One chart: The Baltic Dry Index has fallen across the board, and freight rates for all types of vessels have declined in tandem.

2026-06-22 23:43:02

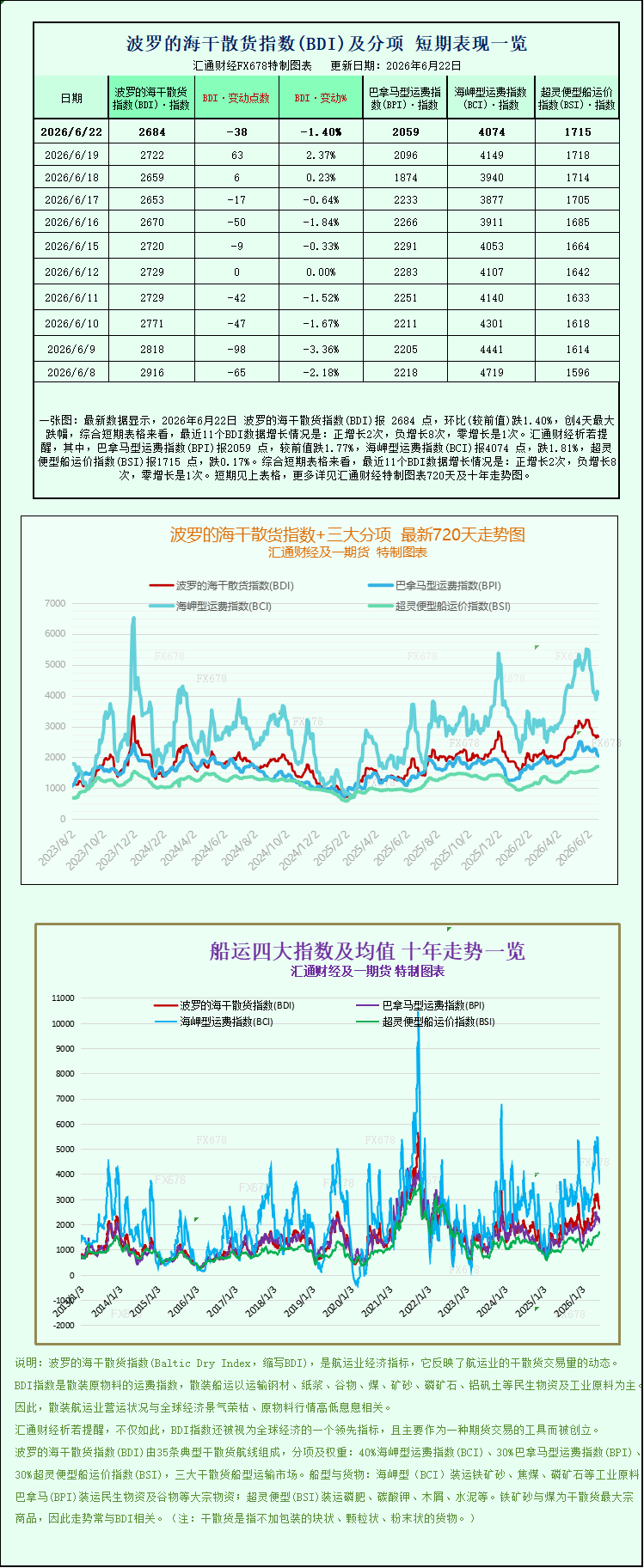

The latest data shows that on June 22, 2026, the Baltic Dry Index (BDI) was 2684 points, a decrease of 1.40% compared to the previous period, marking the largest drop in four days. Looking at the short-term charts, the recent 11 BDI data points show: positive growth twice, negative growth eight times, and zero growth once. Specifically, the Panamax Freight Index (BPI) was 2059 points, down 1.77% from the previous period; the Capesize Freight Index (BCI) was 4074 points, down 1.81%; and the Supramax Freight Index (BSI) was 1715 points, down 0.17%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 22, 2026, the latest shipping market data showed that the Baltic Dry Index (BADI), a core indicator of international shipping trends, experienced a significant correction. All categories of dry bulk vessels, including large, medium, and small vessels, were under pressure, with both the index level and average daily freight rates declining, ending the previous partial market recovery. As a key indicator of global dry bulk shipping trade, the across-the-board decline in the BADI directly reflects the current industry situation of cooling global demand for bulk commodities and slight adjustments in the supply-demand pattern, sending an important signal for the dry bulk shipping market trend in the second half of the year.

Data shows that on June 22, the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—fell sharply by 38 points, a 1.4% overall decline, closing at 2684 points. The index showed a continued downward trend throughout the day, with no significant rebound. This decline was not a structural adjustment specific to a single vessel type, but rather a general downturn across the entire sector. The indices for all three major vessel types and their operating earnings all fell to varying degrees, completely reversing the previous recovery trend for some vessel types, and market sentiment became more cautious.

