A chart shows the Baltic Dry Index climbing to a more than one-month high, indicating a divergent upward trend in the dry bulk shipping market.

2026-07-14 01:08:10

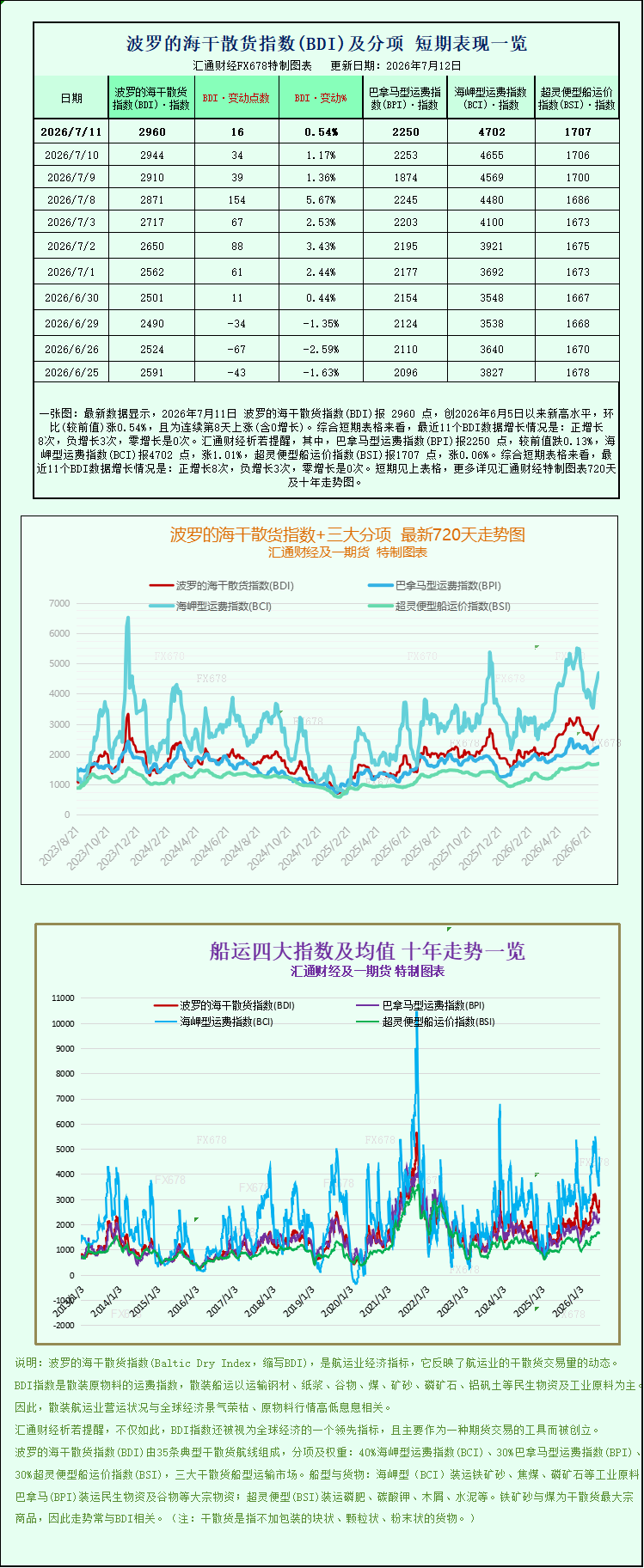

The latest data shows that the Baltic Dry Index (BDI) reached 2960 points on July 11, 2026, a new high since June 5, 2026, up 0.54% month-on-month, marking the 8th consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 8 positive increases, 3 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 2250 points, down 0.13% from the previous value; the Capesize Freight Index (BCI) was 4702 points, up 1.01%; and the Supramax Freight Index (BSI) was 1707 points, up 0.06%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three sub-indices, please refer to the charts specially created by FX678.  On July 13, 2026, the latest shipping market data showed that the Baltic Dry Index (BADI), a key indicator of international dry bulk shipping, steadily rose, reaching a new high in over a month since early June, marking a phase of recovery in the global dry bulk shipping market. This rise was not a general increase across all categories, but rather exhibited significant structural differentiation. Strong increases in freight rates for large Capesize and small-to-medium-sized Supramax vessels offset the slight decline in Panamax vessels, driving the overall market index higher and reflecting the differentiated changes in the current global supply and demand pattern for bulk commodities. Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk vessel types (Capesize, Panamax, and Supramax), rose 16 points, or 0.5%, to close at 2960 points, the highest closing level since early June, completely shaking off the previous volatile and sluggish trend. Looking at the data by vessel type, the core driver of this index rise was the strong rebound of Capesize vessels. As the mainstay of the dry bulk market, this vessel type has the greatest impact on the overall index weight. On that day, the Baltic Capesize Index surged 47 points, a gain exceeding 1%, closing at 4702 points, also reaching a high in over a month, becoming the core force driving the market upward. In terms of actual operating revenue, the profitability of Capesize vessels also rose. Data shows that Capesize vessels with a deadweight tonnage of 150,000 tons, primarily transporting bulk industrial raw materials such as iron ore and coal, saw their average daily revenue increase by $427 to $39,138 per day, with a steady recovery in per-vessel operating revenue, significantly boosting market confidence among large bulk carrier owners. Industry analysts point out that the recovery in Capesize freight rates stems primarily from the adjustment of the global bulk dry bulk shipping structure. Although upstream commodity prices fluctuate, the contraction in shipping supply has provided solid support for freight rates. From a fundamental perspective, the current iron ore shipping market exhibits a clear bullish-bearish tug-of-war pattern, which has become the core factor influencing Capesize freight rate fluctuations. On the one hand, recent international iron ore futures prices have continued to weaken, exacerbating operating pressures in the domestic steel industry. Steel mill losses have continued to widen, and expectations of industry production cuts and restrictions have intensified, directly suppressing iron ore