A chart shows that shipping rates generally weakened, with the Baltic Dry Index declining slightly.

2026-06-23 22:34:42

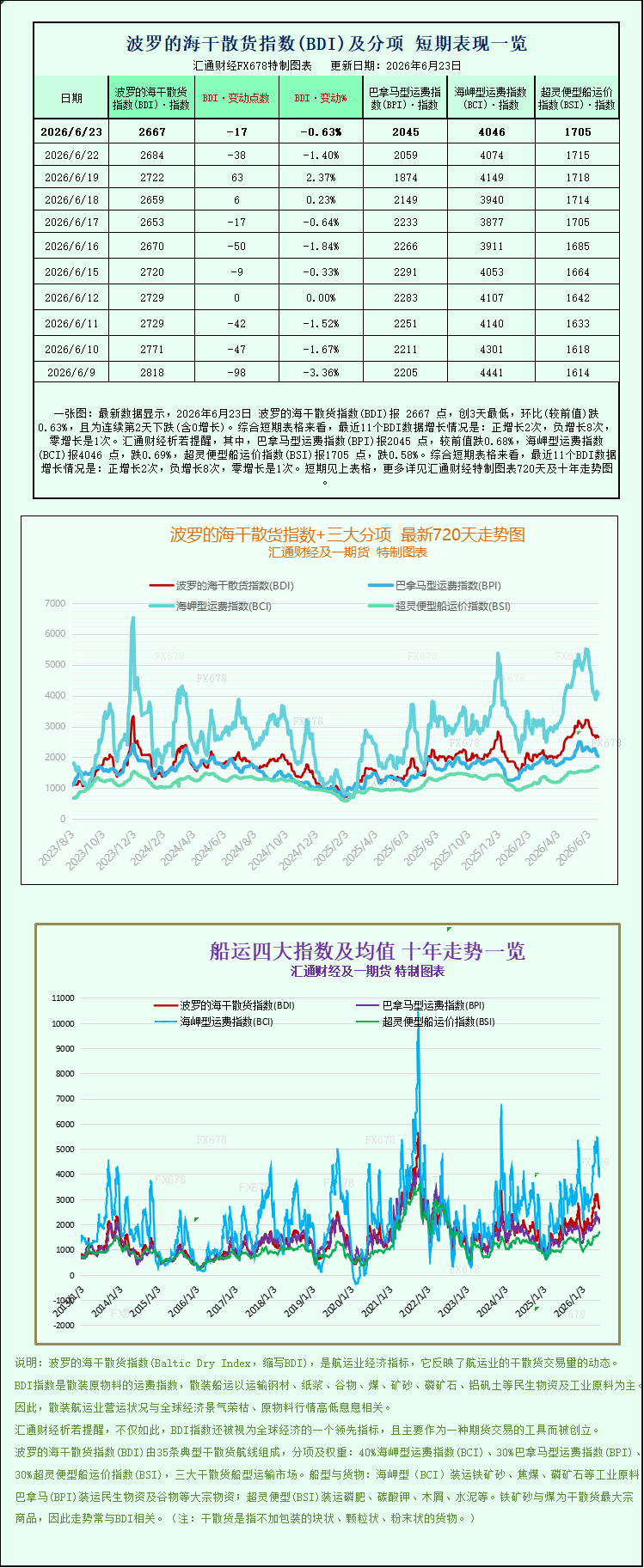

Latest data shows that on June 23, 2026, the Baltic Dry Index (BDI) was 2667 points, a three-day low, down 0.63% from the previous day, marking the second consecutive day of decline (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: positive growth twice, negative growth eight times, and zero growth once. Specifically, the Panamax Freight Index (BPI) was 2045 points, down 0.68% from the previous day; the Capesize Freight Index (BCI) was 4046 points, down 0.69%; and the Supramax Freight Index (BSI) was 1705 points, down 0.58%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

On June 23 local time, the Baltic Dry Index (BDI), a key indicator of the international shipping market, saw a slight decline. Dragged down by simultaneous drops in freight rates across all major vessel types, the BDI closed lower, reflecting weak short-term demand and relatively ample shipping capacity in the global dry bulk market, setting a weak tone for international commodity shipping trends at the end of the second quarter.