In the large dry bulk carrier sector, Capesize vessels remained the primary drag on the index, exhibiting the most significant market volatility. The Baltic Capesize index fell 75 points, or 1.8%, to close at 4074 points. Notably, this index had just reached its highest point since June 10th in the previous trading day, highlighting the instability of the large bulk carrier market. In terms of actual operating earnings, the average daily earnings for Capesize bulk carriers plummeted by $684 to $33,444 per day.

As large dry bulk carriers with a deadweight tonnage of 150,000 tons, Capesize vessels primarily undertake ocean-going transportation of bulk industrial raw materials such as iron ore, thermal coal, and coking coal. Their freight rate fluctuations are deeply tied to the global industrial supply chain and commodity prices. The recent sharp decline in profits is primarily due to changes in supply and demand in the Chinese coal market. Recently, domestic coking coal futures prices have continued to fall, market sentiment is weak, and the resumption of production in core coal-producing areas of Shanxi has accelerated, leading to rising market expectations for increased domestic coal supply and significantly weakening domestic demand for imported coking coal. Simultaneously, the previous period of concentrated coal import replenishment has ended, import growth has slowed, and ocean-going coal transportation orders have decreased significantly, directly resulting in a decline in demand for large bulk carrier capacity and consequently putting downward pressure on freight rates.

The medium-sized dry bulk carrier market also failed to maintain its recovery trend, with Panamax freight rates declining in tandem, matching the drop in rates for larger vessels. The Panamax index fell 37 points, or 1.8%, to close at 2059 points; corresponding to an average daily earnings per vessel decrease of $328, to $18,532 per day. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are the mainstay of global shipping of mid-range bulk commodities such as industrial coal, grain, and agricultural inputs. They are widely used on transatlantic and transpacific short-to-medium-haul ocean routes, boasting broad market coverage and strong demand representation.

The decline in freight rates for this vessel type is due to two main factors. First, it is influenced by the overall weakness in global industrial demand, with a slight decrease in the operating rate of overseas manufacturing and a contraction in demand for industrial coal transportation. Second, the global grain shipping market has entered a period of relative stability, with a slowdown in grain exports from major producing regions such as North and South America and Australia. This has resulted in insufficient growth in grain shipping orders, coupled with the redeployment of some idle shipping capacity after the previous market recovery, leading to a slight increase in market supply and a more relaxed supply-demand balance. Ultimately, this has driven a steady decline in Panamax vessel freight rates. Compared to larger vessel types, the decline in Panamax vessel rates is relatively moderate, but the overall downward trend confirms the overall cooling of demand in the dry bulk shipping market.

While the decline in the small dry bulk carrier market narrowed relatively, it continued its weak trend, with the downward trend spreading across the entire industry. The Supramax vessel index fell slightly by 3 points, or 0.2%, to close at 1715 points. Supramax vessels primarily handle short-haul, small-volume dry bulk cargo transportation, offering more flexible routes and adaptability to a wider range of cargoes. They are relatively less affected by fluctuations in the bulk raw material market, hence their decline was much smaller than that of medium and large-sized vessels. However, the decline in this vessel type index indicates that the current shipping market adjustment has covered all vessel classes, lacking a structural market trend, and the overall market sentiment continues to decline.

In summary, the overall weakening of the Baltic Dry Index is the result of a combination of factors, including short-term supply-demand mismatch, commodity market volatility, and adjustments in regional trade rhythms. On the demand side, the recovery of domestic coal supply, cooling import demand, and a temporary weakening of global industrial and agricultural seaborne demand are the core reasons for the decline in freight rates. On the supply side, the slight recovery in shipping conditions earlier led to the resumption of some shipping capacity, resulting in a marginal easing of overall market capacity supply and further limiting the potential for freight rate increases.

Regarding future market trends, shipping industry analysts believe that the dry bulk shipping market will likely maintain a weak and volatile pattern in the short term. The pace of domestic coal production recovery, the progress of global manufacturing recovery, and the start of the peak season for grain exports in the Northern Hemisphere will be key factors influencing market movements. If global commodity trade demand steadily recovers, coupled with the arrival of the traditional peak shipping season, freight rates are expected to see a recovery; however, if demand remains weak, freight rates across the sector may continue to operate at low levels. Overall, the dry bulk shipping market has moved beyond its previous surge and entered a period of adjustment, with increased market uncertainty.

On June 22, 2026, the latest shipping market data showed that the Baltic Dry Index (BADI), a core indicator of international shipping trends, experienced a significant correction. All categories of dry bulk vessels, including large, medium, and small vessels, were under pressure, with both the index level and average daily freight rates declining, ending the previous partial market recovery. As a key indicator of global dry bulk shipping trade, the across-the-board decline in the BADI directly reflects the current industry situation of cooling global demand for bulk commodities and slight adjustments in the supply-demand pattern, sending an important signal for the dry bulk shipping market trend in the second half of the year.

