The US dollar weakened slightly ahead of the non-farm payrolls report, with weak ADP and PMI data coupled with increased policy uncertainty fueling a wait-and-see attitude in the market.

2026-07-02 13:35:53

The US dollar weakened throughout the Asian and early European sessions on Thursday, with the dollar index falling back to around 101.35 . Market sentiment was noticeably cautious ahead of the release of the US non-farm payroll data. As this data will directly influence the Federal Reserve's decision on the future path of interest rates, traders generally reduced directional bets, putting short-term pressure on the dollar.

The market's current focus is on the upcoming US June non-farm payrolls report. The market expects approximately 110,000 new jobs, significantly lower than May's 172,000, suggesting a possible marginal cooling in the labor market. Meanwhile, the unemployment rate is expected to remain unchanged at 4.3% , while average hourly earnings growth is projected to rise to 3.5% year-on-year, becoming an important indicator of inflation stickiness.

Recent high-frequency data releases have already foreshadowed some signs of weakness. US ADP employment growth was only 98,000, lower than the expected 113,000; the ISM Manufacturing PMI fell to 53.3, also below market expectations. These data reinforce the assessment of slowing economic momentum, leaving the US dollar lacking further upward momentum in the short term.

Despite marginally weakening economic data, the Federal Reserve maintains a tight policy stance. In a recent speech, Fed Chairman Kevin Warsh reiterated that current inflation levels remain too high and a firm return to the 2% target is essential, emphasizing the principles of monetary policy independence and data dependence. This overall hawkish stance provides some support for the dollar during its downward trend.

Market expectations for the interest rate path remain tight. Market surveys indicate that federal funds futures still imply an 85% probability that the Federal Reserve will at least maintain or even further tighten its policy, suggesting continued market vigilance regarding sticky inflation. However, divergent economic data is weakening this one-sided expectation, causing the dollar to enter a period of high-level fluctuation.

From a market structure perspective, the US dollar is currently in a data-driven consolidation phase with no clear directional trend. Employment data has become the key variable determining the short-term trend. If non-farm payrolls significantly miss expectations, it could suppress US Treasury yields and push the dollar down; conversely, it could strengthen interest rate expectations and support a renewed dollar rebound.

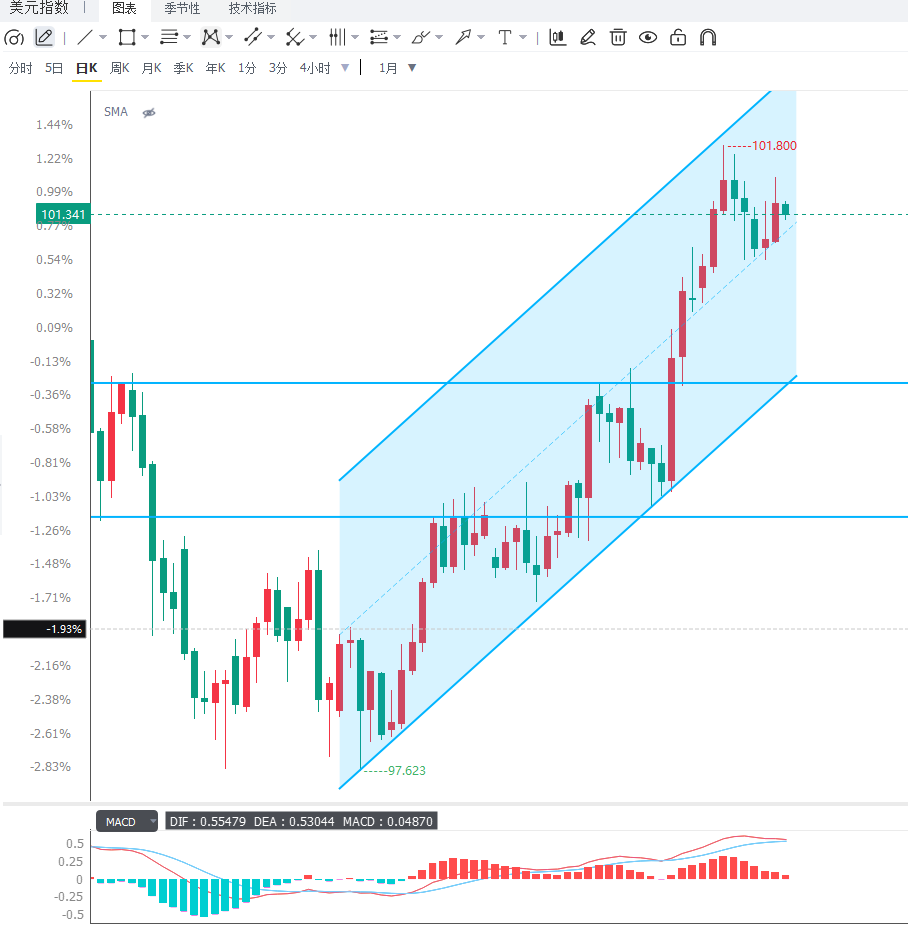

From a daily chart perspective, the US dollar index remains within a high-level consolidation range, with no clear trend reversal signal yet, but upward momentum is gradually slowing. Key resistance levels are currently located in the 101.80 and 102.30 area, while support is concentrated in the 100.80 and 100.20 area. A break below these levels could open up potential for a short-term pullback.

