A chart shows the Baltic Dry Index holding steady, with divergent trends across different ship types.

2026-06-12 23:58:25

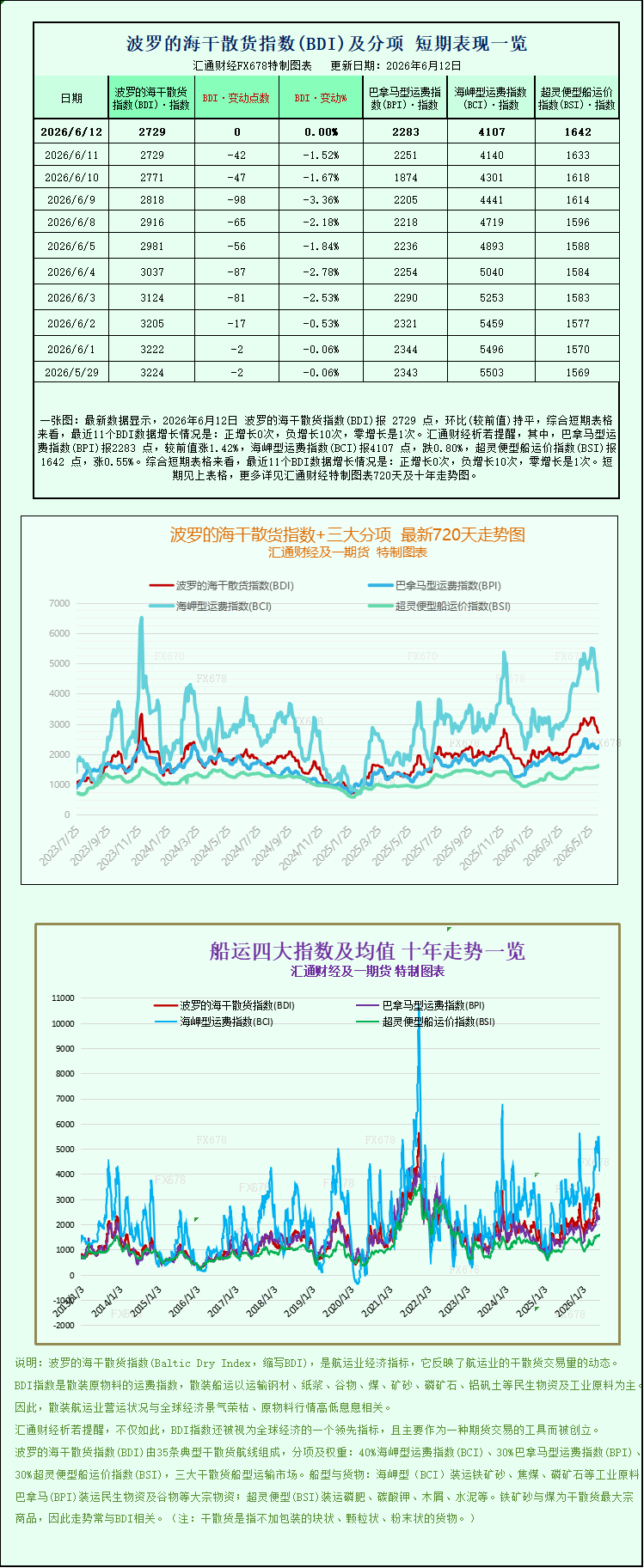

The latest data shows that on June 12, 2026, the Baltic Dry Index (BDI) was 2729 points, unchanged from the previous month. Looking at the short-term charts, the BDI saw the following changes over the last 11 trading days: 0 positive increases, 10 negative increases, and 1 zero increase. Specifically, the Panamax Freight Index (BPI) was 2283 points, up 1.42% from the previous month; the Capesize Freight Index (BCI) was 4107 points, down 0.80%; and the Supramax Freight Index (BSI) was 1642 points, up 0.55%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), which tracks global dry bulk shipping rates, stabilized on Friday, ending a multi-day decline. Looking at specific vessel types, the market exhibited significant structural divergence. Large Capesize vessels continued their downward trend, while Panamax and Supramax small and medium-sized bulk carriers bucked the trend with slight increases. This mixed performance across the three main vessel types fully reflects the differentiated supply and demand dynamics of the current global dry bulk shipping market.

