Will the Bank of Japan's impending interest rate hike save the persistently weak yen?

2026-06-13 01:08:57

The Bank of Japan (BOJ) will begin its fifth interest rate hike in this tightening cycle next Tuesday, raising the policy rate from 0.75% to 1.00%. This rate level will be the highest in Japan in nearly 31 years and is a key step in the BOJ's continued tightening of monetary policy after exiting negative interest rate policy. Throughout this rate hike cycle, the BOJ has released hawkish policy signals before each interest rate decision, and this meeting is no exception. In his public speech on June 3, BOJ Governor Kazuo Ueda clearly signaled a firm commitment to raising interest rates, essentially locking in the 25 basis point hike, which the market had already largely anticipated.

However, market sentiment remains cautious, with financial markets currently pricing in only about a 90% probability of an interest rate hike. The reason for the lack of a 100% consensus is primarily due to persistent market skepticism regarding the Bank of Japan's resolve and sustainability in normalizing monetary policy. This lingering doubt not only influences interest rate trends but also acts as a key factor suppressing the yen's exchange rate. Meanwhile, shipping disruptions in the Strait of Hormuz and pressure on energy supply chains, coupled with persistently high global oil and gas prices, have fueled Bank of Japan policymakers' growing concern that inflation could have a second-hand transmission effect, spreading from the energy sector to all industries and triggering widespread price increases. This is also a significant factor compelling this interest rate hike.

While the CPI data appears to be declining, inflationary pressures are actually accumulating.

As a core waterway for global energy transport, the Strait of Hormuz is currently experiencing oil and gas transport volumes at extremely low levels compared to before the conflict. The longer the shipping disruptions continue, the greater the risk of high-priced energy being transmitted to various industries in Japan, and the pressure of widespread imported inflation will continue to rise.

Superficially, Japan's inflation level appears to be temporarily declining, but this trend is not due to an endogenous economic slowdown; it relies entirely on government-backed subsidies to support people's livelihoods. To alleviate the cost of living pressure on the public, the Japanese government has introduced several livelihood support measures, with special subsidies for fuel and education being the most effective. As a result, Japan's overall CPI and core CPI both fell to 1.4% year-on-year in April. Furthermore, the Sanae Takaichi government announced a new fiscal stimulus package, planning to further increase energy subsidies from July to September to further reduce residential electricity and gas costs, thus offsetting upward inflationary pressures in the short term.

However, stripping away the veneer of policy intervention, the real price pressures in the Japanese market are continuing to mount. Since 2026, the growth rate of employee wages in Japanese companies has remained stable at over 3% for most of the time. A 3% wage growth rate is a core critical criterion for the Bank of Japan to determine whether inflation can stably anchor itself to its 2% policy target. Sustained wage increases mean that Japan has established a positive cycle of "wages-inflation." At the same time, the continued depreciation of the yen has significantly increased import costs. Coupled with the double impact of soaring international oil prices, production costs in Japan's industrial sector have risen rapidly. In recent months, the producer price index has accelerated significantly, and the upward pressure on upstream prices is gradually being transmitted to downstream consumers. The potential inflationary risk cannot be ignored.

The Bank of Japan's policy path is caught in a dilemma, with the pace of interest rate hikes highly controversial.

Since initiating its tightening cycle in March 2024, the Bank of Japan has raised interest rates multiple times. However, constrained by its long-term loose monetary policy and lagging policy adjustments, Japan's real interest rate remains in negative territory. This means that Japan's current monetary policy maintains a strong easing character overall. The Bank of Japan has repeatedly emphasized this point, intending to signal to the market that there is still ample room for further interest rate hikes and that the monetary tightening process is not over. However, there is significant disagreement in the market. Many believe that the Bank of Japan has long lagged behind the economic situation. Faced with persistently rising inflationary pressures and a recovering job market, the central bank should accelerate the pace of interest rate hikes and intensify tightening, rather than proceeding gradually and slowly.

The political upheavals in Japan have further exacerbated policy uncertainty. Since Sanae Takaichi became Prime Minister of Japan, the new government has consistently expressed clear opposition to interest rate hikes, fearing that tight monetary policy would stifle economic recovery and increase the burden on businesses and debt. This has greatly hampered the Bank of Japan's hawkish interest rate path, leaving policymakers in a dilemma.