procurement demand and price increases, thus bringing certain negative pressure to the upstream shipping market. On the other hand, shipments from major global iron ore exporting countries have declined in stages, resulting in a relatively tight supply of large vessels available in the shipping market. This supply-demand mismatch has effectively offset the weak demand, ultimately supporting a counter-trend rise in Capesize freight rates and driving the sub-index higher. In stark contrast to the strong performance of Capesize vessels, the medium-sized Panamax vessel market showed a slight pullback, becoming the only drag on the market that day. Data shows that the Panamax vessel index fell slightly by 3 points, a decrease of 0.1%, closing at 2250 points, with an overall relatively stable trend. Correspondingly, vessel operating revenues saw slight adjustments. Panamax vessels, primarily engaged in the transportation of coal, grain, and other commodities in the 60,000 to 70,000 tonne class, saw their average daily revenue fall to the $19,254 range, resulting in a slight contraction in profitability. It is understood that Panamax vessels mainly serve the global cross-regional transportation of energy coal and grain. Recently, global coal trade demand has been stable, and the increase in grain shipping orders has been insufficient. Coupled with relatively ample short-term capacity deployment for this vessel type, the market supply and demand have been relaxed, ultimately leading to a slight decline in freight rates. The small vessel sector continued its moderate recovery, providing auxiliary support for the overall index's upward movement. The Supramax vessel index rose slightly by 1 point, or 0.1%, closing at 1707 points, marking a continuous slight upward trend. Supramax vessels are highly flexible and adaptable to a wide range of cargo types, mainly undertaking small-batch, multi-category dry bulk cargo transportation orders, covering building materials, niche minerals, and miscellaneous grains. Recent increases in global regional trade activity, with a continued rise in short-haul and fractional shipping orders in Southeast Asia, the Middle East, and Latin America, have driven a steady recovery in freight rates for smaller vessels. Although the increase is limited, it has solidified the foundation for the overall recovery of the dry bulk market. From an industry perspective, the current rise in the Baltic Dry Index directly reflects the rebalancing of supply and demand in the global dry bulk shipping market, highlighting structural differentiation. Large vessels benefit from the contraction in shipments of major mineral commodities and continued capacity constraints, while smaller vessels are steadily recovering due to the recovery in regional trade. Medium-sized vessels, however, are weaker due to lackluster demand for energy and food. In the short term, uncertainty regarding iron ore demand will persist. Changes in domestic steel mill production schedules and global commodity shipments will be key variables in the future trend of Capesize vessel freight rates. Meanwhile, with the global peak trade season approaching, dry bulk shipping demand is expected to continue to rise. If capacity supply remains tight, the Baltic Dry Index is likely to continue its upward trend, and the overall profitability of the industry is expected to continue to improve.

