World Gold Council: Gold prices are expected to remain range-bound in the second half of the year, or resume their upward trend, with limited downside potential.

2026-07-02 11:30:13

The World Gold Council released its mid-year outlook report, reviewing the dramatic price drop in the first half of the year, from nearly $5,600 to below $4,000. It predicts that gold will generally trade within a range in the second half of the year, with fluctuations of approximately 5%. Continued central bank gold purchases and long-term capital allocation provide bottom support, while geopolitical factors, changes in interest rate expectations, and policy adjustments in India will influence the direction of gold price breaksouts. The driving factors for bullish and bearish trends are clearly diverging, and the medium- to long-term investment value of precious metals has not disappeared.

The report's authors, Juan Carlos Artigas, Taylor Burnette, and Dr. Fergal O'Connor, stated that while gold prices have fallen by approximately 7% this year, this has been accompanied by extreme price fluctuations. During the escalating US-Iran conflict, gold volatility briefly exceeded 50%, but has since fallen below 30%, still above the 20-year average. Historical patterns show that volatility gradually returns to normal after periods of high levels.

Looking at intraday trading patterns, significant gold price fluctuations are concentrated during the Asian and US trading sessions, with pullbacks mostly occurring in the US session and rebounds frequently happening in the Asian session. This fully reflects the increasingly crucial role of Asian consumers and investors in the gold pricing system. Even after a deep correction, gold remains one of the top-performing asset classes over the past year.

According to the World Gold Council's self-developed valuation model, the current gold price reflects the current macroeconomic situation of moderate global growth, declining high inflation, and slight tightening by central banks. If there are no major variables, the gold price will fluctuate around $4,100 in the second half of the year, with a fluctuation of 5%.

The core catalysts for a bullish trend include three categories: economic downturn or escalating geopolitical risks, rising market expectations for interest rate cuts, and concentrated buying on dips. With multiple positive factors converging, gold prices are expected to return to $4,500, and strong signals could support a move towards the $5,000 mark.

Short-selling pressure stems from a stronger dollar, rising US Treasury yields, and increased market risk appetite. Even if gold prices fall 10% to 15% from current levels, bargain-hunting demand will limit further declines, and purely technical weakness is unlikely to lead to a sustained one-sided downtrend.

Since 2022, global central banks have averaged a net purchase of 1,000 tons of gold per year. In the first quarter of this year, some central banks temporarily reduced their holdings to replace gold, but still maintained net purchases throughout the year.

Association research indicates that more reserve managers plan to increase their gold holdings, but the number of central banks purchasing more gold does not necessarily represent a corresponding expansion in the scale of procurement. Calculations show that, based on the long-term average of 600 tons per year, an additional 20 to 30 tons of gold purchased by central banks would likely lead to a 1% increase in gold prices. The market confidence conveyed by gold purchases also has a boosting effect; if the pace of central bank gold purchases slows significantly, gold prices will face direct downward pressure.

India is the world's second-largest gold consumer market, with an average annual net demand of 800 tons, all of which is imported, continuously dragging down its current account.

The depreciation of the rupee, coupled with pressure on energy supply, has led India to raise its gold import tariff from 6% to 15%, and physical demand is expected to decrease by 50 to 60 tons this year. This negative factor has already been partially priced into gold prices. Further weakening of the domestic economy will dampen residents' willingness to buy gold, and increased defaults on gold-backed loans will further expand the physical supply, further suppressing prices.

In summary, gold prices fluctuated significantly in the first half of 2026, directly reflecting gold's high sensitivity to macroeconomic factors, geopolitical events, and market sentiment. In the second half of the year, barring extreme events, gold prices are expected to trade within a range, with central bank gold purchases providing solid support. However, if economic or geopolitical risks escalate or interest rate expectations shift, gold prices will have room to rise. Relying on its resilient demand across diverse sectors, gold remains an indispensable strategic asset for preserving value in a global environment of uncertainty.