Policy disagreements have also directly dragged down the yen's exchange rate. Since Sanae Takashi took office, the yen has been continuously sold off in the market, and its exchange rate has weakened. Coupled with the energy crisis triggered by geopolitical conflicts in the Middle East, the market has further lowered its expectations for aggressive interest rate hikes by the Bank of Japan. Investors generally believe that against the backdrop of escalating external risks, the Bank of Japan will prioritize ensuring economic growth rather than focusing on curbing inflation, which has further amplified the downward pressure on the yen.

Japanese bond yields surged, while the yen's exchange rate bucked the trend and remained weak.

In stark contrast to the weak yen, yields on long-term Japanese government bonds have risen sharply. The yield on 10-year Japanese government bonds climbed to a near 30-year high, while the yield on 30-year bonds hit a record low, indicating a clear upward trend in long-term interest rates. However, the core driver of this yield surge is not inflation expectations, but rather market concerns about the continued rise in Japan's government debt. Japan's total government debt has remained high for years, and the accumulating debt risk has become the core factor dominating long-term interest rates. Therefore, the rise in interest rates has not provided an effective boost to the yen's exchange rate, and the yen has remained in a weak and volatile pattern.

Even though the Bank of Japan raised interest rates by 25 basis points as expected this Tuesday, the market generally anticipates that its overall policy stance will not undergo a fundamental shift, and it will most likely continue its moderate tightening tone. If the central bank fails to release a strong hawkish signal of accelerated tightening and continued interest rate hikes, the yen's depreciation predicament will be difficult to reverse, and it will continue to face downward pressure.

The deputy governor presided over the decision-making press conference, which became a key factor in the yen's exchange rate movement.

Due to the unexpected hospitalization of Kazuo Ueda, the interest rate decision meeting on June 16 will be chaired by Vice Governor Ryozo Himo. This is the first time in this interest rate hike cycle that a policy meeting not led by the governor has been held, increasing the uncertainty surrounding the meeting's decision-making tone. The subsequent major press conference will be held by another vice governor, Shinichi Uchida, whose remarks will be crucial in influencing the short-term yen's exchange rate.

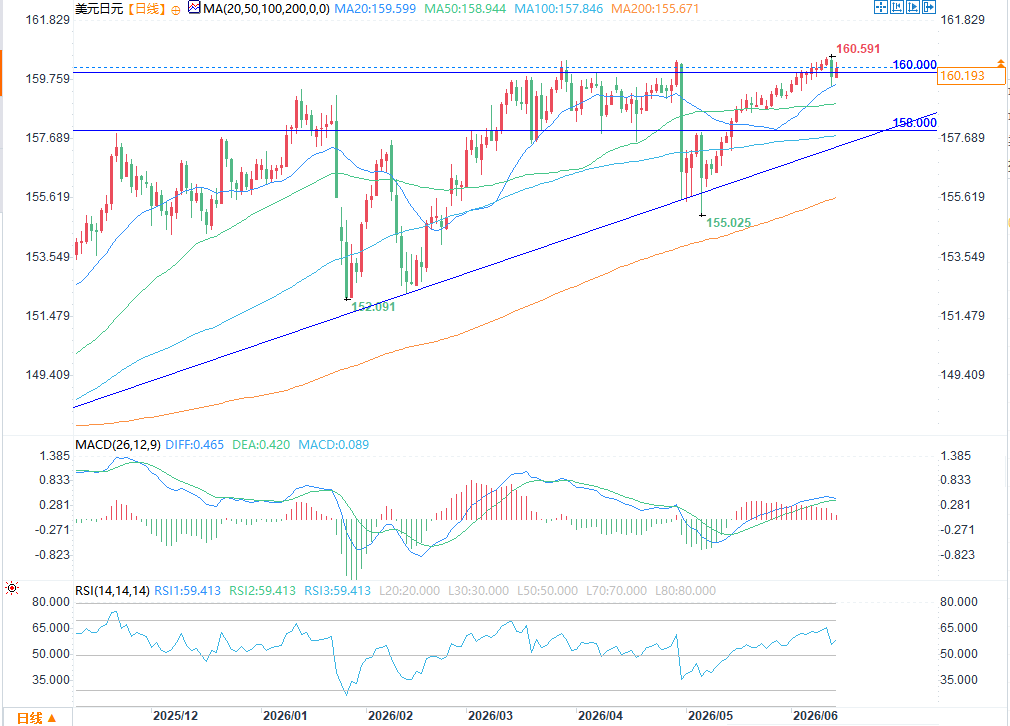

Regardless of which executive speaks, their wording will be extremely cautious. The market has very low tolerance for hawkish policy stances; even the slightest dovish or weaker-than-expected signal could trigger a new wave of yen selling. Currently, the USD/JPY exchange rate is testing the key 160 level. If the current policy decision and press conference are generally dovish and lack sufficient tightening力度, the USD/JPY exchange rate will likely break through the upper resistance level and rise further to the 162 mark, further worsening the yen's depreciation trend.