On July 13, 2026, the latest shipping market data showed that the Baltic Dry Index (BADI), a key indicator of international dry bulk shipping, steadily rose, reaching a new high in over a month since early June, marking a phase of recovery in the global dry bulk shipping market. This rise was not a general increase across all categories, but rather exhibited significant structural differentiation. Strong increases in freight rates for large Capesize and small-to-medium-sized Supramax vessels offset the slight decline in Panamax vessels, driving the overall market index higher and reflecting the differentiated changes in the current global supply and demand pattern for bulk commodities. Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk vessel types (Capesize, Panamax, and Supramax), rose 16 points, or 0.5%, to close at 2960 points, the highest closing level since early June, completely shaking off the previous volatile and sluggish trend. Looking at the data by vessel type, the core driver of this index rise was the strong rebound of Capesize vessels. As the mainstay of the dry bulk market, this vessel type has the greatest impact on the overall index weight. On that day, the Baltic Capesize Index surged 47 points, a gain exceeding 1%, closing at 4702 points, also reaching a high in over a month, becoming the core force driving the market upward. In terms of actual operating revenue, the profitability of Capesize vessels also rose. Data shows that Capesize vessels with a deadweight tonnage of 150,000 tons, primarily transporting bulk industrial raw materials such as iron ore and coal, saw their average daily revenue increase by $427 to $39,138 per day, with a steady recovery in per-vessel operating revenue, significantly boosting market confidence among large bulk carrier owners. Industry analysts point out that the recovery in Capesize freight rates stems primarily from the adjustment of the global bulk dry bulk shipping structure. Although upstream commodity prices fluctuate, the contraction in shipping supply has provided solid support for freight rates. From a fundamental perspective, the current iron ore shipping market exhibits a clear bullish-bearish tug-of-war pattern, which has become the core factor influencing Capesize freight rate fluctuations. On the one hand, recent international iron ore futures prices have continued to weaken, exacerbating operating pressures in the domestic steel industry. Steel mill losses have continued to widen, and expectations of industry production cuts and restrictions have intensified, directly suppressing iron ore procurement demand and price increases, thus bringing certain negative pressure to the upstream shipping market. On the other hand, shipments from major global iron ore exporting countries have declined in stages, resulting in a relatively tight supply of large vessels available in the shipping market. This supply-demand mismatch has effectively offset the weak demand, ultimately supporting a counter-trend rise in Capesize freight rates and driving the sub-index higher. In stark contrast to the strong performance of Capesize vessels, the medium-sized Panamax vessel market showed a slight pullback, becoming the only drag on the market that day. Data shows that the Panamax vessel index fell slightly by 3 points, a decrease of 0.1%, closing at 2250 points, with an overall relatively stable trend. Correspondingly, vessel operating revenues saw slight adjustments. Panamax vessels, primarily engaged in the transportation of coal, grain, and other commodities in the 60,000 to 70,000 tonne class, saw their average daily revenue fall to the $19,254 range, resulting in a slight contraction in profitability. It is understood that Panamax vessels mainly serve the global cross-regional transportation of energy coal and grain. Recently, global coal trade demand has been stable, and the increase in grain shipping orders has been insufficient. Coupled with relatively ample short-term capacity deployment for this vessel type, the market supply and demand have been relaxed, ultimately leading to a slight decline in freight rates. The small vessel sector continued its moderate recovery, providing auxiliary support for the overall index's upward movement. The Supramax vessel index rose slightly by 1 point, or 0.1%, closing at 1707 points, marking a continuous slight upward trend. Supramax vessels are highly flexible and adaptable to a wide range of cargo types, mainly undertaking small-batch, multi-category dry bulk cargo transportation orders, covering building materials, niche minerals, and miscellaneous grains. Recent increases in global regional trade activity, with a continued rise in short-haul and fractional shipping orders in Southeast Asia, the Middle East, and Latin America, have driven a steady recovery in freight rates for smaller vessels. Although the increase is limited, it has solidified the foundation for the overall recovery of the dry bulk market. From an industry perspective, the current rise in the Baltic Dry Index directly reflects the rebalancing of supply and demand in the global dry bulk shipping market, highlighting structural differentiation. Large vessels benefit from the contraction in shipments of major mineral commodities and continued capacity constraints, while smaller vessels are steadily recovering due to the recovery in regional trade. Medium-sized vessels, however, are weaker due to lackluster demand for energy and food. In the short term, uncertainty regarding iron ore demand will persist. Changes in domestic steel mill production schedules and global commodity shipments will be key variables in the future trend of Capesize vessel freight rates. Meanwhile, with the global peak trade season approaching, dry bulk shipping demand is expected to continue to rise. If capacity supply remains tight, the Baltic Dry Index is likely to continue its upward trend, and the overall profitability of the industry is expected to continue to improve.

