The Bank of Japan's interest rate hike failed to save the yen, and the US June non-farm payroll data may trigger a shift in the currency market.

2026-07-02 09:38:57

The Bank of Japan's interest rate hikes failed to reverse the yen's depreciation trend, with the USD/JPY exchange rate continuing to hit multi-decade highs. The core reason lies in the huge policy interest rate differential between the US and Japan. Japanese officials have only issued verbal warnings and are unwilling to announce clear intervention thresholds. Even if they do intervene in the market, it can only provide short-term support for the yen and cannot change the long-term depreciation logic.

This Thursday's US non-farm payroll data will be a watershed moment for the market, while also defining key support and resistance levels for both bulls and bears. Before the interest rate differential narrows significantly, any pullbacks will present opportunities for bulls to enter the market.

Last month, the Bank of Japan raised its policy rate to 1%, the strongest monetary tightening measure in years. However, after the rate hike, the USD/JPY exchange rate continued to fluctuate and rise, stabilizing above the 162 mark and constantly hitting new highs in recent years.

The market trend is logically clear, primarily driven by the interest rate differential between the two countries. Even after the rate hikes, the policy rates of the Federal Reserve and the Bank of Japan will still differ by 275 basis points. Last month, the Fed maintained its high interest rates and released hawkish signals. Market arbitrage funds continue to borrow low-interest yen and buy high-yield dollar assets. As long as the interest rate differential remains high, the exchange rate rise will be driven by the yield differential, not by market sentiment towards the yen.

As the exchange rate continues to rise, Japanese finance officials have intensified their warnings, stating that they are closely monitoring exchange rate fluctuations and will not rule out any intervention measures.

The market generally believes that 160 is the implicit intervention range for the Japanese exchange rate. Historically, official intervention has occurred when the exchange rate touched this level, but regulators have consistently refused to disclose specific defensive levels. This ambiguity is interpreted by trading funds as a sign of hesitation, leading to continued upward pressure on the exchange rate and making it difficult to alleviate depreciation pressure.

Even if the Japanese Ministry of Finance directly intervenes in the market to buy yen, it can only quickly lower the exchange rate on a single day, and cannot fundamentally eliminate the US-Japan interest rate differential that is causing the yen to weaken.

Historical data shows that short-term declines caused by intervention only provide arbitrage traders with lower entry points for long positions, making it difficult to form a long-term trend reversal. In fact, short-term sharp drops are beneficial to short arbitrage positions that should have been suppressed.

Due to the adjustment of the US Independence Day holiday schedule, the non-farm payroll data, originally scheduled for release on Friday, will now be released at 20:30 Beijing time on Thursday.

The market expects non-farm payrolls to increase by 110,000, compared to 172,000 in the previous month, with the unemployment rate remaining at 4.3%. Earlier private sector employment data has already weakened. If the overall non-farm payroll data falls short of expectations, US Treasury yields and the dollar will decline in tandem, passively strengthening the yen. Conversely, strong data will reinforce interest rate differential expectations, accelerating the yen's depreciation and forcing Japan to implement control measures.

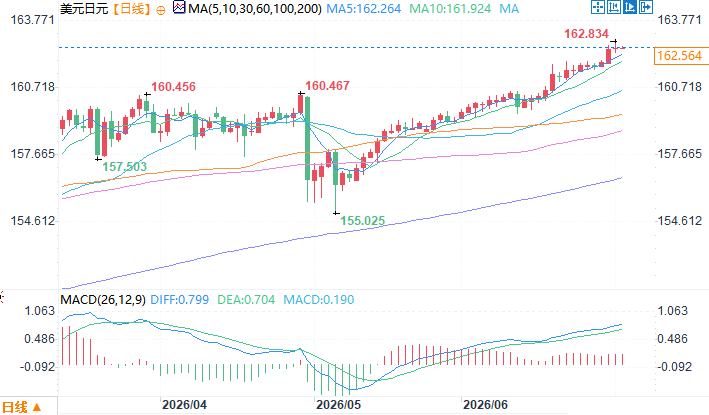

The primary short-term resistance is at the 163 level. Continued bullish momentum could target the 164 psychological level. The greater the upside potential within this range, the higher the probability of Japanese intervention. Key support lies at the 160 level, which coincides with the 50-day moving average. This level serves as both a psychological barrier and a potential intervention line. A decisive break below this level on the daily chart would reverse the bullish trend, with the next support level at 158.50.

The current stochastic oscillator is deeply overbought, but with ample interest rate differentials providing support, it's unlikely the overbought condition will reverse the trend. As long as the price holds above 160, the overall trend remains bullish. Only when intervention is implemented, the USD/JPY interest rate differential narrows substantially, or the closing price falls below 160 will the bullish/bearish logic reverse. Before that, every pullback presents an opportunity to buy.

