A major warning from the Eurozone PMI: proactive inventory reduction signals a slowdown in global demand.

2026-07-01 17:19:38

When assessing the long-term trends of international oil prices and commodities, geopolitical tensions often occupy the most prominent space in the media.

However, the underlying logic of the macroeconomy is never just about the "story" on the supply side, but also about the "reality" on the demand side.

Today's S&P Global Eurozone Manufacturing Purchasing Managers' Index (PMI) report for June has torn away the false prosperity of global trade and industrial demand, revealing the "invisible hand" that truly plays a decisive role behind the decline in international oil prices.

Literally speaking, the Eurozone manufacturing sector delivered a "barely satisfactory" performance in June, showing a weak recovery above the expansion/contraction threshold.

The composite index remained in expansion: the Eurozone manufacturing PMI came in at 51.4 in June, a slight decrease from 51.6 in May, but it has remained above the 50 mark for the fifth consecutive month.

The first half of the year ended successfully on the output side: the scale of manufacturing output achieved six consecutive months of month-on-month growth, and the overall performance in the second quarter reached the best level since the first quarter of 2022.

Price pressures eased marginally: both input cost inflation and output price inflation in the industry cooled down, falling to new lows in three months, and business confidence also rose to a four-month high.

However, behind these seemingly stable, or even slightly optimistic, figures, the variations in several key sub-indicators reveal a huge hole in the endogenous demand of the Eurozone and even the global economy.

If we break down this PMI report into its components, we will find that its "expansion" is extremely unhealthy.

From this, we can glean two critical signals regarding global demand: external demand is dragging down across the board, a zero-sum game of "domestic cold and even colder external cold," the decline of "preventative restocking," and global industry falling into proactive destocking. "This is the core micro-secret of this report."

The report clearly states: "External demand continues to be a drag, and the scale of export orders has declined for two consecutive months."

As a typical export-oriented economy, the continued contraction of new export orders in the Eurozone sends a dangerous signal—core foreign trade partners outside Europe (such as the United States, Asia and other major economies) are reducing their purchases of European manufactured goods.

The global trade pie is not getting bigger; on the contrary, it is getting smaller, and global industry is caught in a painful game of existing or even decreasing scale.

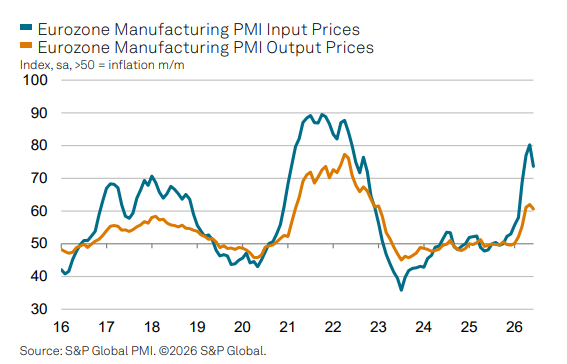

The decline in order volume, coupled with a significant increase in PMI costs as shown in the chart below, and limited increases in pricing, paints a picture of weak demand.

In the past few months, due to the tense situation in the Middle East and the high risk of supply chain disruptions, global companies, out of fear, carried out a large-scale "front-loading" – that is, placing orders to stockpile raw materials and semi-finished products regardless of whether they would need them at the moment.

This panic buying has artificially inflated global industrial demand over the past few months.

However, the data for June revealed the truth: "The purchase volume of raw materials and semi-finished products declined month-on-month in June, ending the growth trend of the previous three months... The scale of purchase inventory saw the largest drop since January this year."

With businesses ceasing to buy new products and geopolitical risks easing slightly, global buyers have become incredibly pragmatic, opting to rely on existing inventory to ensure production and mitigate supply chain disruptions.

This collective shift from "panic buying" to "aggressive destocking" reveals the true nature of the global industrial sector: end-user demand is extremely weak, and companies no longer have the confidence to continue expanding their procurement.

Chris Williamson, chief business economist at S&P Global Market Intelligence, commented, "The current cost pressures have eased favorably, with the core driver being the sharp decline in international oil prices this month..."

This forms a perfect logical loop. Many people attribute the recent drop in international oil prices solely to the marginal improvement in geopolitical relations.

However, they overlooked a deeper reason: the easing of geopolitical tensions was merely the "fuse" that triggered the squeeze on crude oil premiums, while the real "trump card" that overturned high oil prices was the substantial weakness in global industrial demand.

As the "lifeblood of industry," the long-term price trend of crude oil is ultimately determined by supply and demand fundamentals. The "collective braking of purchasing volume," "continued drag from external demand," and "the collapse of preventative restocking behavior" in the Eurozone PMI data in June all prove one thing—the marginal consumption of raw materials and energy by major industrial countries around the world is substantially slowing down.

