the Supramax index rising 4 points, or 0.3%, to close at 1618. These vessels offer greater flexibility and cover a wider range of routes, primarily handling small- to medium-volume bulk cargo transport such as grains, fertilizers, and building materials. They are less affected by the cyclical fluctuations of heavy industry and, supported by global daily essential trade, their freight rates have remained stable, offsetting some of the market pressure from the decline in larger vessel sizes.

The current market divergence is essentially a reflection of the structural recovery in the global economy. While demand for seaborne raw materials from heavy industry is experiencing a short-term correction, demand for essential bulk cargo such as food, basic energy, and building materials remains stable, leading to a significant divergence in freight rates across different vessel types. Industry analysts predict that future market trends will largely depend on the recovery pace of the domestic steel industry chain. If demand for iron ore and coal imports continues to recover, Capesize freight rates are expected to stop falling and rebound, driving a recovery in the overall market index; while smaller vessel types are likely to continue their stable, fluctuating trend.

Overall, the dry bulk shipping market cooled slightly on June 10, highlighting structural characteristics. In the short term, the market will remain in a state of supply and demand interplay. Going forward, continued attention should be paid to the pace of global commodity trade, domestic industrial operating rates, and changes in international shipping capacity, as these factors will dominate the trend of dry bulk freight rates in the next phase.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.