(USD/JPY daily chart source: EasyForex)

Conversely, if Shinichi Uchida releases an unexpectedly hawkish signal, while it may temporarily suppress dollar bulls and boost the yen, the yen's rebound will be very limited without government intervention, making it difficult to break through the short-term upward trend line. If the USD/JPY exchange rate surges rapidly and the yen's depreciation spirals out of control, the Japanese government will likely intervene in the market. If intervention occurs, the first target for yen bulls is the 155 level, and a break above that could lead to a further target of 152.50, at which point the yen will likely experience a period of recovery.

For forex traders, the biggest risk in this market movement lies in the mismatch between policy and intervention timing. The Japanese government is highly unlikely to intervene on the day of the Bank of Japan's decision, instead choosing to wait for the Federal Reserve's interest rate decision the following day before taking action. Even if the Bank of Japan temporarily stabilizes the yen's decline through interest rate hikes and hawkish statements, if the Federal Reserve adopts a hawkish stance this Wednesday and withdraws its monetary easing tendencies, the US-Japan interest rate differential will widen again, potentially erasing all of the yen's short-term gains and plunging it back into depreciation pressure.

However, market sentiment remains cautious, with financial markets currently pricing in only about a 90% probability of an interest rate hike. The reason for the lack of a 100% consensus is primarily due to persistent market skepticism regarding the Bank of Japan's resolve and sustainability in normalizing monetary policy. This lingering doubt not only influences interest rate trends but also acts as a key factor suppressing the yen's exchange rate. Meanwhile, shipping disruptions in the Strait of Hormuz and pressure on energy supply chains, coupled with persistently high global oil and gas prices, have fueled Bank of Japan policymakers' growing concern that inflation could have a second-hand transmission effect, spreading from the energy sector to all industries and triggering widespread price increases. This is also a significant factor compelling this interest rate hike.

While the CPI data appears to be declining, inflationary pressures are actually accumulating.

As a core waterway for global energy transport, the Strait of Hormuz is currently experiencing oil and gas transport volumes at extremely low levels compared to before the conflict. The longer the shipping disruptions continue, the greater the risk of high-priced energy being transmitted to various industries in Japan, and the pressure of widespread imported inflation will continue to rise.

Superficially, Japan's inflation level appears to be temporarily declining, but this trend is not due to an endogenous economic slowdown; it relies entirely on government-backed subsidies to support people's livelihoods. To alleviate the cost of living pressure on the public, the Japanese government has introduced several livelihood support measures, with special subsidies for fuel and education being the most effective. As a result, Japan's overall CPI and core CPI both fell to 1.4% year-on-year in April. Furthermore, the Sanae Takaichi government announced a new fiscal stimulus package, planning to further increase energy subsidies from July to September to further reduce residential electricity and gas costs, thus offsetting upward inflationary pressures in the short term.

However, stripping away the veneer of policy intervention, the real price pressures in the Japanese market are continuing to mount. Since 2026, the growth rate of employee wages in Japanese companies has remained stable at over 3% for most of the time. A 3% wage growth rate is a core critical criterion for the Bank of Japan to determine whether inflation can stably anchor itself to its 2% policy target. Sustained wage increases mean that Japan has established a positive cycle of "wages-inflation." At the same time, the continued depreciation of the yen has significantly increased import costs. Coupled with the double impact of soaring international oil prices, production costs in Japan's industrial sector have risen rapidly. In recent months, the producer price index has accelerated significantly, and the upward pressure on upstream prices is gradually being transmitted to downstream consumers. The potential inflationary risk cannot be ignored.

The Bank of Japan's policy path is caught in a dilemma, with the pace of interest rate hikes highly controversial.

Since initiating its tightening cycle in March 2024, the Bank of Japan has raised interest rates multiple times. However, constrained by its long-term loose monetary policy and lagging policy adjustments, Japan's real interest rate remains in negative territory. This means that Japan's current monetary policy maintains a strong easing character overall. The Bank of Japan has repeatedly emphasized this point, intending to signal to the market that there is still ample room for further interest rate hikes and that the monetary tightening process is not over. However, there is significant disagreement in the market. Many believe that the Bank of Japan has long lagged behind the economic situation. Faced with persistently rising inflationary pressures and a recovering job market, the central bank should accelerate the pace of interest rate hikes and intensify tightening, rather than proceeding gradually and slowly.