Data shows that the core benchmark Baltic Dry Index remained unchanged at 2729 points on the day, with the market remaining stable without significant fluctuations. However, looking at the overall trend for the week, the market cooling trend was very obvious. The index fell sharply by 8.5% this week, marking the largest weekly drop in recent times and reaching a low point since May 1st, ending the strong performance of the previous two months despite the off-season. Industry analysts pointed out that the sharp correction in the index this week was mainly dragged down by the continued plunge in Capesize vessel freight rates, which have a higher weighting. The resilience of small and medium-sized vessels effectively supported the overall index, preventing further sharp declines and ultimately leading to the index stabilizing on Friday.

As the core benchmark for large vessels in the dry bulk market, Capesize vessels became the main drag on the market this week, with their weak performance continuing to worsen. Data shows that the Capesize index fell another 33 points on Friday, a daily drop of 0.8%, closing at 4107 points. The cumulative weekly drop reached a staggering 16.1%, far exceeding the overall index decline, making it the core driver of this market correction. Correspondingly, in terms of vessel revenue, Capesize vessels (150,000-ton deadweight class), primarily engaged in the ocean transport of bulk industrial raw materials such as iron ore and coal, saw their average daily revenue decline by $300, closing at $33,748, marking several consecutive trading days of declining revenue.

The continued weakness in Capesize freight rates is a result of the combined effects of supply-demand mismatch and fluctuations in the commodity market. From the capacity perspective, the recent concentrated release of empty vessels in the Pacific Ocean has led to a short-term oversupply, disrupting the previous tight supply-demand balance. This has significantly increased cargo owners' bargaining power, directly suppressing the upside potential of freight rates. From the demand side, weak demand in the end-user steel market has dragged down global iron ore procurement and transportation demand, becoming the core factor suppressing Capesize freight rates. On Friday, domestic Dalian iron ore futures prices also declined, with traders continuously navigating the market's bullish and bearish logic: on the one hand, the domestic steel industry's operating rate was lower than expected, resulting in sluggish end-user steel demand and suppressing iron ore spot procurement demand, thus hindering the release of ocean shipping orders; on the other hand, workers at BHP Billiton's core iron ore transportation hub in Australia voted to halt operations, triggering market concerns about a subsequent iron ore supply shortage. The offsetting bullish and bearish sentiments caused iron ore prices to fluctuate downwards, further exacerbating the wait-and-see attitude in the Capesize market and leading to continued downward pressure on freight rates.

In stark contrast to the weak performance of large Capesize vessels, the medium-sized Panamax market remained robust, bucking the trend and achieving an increase. Data shows that the Panamax index rose 32 points on Friday, a single-day increase of 1.4%, a strong performance, closing at 2283 points, with a cumulative weekly increase of 2.1%, demonstrating independent upward movement against the backdrop of a general market correction. Earnings data also improved, with Panamax vessels primarily engaged in the transportation of bulk commodities such as coal and grain (60,000 to 70,000 tons) seeing their average daily revenue rise by $290 to $20,545, indicating a steady recovery in profitability.

The recovery in Panamax vessel prices is primarily driven by the robust support from global grain and regional coal transportation demand. Currently, it is the peak season for grain trade in the Northern Hemisphere, with ongoing orders for grain shipments from North and South America, and Australia to Eurasia, providing stable demand support for medium-sized bulk carriers. Simultaneously, regional coal restocking demand is steadily recovering, with power plants in the Asia-Pacific and Europe replenishing their stocks in stages, driving a rebound in short- and medium-haul coal transportation demand. Compared to Capesize vessels, which are highly dependent on industrial bulk raw materials, Panamax vessels are better suited to consumer and regional energy trade, exhibiting stronger demand resilience. Coupled with the current moderate pace of medium-sized vessel capacity deployment and the absence of concentrated oversupply pressure, this has ultimately led to a rebound in freight rates against the overall market trend.

