A chart: The Baltic Dry Index rises to a two-week high, boosted by Cape of Good Hope shipping rates.

2026-07-04 00:13:49

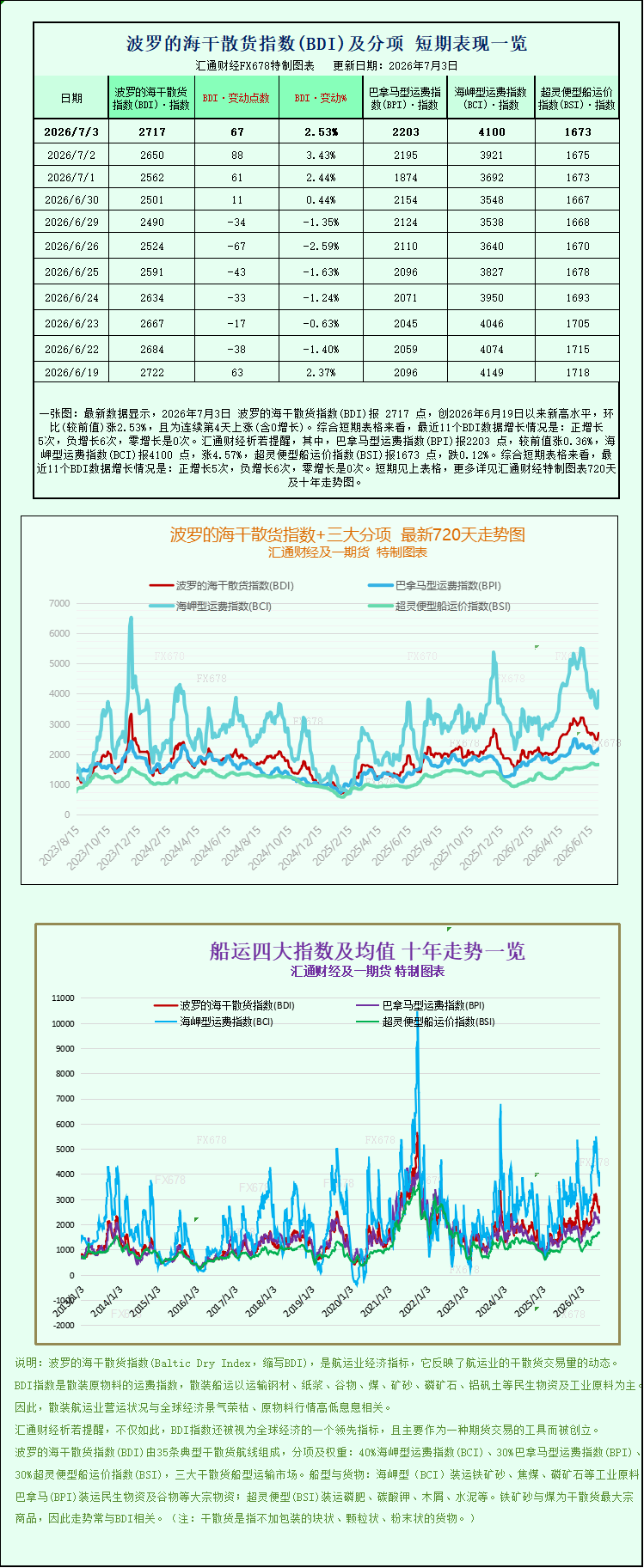

Latest data shows that the Baltic Dry Index (BDI) reached 2717 points on July 3, 2026, a new high since June 19, 2026, up 2.53% month-on-month, marking the fourth consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 5 positive increases, 6 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2203 points, up 0.36% from the previous value; the Capesize Freight Index (BCI) was 4100 points, up 4.57%; and the Supramax Freight Index (BSI) was 1673 points, down 0.12%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index, which tracks charter rates for dry bulk shipping vessels, hit a two-week high on Friday, driven by stronger Capesize vessel rates.

The Baltic Dry Index (BDI) combines freight rates for three major vessel types: Capesize, Panamax, and Supramax. It rose 67 points, or 2.5%, to close at 2,717 points, the highest level since June 19, with a cumulative weekly increase of 7.6%.

In terms of specific ship type indices, the Capesize freight rate index rose 179 points, or 4.6%, to 4,100 points, a weekly increase of 12%, reaching its highest level since mid-April.

The Cape-class vessel has a deadweight tonnage of approximately 150,000 tons and mainly transports raw materials such as iron ore and coal. The average daily earnings per unit of this vessel type rose by $1,618 to $33,678.