The Baltic Dry Index (BDI) is a core benchmark for the global dry bulk shipping market, primarily tracking ocean freight rates for bulk commodities such as iron ore, coal, grain, and mineral sands. It covers the operating profitability of large, medium, and small mainstream dry bulk vessels and is a crucial leading indicator for assessing global commodity trade activity, industrial production levels, and international trade and logistics trends, attracting significant attention from shipping companies, traders, and commodity investors. This recent decline in the index is not due to fluctuations in a single vessel type, but rather reflects a weakening market as a whole, with freight rates for all three major vessel types falling across the board, clearly indicating a downward trend in the market.

Data shows that the Baltic Dry Index (BDI), which reflects freight rates for the three main vessel types—Capesize, Panamax, and Supramax—fell by 17 points, or 0.6%, to close at 2667 points. The overall index trend was stable to slightly weak, ending the previous brief period of slight recovery. Looking at different vessel types, all sub-indices declined to varying degrees, with larger vessel freight rates experiencing a more significant drop, indicating a clear market divergence.

The Capesize index, representing very large dry bulk carriers, showed significant pressure on the day, falling 28 points, or 0.7%, to close at 4046 points, a new low since June 18th, highlighting a short-term weak trend. Capesize vessels are the core force in ocean-going dry bulk shipping, mainly carrying bulk cargoes of 150,000 tons or more, primarily industrial raw materials such as iron ore, thermal coal, and metallurgical coal. Their freight rates are highly correlated with global steel industry and industrial energy demand.

In terms of vessel operating earnings, the average daily earnings for Capesize vessels fell sharply by $252 to $33,192 on the day. Industry analysts pointed out that the core reason for the decline in earnings for this vessel type was the weak iron ore market. Approaching the end of the second quarter, major global iron ore suppliers increased their shipments, leading to a continuous rise in market supply, while demand showed a seasonal weakening trend. The steel industry in many parts of the world entered its seasonal off-season, with a decline in end-user steel consumption demand, reduced steel mill operating rates, and a cooling of iron ore purchasing intentions. This supply-demand mismatch caused iron ore prices to fall to their lowest level in months. The shrinking demand for raw materials directly dragged down the volume of shipping orders and freight rates for large ocean-going bulk carriers, becoming the core driver of the weakening Capesize vessel market.

The medium-sized vessel market also failed to escape the downward trend, with the Panamax index falling 14 points, or 0.7%, to 2045. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are the mainstay of global feeder shipping and regional commodity trade, primarily transporting bulk commodities such as thermal coal, grain, and fertilizer. They are widely used on transoceanic trade routes between Asia and Europe, and Asia and America, boasting broad market coverage and high trading activity. Earnings data shows that the average daily operating income for this vessel type decreased by $126 to $18,406, with profit margins continuing to narrow. The main reasons for the decline in Panamax freight rates are the stable but weak demand for grain transportation and insufficient increase in cross-regional coal transport.

The market for small dry bulk vessels also declined, with the Supramax index falling 10 points, or 0.6%, to close at 1705. Supramax vessels offer greater flexibility and are well-suited to the navigation conditions of small and medium-sized ports, primarily handling short-haul, small-volume dry bulk shipping orders, and are an important component of the regional shipping market. The decline in freight rates for this vessel type indicates an overall weakening of global demand for bulk commodity shipping in smaller and medium-sized areas, with the market weakness affecting all vessel types.

Based on a comprehensive analysis of current market trends, the recent decline in the Baltic Dry Index across the board is a result of the combined effects of short-term supply and demand fundamentals. On the demand side, the traditional peak season for industry in Europe and the United States is coming to an end, while the seasonal off-season for the steel industry is approaching, leading to a temporary contraction in global seaborne demand for industrial raw materials. On the supply side, relatively ample shipping capacity was deployed at the end of the second quarter, coupled with a cooling of market expectations due to concentrated shipments of bulk commodities, further suppressing the upside potential for freight rates.

Industry insiders indicate that in the short term, given weak seasonal demand and fluctuating raw material prices, the dry bulk shipping market is likely to maintain a weak and volatile pattern. Subsequent market trends will primarily depend on the recovery of global steel production capacity, the pace of the start of the peak season for grain transportation in the Northern Hemisphere, and the strength of the recovery in industrial energy demand in the Asia-Pacific region. These factors will be key drivers for stabilizing and rebounding freight rates.

On June 23 local time, the Baltic Dry Index (BDI), a key indicator of the international shipping market, saw a slight decline. Dragged down by simultaneous drops in freight rates across all major vessel types, the BDI closed lower, reflecting weak short-term demand and relatively ample shipping capacity in the global dry bulk market, setting a weak tone for international commodity shipping trends at the end of the second quarter.