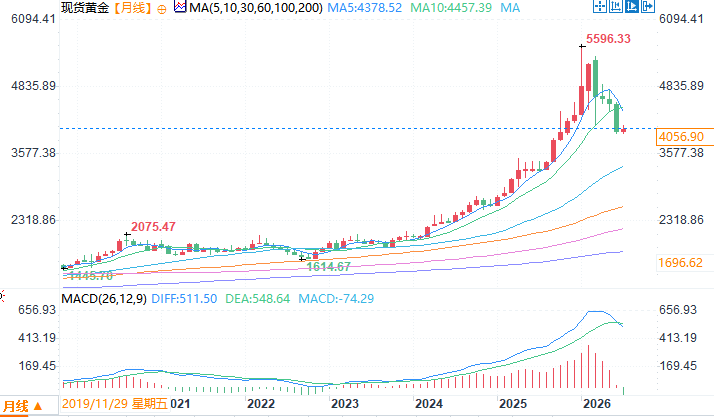

Spot gold monthly chart source: EasyForex

At 11:29 AM Beijing time on July 2nd, spot gold was trading at $4065.19 per ounce.

The market experienced significant volatility in the first half of the year, with a clear divergence between Asian and American trading sessions.

The report's authors, Juan Carlos Artigas, Taylor Burnette, and Dr. Fergal O'Connor, stated that while gold prices have fallen by approximately 7% this year, this has been accompanied by extreme price fluctuations. During the escalating US-Iran conflict, gold volatility briefly exceeded 50%, but has since fallen below 30%, still above the 20-year average. Historical patterns show that volatility gradually returns to normal after periods of high levels.

Looking at intraday trading patterns, significant gold price fluctuations are concentrated during the Asian and US trading sessions, with pullbacks mostly occurring in the US session and rebounds frequently happening in the Asian session. This fully reflects the increasingly crucial role of Asian consumers and investors in the gold pricing system. Even after a deep correction, gold remains one of the top-performing asset classes over the past year.

The benchmark market will fluctuate in the second half of the year, with bullish and bearish catalysts determining the direction of the breakout.

According to the World Gold Council's self-developed valuation model, the current gold price reflects the current macroeconomic situation of moderate global growth, declining high inflation, and slight tightening by central banks. If there are no major variables, the gold price will fluctuate around $4,100 in the second half of the year, with a fluctuation of 5%.

The core catalysts for a bullish trend include three categories: economic downturn or escalating geopolitical risks, rising market expectations for interest rate cuts, and concentrated buying on dips. With multiple positive factors converging, gold prices are expected to return to $4,500, and strong signals could support a move towards the $5,000 mark.

Short-selling pressure stems from a stronger dollar, rising US Treasury yields, and increased market risk appetite. Even if gold prices fall 10% to 15% from current levels, bargain-hunting demand will limit further declines, and purely technical weakness is unlikely to lead to a sustained one-sided downtrend.

Central bank gold purchases have formed a long-term support level, while the pace of these purchases disrupts short-term market movements.

Since 2022, global central banks have averaged a net purchase of 1,000 tons of gold per year. In the first quarter of this year, some central banks temporarily reduced their holdings to replace gold, but still maintained net purchases throughout the year.

Association research indicates that more reserve managers plan to increase their gold holdings, but the number of central banks purchasing more gold does not necessarily represent a corresponding expansion in the scale of procurement. Calculations show that, based on the long-term average of 600 tons per year, an additional 20 to 30 tons of gold purchased by central banks would likely lead to a 1% increase in gold prices. The market confidence conveyed by gold purchases also has a boosting effect; if the pace of central bank gold purchases slows significantly, gold prices will face direct downward pressure.

Changes in India's import policy have become a key variable of uncertainty.

India is the world's second-largest gold consumer market, with an average annual net demand of 800 tons, all of which is imported, continuously dragging down its current account.

The depreciation of the rupee, coupled with pressure on energy supply, has led India to raise its gold import tariff from 6% to 15%, and physical demand is expected to decrease by 50 to 60 tons this year. This negative factor has already been partially priced into gold prices. Further weakening of the domestic economy will dampen residents' willingness to buy gold, and increased defaults on gold-backed loans will further expand the physical supply, further suppressing prices.

Summarize

In summary, gold prices fluctuated significantly in the first half of 2026, directly reflecting gold's high sensitivity to macroeconomic factors, geopolitical events, and market sentiment. In the second half of the year, barring extreme events, gold prices are expected to trade within a range, with central bank gold purchases providing solid support. However, if economic or geopolitical risks escalate or interest rate expectations shift, gold prices will have room to rise. Relying on its resilient demand across diverse sectors, gold remains an indispensable strategic asset for preserving value in a global environment of uncertainty.

Spot gold monthly chart source: EasyForex

At 11:29 AM Beijing time on July 2nd, spot gold was trading at $4065.19 per ounce.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.