The Panamax freight index rose 8 points, or 0.4%, to close at 2203 points, marking a weekly increase of over 4% and the second consecutive week of rising freight rates.

Panamax vessels, with a deadweight tonnage of 60,000 to 70,000 tons, primarily transport coal and grain, resulting in an average daily revenue increase of $67 to $19,825.

In the small vessel sector, the full details of the Supramax freight rate index were not disclosed in the original text.

The Baltic Dry Index (BDI) is a core leading indicator for global commodity shipping. Compiled and published daily by the Baltic Exchange in London, it directly reflects the ocean shipping demand of global steel mills, power plants, and grain and oil traders. It is widely used by shipbuilders, traders, and investment institutions as a basis for judging the health of the real economy. The index is weighted by freight rates for three types of vessels, with the Cape-class vessels, which have the largest deadweight and primarily transport minerals, having the strongest impact on index fluctuations. The recent rebound in the index was driven by this vessel type.

The Baltic Dry Index (BDI) stabilized above 2717 points this Friday, ending nearly two weeks of low-level fluctuations. A 2.5% increase on a single day and a 7.6% increase on a weekly basis signifies that the dry bulk market has fully recovered from the June off-season slump. The market remained under pressure in mid-to-late June, partly due to phased production cuts by Asian steel mills and a slowdown in raw material restocking, leading to weakened demand for mineral shipping; and partly due to a large number of new ship deliveries, resulting in ample market capacity and continuously depressing charter rates. Entering July, the supply-demand relationship reversed rapidly, driving a strong recovery in the index.

The biggest highlight of this round of market activity came from the Capesize shipping market. Its sub-index surged 12% in a single week, returning to 4100 points and reaching a near three-month high. Daily shipowner profits increased by over $1600, steadily exceeding $33,000. The core routes for Capesize vessels are concentrated on iron ore exports from Australia and Brazil to East Asia, with freight rates directly tied to the steel industry chain. This strength is driven by three core factors: First, Asian steel mills have completed maintenance and production cuts, focusing on summer iron ore stockpiling, leading to a continuous increase in shipments from Australian and Brazilian mining companies and a surge in short-term charter orders. Second, some vessels were temporarily diverted to the Atlantic to transport coal, tightening available capacity on major Pacific routes and creating a short-term structural gap. Third, early stockpiling of heating coal in the Northern Hemisphere and increased imports of thermal coal by Asian and European power plants have combined demand for both ore and coal, significantly boosting shipowners' bargaining power. For shipping companies, the increase in daily charter rates directly boosted operating profits, with leading dry bulk shipping companies seeing weekly revenue per vessel increase by over $10,000, demonstrating a significant improvement in fundamentals.

In contrast to the surge in Capesize freight rates, Panamax freight rates have shown a more moderate and stable trend. While only slightly increasing by 0.4% on the day, it marked the second consecutive week of gains, with a weekly increase exceeding 4%, and daily earnings remaining stable at nearly $20,000. Panamax vessels, with a deadweight tonnage of 60,000-70,000 tons, carry global grain trade such as wheat, corn, and soybeans, while also transporting coal to small and medium-sized power plants. Demand is diversified and less volatile. The core driver currently supporting its freight rates is the peak season for global grain exports: increased shipments of North American corn and soybeans, continued shipments of South American soybeans and wheat, and stable demand from grain-importing countries in the Middle East and North Africa. Grain trade has inelastic characteristics; even if industrial raw material demand fluctuates in the short term, the demand for agricultural product transportation provides solid support for Panamax freight rates, which is key to the continued slow and steady rise in this vessel type.

The divergence in price trends across large and small vessels clearly reflects the current differences in the global commodity trade structure: a surge in demand for industrial minerals has driven up the prices of large mining vessels, while the rigid demand for grain has provided a stable upward trend for medium-sized vessels; smaller Supramax vessels, mainly responsible for short-distance bulk cargo, fertilizer, sand and gravel, and small-scale grain transportation, have ample market supply, and their prices typically lag behind the broader market, only experiencing slight increases in the short term, unlikely to see significant surges. The overall market has formed a tiered pattern of "large vessels leading the rise, medium-sized vessels steadily rising, and small vessels following suit," with bullish sentiment spreading across the board.