On July 13, 2026, the latest shipping market data showed that the Baltic Dry Index (BADI), a key indicator of international dry bulk shipping, steadily rose, reaching a new high in over a month since early June, marking a phase of recovery in the global dry bulk shipping market. This rise was not a general increase across all categories, but rather exhibited significant structural differentiation. Strong increases in freight rates for large Capesize and small-to-medium-sized Supramax vessels offset the slight decline in Panamax vessels, driving the overall market index higher and reflecting the differentiated changes in the current global supply and demand pattern for bulk commodities. Specifically, the Baltic Dry Index, which tracks freight rates for the three major dry bulk vessel types (Capesize, Panamax, and Supramax), rose 16 points, or 0.5%, to close at 2960 points, the highest closing level since early June, completely shaking off the previous volatile and sluggish trend. Looking at the data by vessel type, the core driver of this index rise was the strong rebound of Capesize vessels. As the mainstay of the dry bulk market, this vessel type has the greatest impact on the overall index weight. On that day, the Baltic Capesize Index surged 47 points, a gain exceeding 1%, closing at 4702 points, also reaching a high in over a month, becoming the core force driving the market upward. In terms of actual operating revenue, the profitability of Capesize vessels also rose. Data shows that Capesize vessels with a deadweight tonnage of 150,000 tons, primarily transporting bulk industrial raw materials such as iron ore and coal, saw their average daily revenue increase by $427 to $39,138 per day, with a steady recovery in per-vessel operating revenue, significantly boosting market confidence among large bulk carrier owners. Industry analysts point out that the recovery in Capesize freight rates stems primarily from the adjustment of the global bulk dry bulk shipping structure. Although upstream commodity prices fluctuate, the contraction in shipping supply has provided solid support for freight rates. From a fundamental perspective, the current iron ore shipping market exhibits a clear bullish-bearish tug-of-war pattern, which has become the core factor influencing Capesize freight rate fluctuations. On the one hand, recent international iron ore futures prices have continued to weaken, exacerbating operating pressures in the domestic steel industry. Steel mill losses have continued to widen, and expectations of industry production cuts and restrictions have intensified, directly suppressing iron ore procurement demand and price increases, thus bringing certain negative pressure to the upstream shipping market. On the other hand, shipments from major global iron ore exporting countries have declined in stages, resulting in a relatively tight supply of large vessels available in the shipping market. This supply-demand mismatch has effectively offset the weak demand, ultimately supporting a counter-trend rise in Capesize freight rates and driving the sub-index higher. In stark contrast to the strong performance of Capesize vessels, the medium-sized Panamax vessel market showed a slight pullback, becoming the only drag on the market that day. Data shows that the Panamax vessel index fell slightly by 3 points, a decrease of 0.1%, closing at 2250 points, with an overall relatively stable trend. Correspondingly, vessel operating revenues saw slight adjustments. Panamax vessels, primarily engaged in the transportation of coal, grain, and other commodities in the 60,000 to 70,000 tonne class, saw their average daily revenue fall to the $19,254 range, resulting in a slight contraction in profitability. It is understood that Panamax vessels mainly serve the global cross-regional transportation of energy coal and grain. Recently, global coal trade demand has been stable, and the increase in grain shipping orders has been insufficient. Coupled with relatively ample short-term capacity deployment for this vessel type, the market supply and demand have been relaxed, ultimately leading to a slight decline in freight rates. The small vessel sector continued its moderate recovery, providing auxiliary support for the overall index's upward movement. The Supramax vessel index rose slightly by 1 point, or 0.1%, closing at 1707 points, marking a continuous slight upward trend. Supramax vessels are highly flexible and adaptable to a wide range of cargo types, mainly undertaking small-batch, multi-category dry bulk cargo transportation orders, covering building materials, niche minerals, and miscellaneous grains. Recent increases in global regional trade activity, with a continued rise in short-haul and fractional shipping orders in Southeast Asia, the Middle East, and Latin America, have driven a steady recovery in freight rates for smaller vessels. Although the increase is limited, it has solidified the foundation for the overall recovery of the dry bulk market. From an industry perspective, the current rise in the Baltic Dry Index directly reflects the rebalancing of supply and demand in the global dry bulk shipping market, highlighting structural differentiation. Large vessels benefit from the contraction in shipments of major mineral commodities and continued capacity constraints, while smaller vessels are steadily recovering due to the recovery in regional trade. Medium-sized vessels, however, are weaker due to lackluster demand for energy and food. In the short term, uncertainty regarding iron ore demand will persist. Changes in domestic steel mill production schedules and global commodity shipments will be key variables in the future trend of Capesize vessel freight rates. Meanwhile, with the global peak trade season approaching, dry bulk shipping demand is expected to continue to rise. If capacity supply remains tight, the Baltic Dry Index is likely to continue its upward trend, and the overall profitability of the industry is expected to continue to improve.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.