The Baltic Dry Index (BDI) is a core benchmark for the global dry bulk shipping market, primarily tracking ocean freight rates for bulk commodities such as iron ore, coal, grain, and mineral sands. It covers the operating profitability of large, medium, and small mainstream dry bulk vessels and is a crucial leading indicator for assessing global commodity trade activity, industrial production levels, and international trade and logistics trends, attracting significant attention from shipping companies, traders, and commodity investors. This recent decline in the index is not due to fluctuations in a single vessel type, but rather reflects a weakening market as a whole, with freight rates for all three major vessel types falling across the board, clearly indicating a downward trend in the market.

Data shows that the Baltic Dry Index (BDI), which reflects freight rates for the three main vessel types—Capesize, Panamax, and Supramax—fell by 17 points, or 0.6%, to close at 2667 points. The overall index trend was stable to slightly weak, ending the previous brief period of slight recovery. Looking at different vessel types, all sub-indices declined to varying degrees, with larger vessel freight rates experiencing a more significant drop, indicating a clear market divergence.

The Capesize index, representing very large dry bulk carriers, showed significant pressure on the day, falling 28 points, or 0.7%, to close at 4046 points, a new low since June 18th, highlighting a short-term weak trend. Capesize vessels are the core force in ocean-going dry bulk shipping, mainly carrying bulk cargoes of 150,000 tons or more, primarily industrial raw materials such as iron ore, thermal coal, and metallurgical coal. Their freight rates are highly correlated with global steel industry and industrial energy demand.

In terms of vessel operating earnings, the average daily earnings for Capesize vessels fell sharply by $252 to $33,192 on the day. Industry analysts pointed out that the core reason for the decline in earnings for this vessel type was the weak iron ore market. Approaching the end of the second quarter, major global iron ore suppliers increased their shipments, leading to a continuous rise in market supply, while demand showed a seasonal weakening trend. The steel industry in many parts of the world entered its seasonal off-season, with a decline in end-user steel consumption demand, reduced steel mill operating rates, and a cooling of iron ore purchasing intentions. This supply-demand mismatch caused iron ore prices to fall to their lowest level in months. The shrinking demand for raw materials directly dragged down the volume of shipping orders and freight rates for large ocean-going bulk carriers, becoming the core driver of the weakening Capesize vessel market.

The medium-sized vessel market also failed to escape the downward trend, with the Panamax index falling 14 points, or 0.7%, to 2045. Panamax vessels, with a deadweight tonnage concentrated between 60,000 and 70,000 tons, are the mainstay of global feeder shipping and regional commodity trade, primarily transporting bulk commodities such as thermal coal, grain, and fertilizer. They are widely used on transoceanic trade routes between Asia and Europe, and Asia and America, boasting broad market coverage and high trading activity. Earnings data shows that the average daily operating income for this vessel type decreased by $126 to $18,406, with profit margins continuing to narrow. The main reasons for the decline in Panamax freight rates are the stable but weak demand for grain transportation and insufficient increase in cross-regional coal transport.

The market for small dry bulk vessels also declined, with the Supramax index falling 10 points, or 0.6%, to close at 1705. Supramax vessels offer greater flexibility and are well-suited to the navigation conditions of small and medium-sized ports, primarily handling short-haul, small-volume dry bulk shipping orders, and are an important component of the regional shipping market. The decline in freight rates for this vessel type indicates an overall weakening of global demand for bulk commodity shipping in smaller and medium-sized areas, with the market weakness affecting all vessel types.

Based on a comprehensive analysis of current market trends, the recent decline in the Baltic Dry Index across the board is a result of the combined effects of short-term supply and demand fundamentals. On the demand side, the traditional peak season for industry in Europe and the United States is coming to an end, while the seasonal off-season for the steel industry is approaching, leading to a temporary contraction in global seaborne demand for industrial raw materials. On the supply side, relatively ample shipping capacity was deployed at the end of the second quarter, coupled with a cooling of market expectations due to concentrated shipments of bulk commodities, further suppressing the upside potential for freight rates.

Industry insiders indicate that in the short term, given weak seasonal demand and fluctuating raw material prices, the dry bulk shipping market is likely to maintain a weak and volatile pattern. Subsequent market trends will primarily depend on the recovery of global steel production capacity, the pace of the start of the peak season for grain transportation in the Northern Hemisphere, and the strength of the recovery in industrial energy demand in the Asia-Pacific region. These factors will be key drivers for stabilizing and rebounding freight rates.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.