The continued rise in the Baltic Dry Index (BDI) has multiple market transmission effects. First, it benefits listed dry bulk shipping companies, as higher charter rates directly increase their revenue and profits, driving a recovery in the valuation of the shipping sector in the secondary market. Second, rising shipping costs will be transmitted to the landed prices of bulk commodities, slightly increasing the import costs for steel mills and grain and oil companies. Third, the index's recovery releases positive macroeconomic signals, indicating a recovery in Asian manufacturing activity, increased activity in global infrastructure and agricultural trade, and the real economy shaking off the pressure of the off-season.

Meanwhile, the market still faces upward constraints. In the medium to long term, a large number of newly built dry bulk vessels will continue to be delivered, and the expansion of shipping capacity will gradually alleviate the current short-term shortage of vessels and excess cargo, limiting the long-term upside potential for freight rates. Short-term risks are concentrated on the pace of steel mill procurement; if iron ore restocking slows down, Cape-of-Good freight rates are highly likely to experience a rapid correction. Furthermore, changes in global energy policies and geopolitical trade will also disrupt the import and export rhythms of coal and minerals, altering the supply and demand balance along shipping routes.

Looking ahead to the short-term market, the optimism generated by this week's strong gains will continue to build, coupled with the approaching peak season for raw material stockpiling in the third quarter, the dry bulk index is likely to remain at a high level. Capesize vessels still have some room for further upward movement, Panamax vessels will maintain a steady upward trend with fluctuations, and smaller vessels will moderately follow the market's recovery.

The data released this time shows that the current rebound in the Baltic Dry Index (BDI) is the result of multiple factors, including concentrated restocking of mineral resources, essential global food trade demand, and a short-term shipping capacity shortage. The divergence in market conditions for vessels of different tonnages directly reflects the disparity in activity between industrial raw materials and agricultural products, providing important reference for shipping professionals and commodity investors to assess global trade trends. As a leading indicator of the real economy, the recent rise in the BDI also suggests a continued recovery in the activity of global commodity circulation.

The Baltic Dry Index, which tracks charter rates for dry bulk shipping vessels, hit a two-week high on Friday, driven by stronger Capesize vessel rates.

The Baltic Dry Index (BDI) combines freight rates for three major vessel types: Capesize, Panamax, and Supramax. It rose 67 points, or 2.5%, to close at 2,717 points, the highest level since June 19, with a cumulative weekly increase of 7.6%.

In terms of specific ship type indices, the Capesize freight rate index rose 179 points, or 4.6%, to 4,100 points, a weekly increase of 12%, reaching its highest level since mid-April.

The Cape-class vessel has a deadweight tonnage of approximately 150,000 tons and mainly transports raw materials such as iron ore and coal. The average daily earnings per unit of this vessel type rose by $1,618 to $33,678.

The Panamax freight index rose 8 points, or 0.4%, to close at 2203 points, marking a weekly increase of over 4% and the second consecutive week of rising freight rates.

Panamax vessels, with a deadweight tonnage of 60,000 to 70,000 tons, primarily transport coal and grain, resulting in an average daily revenue increase of $67 to $19,825.

In the small vessel sector, the full details of the Supramax freight rate index were not disclosed in the original text.

The Baltic Dry Index (BDI) is a core leading indicator for global commodity shipping. Compiled and published daily by the Baltic Exchange in London, it directly reflects the ocean shipping demand of global steel mills, power plants, and grain and oil traders. It is widely used by shipbuilders, traders, and investment institutions as a basis for judging the health of the real economy. The index is weighted by freight rates for three types of vessels, with the Cape-class vessels, which have the largest deadweight and primarily transport minerals, having the strongest impact on index fluctuations. The recent rebound in the index was driven by this vessel type.

The Baltic Dry Index (BDI) stabilized above 2717 points this Friday, ending nearly two weeks of low-level fluctuations. A 2.5% increase on a single day and a 7.6% increase on a weekly basis signifies that the dry bulk market has fully recovered from the June off-season slump. The market remained under pressure in mid-to-late June, partly due to phased production cuts by Asian steel mills and a slowdown in raw material restocking, leading to weakened demand for mineral shipping; and partly due to a large number of new ship deliveries, resulting in ample market capacity and continuously depressing charter rates. Entering July, the supply-demand relationship reversed rapidly, driving a strong recovery in the index.