Data shows that on June 22, the Baltic Dry Index (BDI), which tracks freight rates for the three major dry bulk carrier types—Capesize, Panamax, and Supramax—fell sharply by 38 points, a 1.4% overall decline, closing at 2684 points. The index showed a continued downward trend throughout the day, with no significant rebound. This decline was not a structural adjustment specific to a single vessel type, but rather a general downturn across the entire sector. The indices for all three major vessel types and their operating earnings all fell to varying degrees, completely reversing the previous recovery trend for some vessel types, and market sentiment became more cautious.

In the large dry bulk carrier sector, Capesize vessels remained the primary drag on the index, exhibiting the most significant market volatility. The Baltic Capesize index fell 75 points, or 1.8%, to close at 4074 points. Notably, this index had just reached its highest point since June 10th in the previous trading day, highlighting the instability of the large bulk carrier market. In terms of actual operating earnings, the average daily earnings for Capesize bulk carriers plummeted by $684 to $33,444 per day.

As large dry bulk carriers with a deadweight tonnage of 150,000 tons, Capesize vessels primarily undertake ocean-going transportation of bulk industrial raw materials such as iron ore, thermal coal, and coking coal. Their freight rate fluctuations are deeply tied to the global industrial supply chain and commodity prices. The recent sharp decline in profits is primarily due to changes in supply and demand in the Chinese coal market. Recently, domestic coking coal futures prices have continued to fall, market sentiment is weak, and the resumption of production in core coal-producing areas of Shanxi has accelerated, leading to rising market expectations for increased domestic coal supply and significantly weakening domestic demand for imported coking coal. Simultaneously, the previous period of concentrated coal import replenishment has ended, import growth has slowed, and ocean-going coal transportation orders have decreased significantly, directly resulting in a decline in demand for large bulk carrier capacity and consequently putting downward pressure on freight rates.

The medium-sized dry bulk carrier market also failed to maintain its recovery trend, with Panamax freight rates declining in tandem, matching the drop in rates for larger vessels. The Panamax index fell 37 points, or 1.8%, to close at 2059 points; corresponding to an average daily earnings per vessel decrease of $328, to $18,532 per day. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are the mainstay of global shipping of mid-range bulk commodities such as industrial coal, grain, and agricultural inputs. They are widely used on transatlantic and transpacific short-to-medium-haul ocean routes, boasting broad market coverage and strong demand representation.

The decline in freight rates for this vessel type is due to two main factors. First, it is influenced by the overall weakness in global industrial demand, with a slight decrease in the operating rate of overseas manufacturing and a contraction in demand for industrial coal transportation. Second, the global grain shipping market has entered a period of relative stability, with a slowdown in grain exports from major producing regions such as North and South America and Australia. This has resulted in insufficient growth in grain shipping orders, coupled with the redeployment of some idle shipping capacity after the previous market recovery, leading to a slight increase in market supply and a more relaxed supply-demand balance. Ultimately, this has driven a steady decline in Panamax vessel freight rates. Compared to larger vessel types, the decline in Panamax vessel rates is relatively moderate, but the overall downward trend confirms the overall cooling of demand in the dry bulk shipping market.

While the decline in the small dry bulk carrier market narrowed relatively, it continued its weak trend, with the downward trend spreading across the entire industry. The Supramax vessel index fell slightly by 3 points, or 0.2%, to close at 1715 points. Supramax vessels primarily handle short-haul, small-volume dry bulk cargo transportation, offering more flexible routes and adaptability to a wider range of cargoes. They are relatively less affected by fluctuations in the bulk raw material market, hence their decline was much smaller than that of medium and large-sized vessels. However, the decline in this vessel type index indicates that the current shipping market adjustment has covered all vessel classes, lacking a structural market trend, and the overall market sentiment continues to decline.

In summary, the overall weakening of the Baltic Dry Index is the result of a combination of factors, including short-term supply-demand mismatch, commodity market volatility, and adjustments in regional trade rhythms. On the demand side, the recovery of domestic coal supply, cooling import demand, and a temporary weakening of global industrial and agricultural seaborne demand are the core reasons for the decline in freight rates. On the supply side, the slight recovery in shipping conditions earlier led to the resumption of some shipping capacity, resulting in a marginal easing of overall market capacity supply and further limiting the potential for freight rate increases.

Regarding future market trends, shipping industry analysts believe that the dry bulk shipping market will likely maintain a weak and volatile pattern in the short term. The pace of domestic coal production recovery, the progress of global manufacturing recovery, and the start of the peak season for grain exports in the Northern Hemisphere will be key factors influencing market movements. If global commodity trade demand steadily recovers, coupled with the arrival of the traditional peak shipping season, freight rates are expected to see a recovery; however, if demand remains weak, freight rates across the sector may continue to operate at low levels. Overall, the dry bulk shipping market has moved beyond its previous surge and entered a period of adjustment, with increased market uncertainty.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.