Will there be a reversal at tonight's CPI+ hearing?

2026-07-14 20:10:11

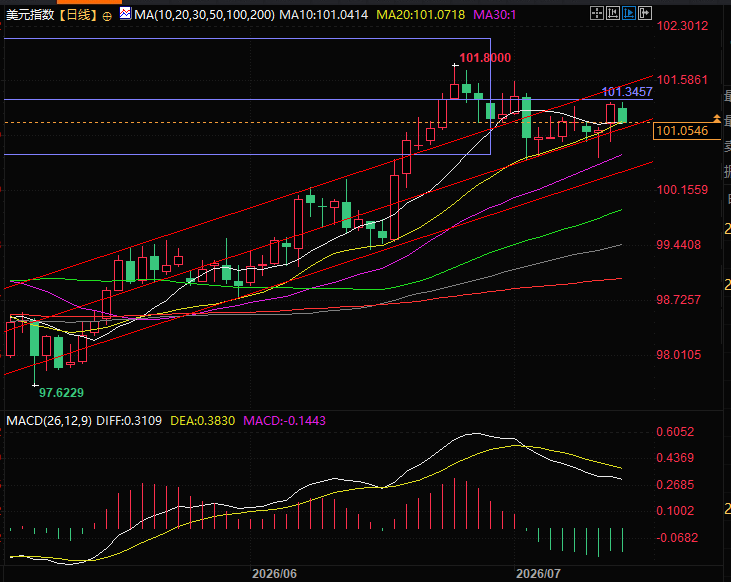

This week, global macro markets will see a key pricing inflection point. The release of the US June CPI inflation data, coupled with the highly anticipated semi-annual congressional hearings of Federal Reserve Chairman Warsh, will be the two core anchors influencing the Fed's July interest rate decision and reshaping US Treasury yields and global capital flows. Currently, hedge funds and fixed-income institutions have already made intensive portfolio adjustments, and market expectations for interest rate hikes are rapidly rising, completely reversing the previous trading logic of easing and rate cuts. The US dollar index has already fallen 0.25% to 101.05, suggesting that CPI may be lower than expected, and the recent continuous rise in interest rate hike expectations may be reversing.

(US Dollar Index Daily Chart, Source: EasyTrade) At 20:07 Beijing time, the US Dollar Index is currently at 101.06.

(US Dollar Index Daily Chart, Source: EasyTrade) At 20:07 Beijing time, the US Dollar Index is currently at 101.06.

Hawkish rhetoric ignites the market, significantly increasing the probability of a July rate hike.

Recent hawkish statements from the Federal Reserve have signaled the market's readjustment of interest rate hikes. Fed Governor Waller explicitly indicated that if June's core inflation data exceeds expectations again, the Fed will need to immediately begin tightening its policy by raising interest rates. As a result, market pricing in a July rate hike has jumped significantly. Data from interest rate derivatives shows that the probability of a 25 basis point rate hike this month has surged from less than 10% several weeks ago to around 50%. The yield on the highly policy-sensitive 2-year US Treasury bond has stabilized above 4.25%, directly reflecting the shift in market sentiment.Inflation is structurally diverging: overall inflation is cooling, but core stickiness remains high.

Market consensus anticipates that US inflation in June will exhibit a pattern of "overall cooling, but core stickiness remaining." The overall CPI year-on-year is expected to fall to 3.8% from 4.2% in May, but the core CPI will only decline slightly by 0.1 percentage point to 2.8%, indicating a continued moderate rise in monthly core prices. This structural inflation characteristic is the core reason why the market is hesitant to bet on a sustained decline in inflation and the continued fermentation of interest rate hike expectations.Geopolitical risks exacerbate inflation concerns, reinforcing the justification for monetary tightening.

Geopolitical risks have further amplified concerns about sticky inflation, providing additional support for the Federal Reserve to tighten policy. The escalating military conflict between the US and Iran and the intensified competition over the Strait of Hormuz have pushed international oil prices higher, significantly increasing uncertainty surrounding energy inflation . Even if overall inflation has somewhat subsided, the combination of rising energy costs and strong core prices leads the market to widely believe that current inflationary pressures are unlikely to spontaneously decline to the Fed's 2% target range, making further monetary tightening fully justified.The market has fully priced in the expected interest rate hikes this year.

With key data releases approaching, market trading logic has been fully pre-empted. Interest rate futures positioning data shows a significant increase in open interest in federal funds futures for August since July, indicating that institutions are positioning themselves in advance for policy changes. The market has already fully priced in at least one rate hike this year, and anticipates another round of rate hikes as early as mid-2027. Some institutions even believe that the three rate cuts implemented by the Federal Reserve last year due to employment concerns will likely be reversed, and the monetary policy cycle will fully enter a tightening phase.The Warsh hearing presents the biggest uncertainty: it lacks forward guidance and is highly data-dependent.

This congressional hearing for Warsh is a crucial window for his presidency, facing congressional questioning and representing the biggest source of market uncertainty this week. Unlike previous Fed officials' explicit forward guidance, Warsh has consistently avoided direct policy statements, favoring data-driven decision-making. This means that even if inflation data weakens slightly this time, the market will not fully priced in a July rate hike; and if inflation exceeds expectations, coupled with Warsh's hawkish testimony, the probability of a rate hike will surge further, and the real yield on US Treasury bonds will continue its upward trend.Asset Impact: Increased market volatility as institutions enter a critical window of opportunity.

For institutional funds such as hedge funds, the combined impact of inflation data and Warsh's testimony directly affects the trading pace of major asset classes. Volatility in US Treasury yields and interest rate derivatives will continue to amplify, simultaneously driving trend-based movements in the foreign exchange, bond, and equity markets. Institutions are generally adopting a wait-and-see approach, and subsequent position adjustments, interest rate trends, and the final pricing of interest rate hike expectations will depend entirely on the strength of inflation data and Warsh's policy statements. Technically, the US dollar index has fallen back to near the middle of its upward channel, which is highly unusual given the escalating geopolitical tensions and rising oil prices. A break below this level could reverse the dollar's upward trend. (US Dollar Index Daily Chart, Source: EasyTrade) At 20:07 Beijing time, the US Dollar Index is currently at 101.06.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.