The small bulk carrier market also maintained a steady upward trend, with a continued positive outlook. The Supramax index rose 9 points on Friday, a daily increase of 0.6%, closing at 1642 points. This week's cumulative increase reached 3.4%, the highest weekly gain among the three major vessel types, demonstrating the most stable market performance. Supramax vessels, with their flexible deadweight tonnage and wide seaworthiness, primarily handle small-batch, multi-category, and multi-route bulk cargo transportation, covering diverse cargo types such as grains, building materials, and niche minerals. Market demand is broad, and they are less affected by fluctuations in the prices of any single commodity.

Industry analysts indicate that the current divergence in vessel types within the dry bulk market is highly persistent, primarily due to differences in cargo composition and supply-demand cycles across different vessel types. In the short term, Capesize vessels will remain in an adjustment cycle. The sluggish recovery in domestic steel demand is unlikely to reverse in the short term, and iron ore transportation demand may continue to be weak. Coupled with short-term overcapacity pressure, large vessel freight rates are likely to maintain a volatile and weak trend. Meanwhile, Panamax and Supramax vessels, supported by the peak season for grain trade and the resilience of demand for diversified cargoes, are expected to continue their resilience, with freight rates maintaining a steady and slightly upward trend.

From a medium- to long-term perspective, with the gradual recovery of global infrastructure demand and the continued release of new iron ore project capacity in the second half of the year, demand for ocean-going bulk commodity shipping is expected to recover, and the Capesize vessel market may be reaching a turning point. Meanwhile, smaller vessels will continue to benefit from the global flow of essential goods, and the overall market remains resilient. Subsequent market trends will largely depend on the progress of domestic end-user demand recovery, the development of the shutdown at Australian iron ore shipping hubs, and changes in the pace of global commodity trade.

The Baltic Dry Index (BDI), which tracks global dry bulk shipping rates, stabilized on Friday, ending a multi-day decline. Looking at specific vessel types, the market exhibited significant structural divergence. Large Capesize vessels continued their downward trend, while Panamax and Supramax small and medium-sized bulk carriers bucked the trend with slight increases. This mixed performance across the three main vessel types fully reflects the differentiated supply and demand dynamics of the current global dry bulk shipping market.

Data shows that the core benchmark Baltic Dry Index remained unchanged at 2729 points on the day, with the market remaining stable without significant fluctuations. However, looking at the overall trend for the week, the market cooling trend was very obvious. The index fell sharply by 8.5% this week, marking the largest weekly drop in recent times and reaching a low point since May 1st, ending the strong performance of the previous two months despite the off-season. Industry analysts pointed out that the sharp correction in the index this week was mainly dragged down by the continued plunge in Capesize vessel freight rates, which have a higher weighting. The resilience of small and medium-sized vessels effectively supported the overall index, preventing further sharp declines and ultimately leading to the index stabilizing on Friday.

As the core benchmark for large vessels in the dry bulk market, Capesize vessels became the main drag on the market this week, with their weak performance continuing to worsen. Data shows that the Capesize index fell another 33 points on Friday, a daily drop of 0.8%, closing at 4107 points. The cumulative weekly drop reached a staggering 16.1%, far exceeding the overall index decline, making it the core driver of this market correction. Correspondingly, in terms of vessel revenue, Capesize vessels (150,000-ton deadweight class), primarily engaged in the ocean transport of bulk industrial raw materials such as iron ore and coal, saw their average daily revenue decline by $300, closing at $33,748, marking several consecutive trading days of declining revenue.