The political upheavals in Japan have further exacerbated policy uncertainty. Since Sanae Takaichi became Prime Minister of Japan, the new government has consistently expressed clear opposition to interest rate hikes, fearing that tight monetary policy would stifle economic recovery and increase the burden on businesses and debt. This has greatly hampered the Bank of Japan's hawkish interest rate path, leaving policymakers in a dilemma.

Policy disagreements have also directly dragged down the yen's exchange rate. Since Sanae Takashi took office, the yen has been continuously sold off in the market, and its exchange rate has weakened. Coupled with the energy crisis triggered by geopolitical conflicts in the Middle East, the market has further lowered its expectations for aggressive interest rate hikes by the Bank of Japan. Investors generally believe that against the backdrop of escalating external risks, the Bank of Japan will prioritize ensuring economic growth rather than focusing on curbing inflation, which has further amplified the downward pressure on the yen.

Japanese bond yields surged, while the yen's exchange rate bucked the trend and remained weak.

In stark contrast to the weak yen, yields on long-term Japanese government bonds have risen sharply. The yield on 10-year Japanese government bonds climbed to a near 30-year high, while the yield on 30-year bonds hit a record low, indicating a clear upward trend in long-term interest rates. However, the core driver of this yield surge is not inflation expectations, but rather market concerns about the continued rise in Japan's government debt. Japan's total government debt has remained high for years, and the accumulating debt risk has become the core factor dominating long-term interest rates. Therefore, the rise in interest rates has not provided an effective boost to the yen's exchange rate, and the yen has remained in a weak and volatile pattern.

Even though the Bank of Japan raised interest rates by 25 basis points as expected this Tuesday, the market generally anticipates that its overall policy stance will not undergo a fundamental shift, and it will most likely continue its moderate tightening tone. If the central bank fails to release a strong hawkish signal of accelerated tightening and continued interest rate hikes, the yen's depreciation predicament will be difficult to reverse, and it will continue to face downward pressure.

The deputy governor presided over the decision-making press conference, which became a key factor in the yen's exchange rate movement.

Due to the unexpected hospitalization of Kazuo Ueda, the interest rate decision meeting on June 16 will be chaired by Vice Governor Ryozo Himo. This is the first time in this interest rate hike cycle that a policy meeting not led by the governor has been held, increasing the uncertainty surrounding the meeting's decision-making tone. The subsequent major press conference will be held by another vice governor, Shinichi Uchida, whose remarks will be crucial in influencing the short-term yen's exchange rate.

Regardless of which executive speaks, their wording will be extremely cautious. The market has very low tolerance for hawkish policy stances; even the slightest dovish or weaker-than-expected signal could trigger a new wave of yen selling. Currently, the USD/JPY exchange rate is testing the key 160 level. If the current policy decision and press conference are generally dovish and lack sufficient tightening力度, the USD/JPY exchange rate will likely break through the upper resistance level and rise further to the 162 mark, further worsening the yen's depreciation trend.

(USD/JPY daily chart source: EasyForex)

Conversely, if Shinichi Uchida releases an unexpectedly hawkish signal, while it may temporarily suppress dollar bulls and boost the yen, the yen's rebound will be very limited without government intervention, making it difficult to break through the short-term upward trend line. If the USD/JPY exchange rate surges rapidly and the yen's depreciation spirals out of control, the Japanese government will likely intervene in the market. If intervention occurs, the first target for yen bulls is the 155 level, and a break above that could lead to a further target of 152.50, at which point the yen will likely experience a period of recovery.

For forex traders, the biggest risk in this market movement lies in the mismatch between policy and intervention timing. The Japanese government is highly unlikely to intervene on the day of the Bank of Japan's decision, instead choosing to wait for the Federal Reserve's interest rate decision the following day before taking action. Even if the Bank of Japan temporarily stabilizes the yen's decline through interest rate hikes and hawkish statements, if the Federal Reserve adopts a hawkish stance this Wednesday and withdraws its monetary easing tendencies, the US-Japan interest rate differential will widen again, potentially erasing all of the yen's short-term gains and plunging it back into depreciation pressure.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.