From a 4-hour chart perspective, the US dollar index is showing a mild downward trend in the short term, with the moving average system beginning to flatten, indicating weakening bullish momentum. The MACD histogram is converging, suggesting the market has entered a wait-and-see and consolidation phase, with fluctuations mainly revolving around data expectations. If the non-farm payroll data is weak, the index may test the 100.80 support area; if the data is strong, it may retest the resistance above 102.

Overall, the US dollar index remains in a consolidation phase at high levels, with no structural shift in the trend, but short-term momentum has clearly cooled. The market is repricing the Fed's interest rate path around the non-farm payroll data, exhibiting a clear event-driven characteristic. Before the data release, the dollar is expected to maintain range-bound trading, with increased volatility but an unclear trend direction. The medium-term trend still depends on the continued performance of employment and inflation data.

Editor's Summary:

Overall, the current trend of the US dollar presents a hedging pattern of "support from tighter policy + marginal weakening of economic data." While the Federal Reserve maintains a hawkish stance, high-frequency employment and manufacturing data are beginning to show signs of cooling, leading the market into a rebalancing phase before key data releases. In the short term, the US dollar lacks a unilateral driver, and non-farm payroll data will be the core variable determining the next stage of its trend. If the data is significantly weak, the US dollar may face a period of correction; if it performs steadily, it still has the foundation to maintain high-level fluctuations or even strengthen again.

The market's current focus is on the upcoming US June non-farm payrolls report. The market expects approximately 110,000 new jobs, significantly lower than May's 172,000, suggesting a possible marginal cooling in the labor market. Meanwhile, the unemployment rate is expected to remain unchanged at 4.3% , while average hourly earnings growth is projected to rise to 3.5% year-on-year, becoming an important indicator of inflation stickiness.

Recent high-frequency data releases have already foreshadowed some signs of weakness. US ADP employment growth was only 98,000, lower than the expected 113,000; the ISM Manufacturing PMI fell to 53.3, also below market expectations. These data reinforce the assessment of slowing economic momentum, leaving the US dollar lacking further upward momentum in the short term.

Despite marginally weakening economic data, the Federal Reserve maintains a tight policy stance. In a recent speech, Fed Chairman Kevin Warsh reiterated that current inflation levels remain too high and a firm return to the 2% target is essential, emphasizing the principles of monetary policy independence and data dependence. This overall hawkish stance provides some support for the dollar during its downward trend.

Market expectations for the interest rate path remain tight. Market surveys indicate that federal funds futures still imply an 85% probability that the Federal Reserve will at least maintain or even further tighten its policy, suggesting continued market vigilance regarding sticky inflation. However, divergent economic data is weakening this one-sided expectation, causing the dollar to enter a period of high-level fluctuation.

From a market structure perspective, the US dollar is currently in a data-driven consolidation phase with no clear directional trend. Employment data has become the key variable determining the short-term trend. If non-farm payrolls significantly miss expectations, it could suppress US Treasury yields and push the dollar down; conversely, it could strengthen interest rate expectations and support a renewed dollar rebound.

From a daily chart perspective, the US dollar index remains within a high-level consolidation range, with no clear trend reversal signal yet, but upward momentum is gradually slowing. Key resistance levels are currently located in the 101.80 and 102.30 area, while support is concentrated in the 100.80 and 100.20 area. A break below these levels could open up potential for a short-term pullback.

From a 4-hour chart perspective, the US dollar index is showing a mild downward trend in the short term, with the moving average system beginning to flatten, indicating weakening bullish momentum. The MACD histogram is converging, suggesting the market has entered a wait-and-see and consolidation phase, with fluctuations mainly revolving around data expectations. If the non-farm payroll data is weak, the index may test the 100.80 support area; if the data is strong, it may retest the resistance above 102.

Overall, the US dollar index remains in a consolidation phase at high levels, with no structural shift in the trend, but short-term momentum has clearly cooled. The market is repricing the Fed's interest rate path around the non-farm payroll data, exhibiting a clear event-driven characteristic. Before the data release, the dollar is expected to maintain range-bound trading, with increased volatility but an unclear trend direction. The medium-term trend still depends on the continued performance of employment and inflation data.

Editor's Summary:

Overall, the current trend of the US dollar presents a hedging pattern of "support from tighter policy + marginal weakening of economic data." While the Federal Reserve maintains a hawkish stance, high-frequency employment and manufacturing data are beginning to show signs of cooling, leading the market into a rebalancing phase before key data releases. In the short term, the US dollar lacks a unilateral driver, and non-farm payroll data will be the core variable determining the next stage of its trend. If the data is significantly weak, the US dollar may face a period of correction; if it performs steadily, it still has the foundation to maintain high-level fluctuations or even strengthen again.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.