The continued weakness in Capesize freight rates is a result of the combined effects of supply-demand mismatch and fluctuations in the commodity market. From the capacity perspective, the recent concentrated release of empty vessels in the Pacific Ocean has led to a short-term oversupply, disrupting the previous tight supply-demand balance. This has significantly increased cargo owners' bargaining power, directly suppressing the upside potential of freight rates. From the demand side, weak demand in the end-user steel market has dragged down global iron ore procurement and transportation demand, becoming the core factor suppressing Capesize freight rates. On Friday, domestic Dalian iron ore futures prices also declined, with traders continuously navigating the market's bullish and bearish logic: on the one hand, the domestic steel industry's operating rate was lower than expected, resulting in sluggish end-user steel demand and suppressing iron ore spot procurement demand, thus hindering the release of ocean shipping orders; on the other hand, workers at BHP Billiton's core iron ore transportation hub in Australia voted to halt operations, triggering market concerns about a subsequent iron ore supply shortage. The offsetting bullish and bearish sentiments caused iron ore prices to fluctuate downwards, further exacerbating the wait-and-see attitude in the Capesize market and leading to continued downward pressure on freight rates.

In stark contrast to the weak performance of large Capesize vessels, the medium-sized Panamax market remained robust, bucking the trend and achieving an increase. Data shows that the Panamax index rose 32 points on Friday, a single-day increase of 1.4%, a strong performance, closing at 2283 points, with a cumulative weekly increase of 2.1%, demonstrating independent upward movement against the backdrop of a general market correction. Earnings data also improved, with Panamax vessels primarily engaged in the transportation of bulk commodities such as coal and grain (60,000 to 70,000 tons) seeing their average daily revenue rise by $290 to $20,545, indicating a steady recovery in profitability.

The recovery in Panamax vessel prices is primarily driven by the robust support from global grain and regional coal transportation demand. Currently, it is the peak season for grain trade in the Northern Hemisphere, with ongoing orders for grain shipments from North and South America, and Australia to Eurasia, providing stable demand support for medium-sized bulk carriers. Simultaneously, regional coal restocking demand is steadily recovering, with power plants in the Asia-Pacific and Europe replenishing their stocks in stages, driving a rebound in short- and medium-haul coal transportation demand. Compared to Capesize vessels, which are highly dependent on industrial bulk raw materials, Panamax vessels are better suited to consumer and regional energy trade, exhibiting stronger demand resilience. Coupled with the current moderate pace of medium-sized vessel capacity deployment and the absence of concentrated oversupply pressure, this has ultimately led to a rebound in freight rates against the overall market trend.

The small bulk carrier market also maintained a steady upward trend, with a continued positive outlook. The Supramax index rose 9 points on Friday, a daily increase of 0.6%, closing at 1642 points. This week's cumulative increase reached 3.4%, the highest weekly gain among the three major vessel types, demonstrating the most stable market performance. Supramax vessels, with their flexible deadweight tonnage and wide seaworthiness, primarily handle small-batch, multi-category, and multi-route bulk cargo transportation, covering diverse cargo types such as grains, building materials, and niche minerals. Market demand is broad, and they are less affected by fluctuations in the prices of any single commodity.

Industry analysts indicate that the current divergence in vessel types within the dry bulk market is highly persistent, primarily due to differences in cargo composition and supply-demand cycles across different vessel types. In the short term, Capesize vessels will remain in an adjustment cycle. The sluggish recovery in domestic steel demand is unlikely to reverse in the short term, and iron ore transportation demand may continue to be weak. Coupled with short-term overcapacity pressure, large vessel freight rates are likely to maintain a volatile and weak trend. Meanwhile, Panamax and Supramax vessels, supported by the peak season for grain trade and the resilience of demand for diversified cargoes, are expected to continue their resilience, with freight rates maintaining a steady and slightly upward trend.

From a medium- to long-term perspective, with the gradual recovery of global infrastructure demand and the continued release of new iron ore project capacity in the second half of the year, demand for ocean-going bulk commodity shipping is expected to recover, and the Capesize vessel market may be reaching a turning point. Meanwhile, smaller vessels will continue to benefit from the global flow of essential goods, and the overall market remains resilient. Subsequent market trends will largely depend on the progress of domestic end-user demand recovery, the development of the shutdown at Australian iron ore shipping hubs, and changes in the pace of global commodity trade.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.