The biggest highlight of this round of market activity came from the Capesize shipping market. Its sub-index surged 12% in a single week, returning to 4100 points and reaching a near three-month high. Daily shipowner profits increased by over $1600, steadily exceeding $33,000. The core routes for Capesize vessels are concentrated on iron ore exports from Australia and Brazil to East Asia, with freight rates directly tied to the steel industry chain. This strength is driven by three core factors: First, Asian steel mills have completed maintenance and production cuts, focusing on summer iron ore stockpiling, leading to a continuous increase in shipments from Australian and Brazilian mining companies and a surge in short-term charter orders. Second, some vessels were temporarily diverted to the Atlantic to transport coal, tightening available capacity on major Pacific routes and creating a short-term structural gap. Third, early stockpiling of heating coal in the Northern Hemisphere and increased imports of thermal coal by Asian and European power plants have combined demand for both ore and coal, significantly boosting shipowners' bargaining power. For shipping companies, the increase in daily charter rates directly boosted operating profits, with leading dry bulk shipping companies seeing weekly revenue per vessel increase by over $10,000, demonstrating a significant improvement in fundamentals.

In contrast to the surge in Capesize freight rates, Panamax freight rates have shown a more moderate and stable trend. While only slightly increasing by 0.4% on the day, it marked the second consecutive week of gains, with a weekly increase exceeding 4%, and daily earnings remaining stable at nearly $20,000. Panamax vessels, with a deadweight tonnage of 60,000-70,000 tons, carry global grain trade such as wheat, corn, and soybeans, while also transporting coal to small and medium-sized power plants. Demand is diversified and less volatile. The core driver currently supporting its freight rates is the peak season for global grain exports: increased shipments of North American corn and soybeans, continued shipments of South American soybeans and wheat, and stable demand from grain-importing countries in the Middle East and North Africa. Grain trade has inelastic characteristics; even if industrial raw material demand fluctuates in the short term, the demand for agricultural product transportation provides solid support for Panamax freight rates, which is key to the continued slow and steady rise in this vessel type.

The divergence in price trends across large and small vessels clearly reflects the current differences in the global commodity trade structure: a surge in demand for industrial minerals has driven up the prices of large mining vessels, while the rigid demand for grain has provided a stable upward trend for medium-sized vessels; smaller Supramax vessels, mainly responsible for short-distance bulk cargo, fertilizer, sand and gravel, and small-scale grain transportation, have ample market supply, and their prices typically lag behind the broader market, only experiencing slight increases in the short term, unlikely to see significant surges. The overall market has formed a tiered pattern of "large vessels leading the rise, medium-sized vessels steadily rising, and small vessels following suit," with bullish sentiment spreading across the board.

The continued rise in the Baltic Dry Index (BDI) has multiple market transmission effects. First, it benefits listed dry bulk shipping companies, as higher charter rates directly increase their revenue and profits, driving a recovery in the valuation of the shipping sector in the secondary market. Second, rising shipping costs will be transmitted to the landed prices of bulk commodities, slightly increasing the import costs for steel mills and grain and oil companies. Third, the index's recovery releases positive macroeconomic signals, indicating a recovery in Asian manufacturing activity, increased activity in global infrastructure and agricultural trade, and the real economy shaking off the pressure of the off-season.

Meanwhile, the market still faces upward constraints. In the medium to long term, a large number of newly built dry bulk vessels will continue to be delivered, and the expansion of shipping capacity will gradually alleviate the current short-term shortage of vessels and excess cargo, limiting the long-term upside potential for freight rates. Short-term risks are concentrated on the pace of steel mill procurement; if iron ore restocking slows down, Cape-of-Good freight rates are highly likely to experience a rapid correction. Furthermore, changes in global energy policies and geopolitical trade will also disrupt the import and export rhythms of coal and minerals, altering the supply and demand balance along shipping routes.

Looking ahead to the short-term market, the optimism generated by this week's strong gains will continue to build, coupled with the approaching peak season for raw material stockpiling in the third quarter, the dry bulk index is likely to remain at a high level. Capesize vessels still have some room for further upward movement, Panamax vessels will maintain a steady upward trend with fluctuations, and smaller vessels will moderately follow the market's recovery.

The data released this time shows that the current rebound in the Baltic Dry Index (BDI) is the result of multiple factors, including concentrated restocking of mineral resources, essential global food trade demand, and a short-term shipping capacity shortage. The divergence in market conditions for vessels of different tonnages directly reflects the disparity in activity between industrial raw materials and agricultural products, providing important reference for shipping professionals and commodity investors to assess global trade trends. As a leading indicator of the real economy, the recent rise in the BDI also suggests a continued recovery in the activity of global commodity circulation.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.