Overall, a single round of interest rate hikes cannot offset the huge interest rate differential between the US and Japan, and the medium-term depreciation trend of the yen is unlikely to change. Verbal intervention by the Japanese side has limited effectiveness, and direct market intervention can only temporarily buffer the market.

The non-farm payroll data released Thursday evening is the biggest short-term variable, as its strength or weakness will directly impact the dollar's trajectory and expectations of intervention. As long as the 160 support level holds, the USD/JPY bullish trend remains intact, and all pullbacks present buying opportunities.

USD/JPY Daily Chart Source: EasyForex

At 9:38 AM Beijing time on July 2, the USD/JPY exchange rate was 162.55/56.

This Thursday's US non-farm payroll data will be a watershed moment for the market, while also defining key support and resistance levels for both bulls and bears. Before the interest rate differential narrows significantly, any pullbacks will present opportunities for bulls to enter the market.

Interest rate hikes are insufficient, and the continued high interest rate differential between the US and Japan is bullish for the US dollar.

Last month, the Bank of Japan raised its policy rate to 1%, the strongest monetary tightening measure in years. However, after the rate hike, the USD/JPY exchange rate continued to fluctuate and rise, stabilizing above the 162 mark and constantly hitting new highs in recent years.

The market trend is logically clear, primarily driven by the interest rate differential between the two countries. Even after the rate hikes, the policy rates of the Federal Reserve and the Bank of Japan will still differ by 275 basis points. Last month, the Fed maintained its high interest rates and released hawkish signals. Market arbitrage funds continue to borrow low-interest yen and buy high-yield dollar assets. As long as the interest rate differential remains high, the exchange rate rise will be driven by the yield differential, not by market sentiment towards the yen.

Japan's verbal pressure and ambiguous intervention have fueled bearish sentiment.

As the exchange rate continues to rise, Japanese finance officials have intensified their warnings, stating that they are closely monitoring exchange rate fluctuations and will not rule out any intervention measures.

The market generally believes that 160 is the implicit intervention range for the Japanese exchange rate. Historically, official intervention has occurred when the exchange rate touched this level, but regulators have consistently refused to disclose specific defensive levels. This ambiguity is interpreted by trading funds as a sign of hesitation, leading to continued upward pressure on the exchange rate and making it difficult to alleviate depreciation pressure.

Intervention in the foreign exchange market is a temporary solution that does not address the root cause; it can only create short-term buying opportunities.

Even if the Japanese Ministry of Finance directly intervenes in the market to buy yen, it can only quickly lower the exchange rate on a single day, and cannot fundamentally eliminate the US-Japan interest rate differential that is causing the yen to weaken.

Historical data shows that short-term declines caused by intervention only provide arbitrage traders with lower entry points for long positions, making it difficult to form a long-term trend reversal. In fact, short-term sharp drops are beneficial to short arbitrage positions that should have been suppressed.

Non-farm payroll data will be a crucial test, influencing subsequent interest rate spread expectations.

Due to the adjustment of the US Independence Day holiday schedule, the non-farm payroll data, originally scheduled for release on Friday, will now be released at 20:30 Beijing time on Thursday.

The market expects non-farm payrolls to increase by 110,000, compared to 172,000 in the previous month, with the unemployment rate remaining at 4.3%. Earlier private sector employment data has already weakened. If the overall non-farm payroll data falls short of expectations, US Treasury yields and the dollar will decline in tandem, passively strengthening the yen. Conversely, strong data will reinforce interest rate differential expectations, accelerating the yen's depreciation and forcing Japan to implement control measures.

Key price levels clearly define the bullish and bearish trends.

The primary short-term resistance is at the 163 level. Continued bullish momentum could target the 164 psychological level. The greater the upside potential within this range, the higher the probability of Japanese intervention. Key support lies at the 160 level, which coincides with the 50-day moving average. This level serves as both a psychological barrier and a potential intervention line. A decisive break below this level on the daily chart would reverse the bullish trend, with the next support level at 158.50.

The current stochastic oscillator is deeply overbought, but with ample interest rate differentials providing support, it's unlikely the overbought condition will reverse the trend. As long as the price holds above 160, the overall trend remains bullish. Only when intervention is implemented, the USD/JPY interest rate differential narrows substantially, or the closing price falls below 160 will the bullish/bearish logic reverse. Before that, every pullback presents an opportunity to buy.

Summarize

Overall, a single round of interest rate hikes cannot offset the huge interest rate differential between the US and Japan, and the medium-term depreciation trend of the yen is unlikely to change. Verbal intervention by the Japanese side has limited effectiveness, and direct market intervention can only temporarily buffer the market.

The non-farm payroll data released Thursday evening is the biggest short-term variable, as its strength or weakness will directly impact the dollar's trajectory and expectations of intervention. As long as the 160 support level holds, the USD/JPY bullish trend remains intact, and all pullbacks present buying opportunities.

USD/JPY Daily Chart Source: EasyForex

At 9:38 AM Beijing time on July 2, the USD/JPY exchange rate was 162.55/56.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.