Factories worldwide are tightening their belts to weather the winter by depleting their inventories, naturally leading to a temporary collapse in their purchasing power for commodities such as crude oil. Therefore, the decline in oil prices is not simply a political maneuver; it is an inevitable reflection of weak global industrial demand and the peak of the inventory cycle in the commodity market.

The global manufacturing sector, lacking visible demand, ultimately cannot support the visible high oil prices.

However, the underlying logic of the macroeconomy is never just about the "story" on the supply side, but also about the "reality" on the demand side.

Today's S&P Global Eurozone Manufacturing Purchasing Managers' Index (PMI) report for June has torn away the false prosperity of global trade and industrial demand, revealing the "invisible hand" that truly plays a decisive role behind the decline in international oil prices.

June Eurozone PMI: A Slowing Down Behind Moderate Expansion

Literally speaking, the Eurozone manufacturing sector delivered a "barely satisfactory" performance in June, showing a weak recovery above the expansion/contraction threshold.

The composite index remained in expansion: the Eurozone manufacturing PMI came in at 51.4 in June, a slight decrease from 51.6 in May, but it has remained above the 50 mark for the fifth consecutive month.

The first half of the year ended successfully on the output side: the scale of manufacturing output achieved six consecutive months of month-on-month growth, and the overall performance in the second quarter reached the best level since the first quarter of 2022.

Price pressures eased marginally: both input cost inflation and output price inflation in the industry cooled down, falling to new lows in three months, and business confidence also rose to a four-month high.

However, behind these seemingly stable, or even slightly optimistic, figures, the variations in several key sub-indicators reveal a huge hole in the endogenous demand of the Eurozone and even the global economy.

Key Insights: The situation is even colder both internally and externally; the "mask" of preventative inventory replenishment has been torn off.

If we break down this PMI report into its components, we will find that its "expansion" is extremely unhealthy.

From this, we can glean two critical signals regarding global demand: external demand is dragging down across the board, a zero-sum game of "domestic cold and even colder external cold," the decline of "preventative restocking," and global industry falling into proactive destocking. "This is the core micro-secret of this report."

The report clearly states: "External demand continues to be a drag, and the scale of export orders has declined for two consecutive months."

As a typical export-oriented economy, the continued contraction of new export orders in the Eurozone sends a dangerous signal—core foreign trade partners outside Europe (such as the United States, Asia and other major economies) are reducing their purchases of European manufactured goods.

The global trade pie is not getting bigger; on the contrary, it is getting smaller, and global industry is caught in a painful game of existing or even decreasing scale.

The decline in order volume, coupled with a significant increase in PMI costs as shown in the chart below, and limited increases in pricing, paints a picture of weak demand.

In the past few months, due to the tense situation in the Middle East and the high risk of supply chain disruptions, global companies, out of fear, carried out a large-scale "front-loading" – that is, placing orders to stockpile raw materials and semi-finished products regardless of whether they would need them at the moment.

This panic buying has artificially inflated global industrial demand over the past few months.

However, the data for June revealed the truth: "The purchase volume of raw materials and semi-finished products declined month-on-month in June, ending the growth trend of the previous three months... The scale of purchase inventory saw the largest drop since January this year."

With businesses ceasing to buy new products and geopolitical risks easing slightly, global buyers have become incredibly pragmatic, opting to rely on existing inventory to ensure production and mitigate supply chain disruptions.

This collective shift from "panic buying" to "aggressive destocking" reveals the true nature of the global industrial sector: end-user demand is extremely weak, and companies no longer have the confidence to continue expanding their procurement.

Conclusion: The real reason for high oil prices is the substantial collapse of global industrial demand.

Chris Williamson, chief business economist at S&P Global Market Intelligence, commented, "The current cost pressures have eased favorably, with the core driver being the sharp decline in international oil prices this month..."

This forms a perfect logical loop. Many people attribute the recent drop in international oil prices solely to the marginal improvement in geopolitical relations.

However, they overlooked a deeper reason: the easing of geopolitical tensions was merely the "fuse" that triggered the squeeze on crude oil premiums, while the real "trump card" that overturned high oil prices was the substantial weakness in global industrial demand.

As the "lifeblood of industry," the long-term price trend of crude oil is ultimately determined by supply and demand fundamentals. The "collective braking of purchasing volume," "continued drag from external demand," and "the collapse of preventative restocking behavior" in the Eurozone PMI data in June all prove one thing—the marginal consumption of raw materials and energy by major industrial countries around the world is substantially slowing down.

Factories worldwide are tightening their belts to weather the winter by depleting their inventories, naturally leading to a temporary collapse in their purchasing power for commodities such as crude oil. Therefore, the decline in oil prices is not simply a political maneuver; it is an inevitable reflection of weak global industrial demand and the peak of the inventory cycle in the commodity market.

The global manufacturing sector, lacking visible demand, ultimately cannot support the visible high oil prices.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.