Wall Street's trump card: Unveiling the three major "moats" protecting the US dollar index from European sell-offs.

2026-01-20 15:32:35

The tariff dispute between the US and Europe over the "Greenland issue" continues to escalate. The market once hotly debated whether Europe would use its $12.6 trillion in US financial assets to "weaponize capital" and impact the dollar index. However, an analysis by the Financial Times of the UK shows that this idea is ultimately unlikely to shake the core support of the dollar index, and its resilience is backed by profound market and structural logic.

As a core indicator of the world's major reserve currencies, the stability of the US dollar index is closely related to global capital flows and the dynamics of US asset holdings in various countries.

The current scale of US financial assets held by Europe is enormous: approximately $8 trillion in direct holdings, plus funds held by European financial institutions in the Middle East, Asia, and the United States, totaling $12.6 trillion.

Among them, European NATO member states, including Canada, hold $3.3 trillion in U.S. Treasury bonds, twice the combined holdings of Japan (approximately $1.1 trillion) and China ($730-770 billion). The movement of these assets was considered a potential variable affecting the dollar index.

From the perspective of the US economic structure, as of the end of June last year, its international investment position was a deep negative value of -$26.14 trillion, which means that the stability of the US dollar index is highly dependent on the continuous inflow of overseas capital.

George Saravelos, chief foreign exchange strategist at Deutsche Bank, once pointed out that the United States’ huge foreign deficit is essentially paid for by global capital, and that if Europe withdraws its funds after the deterioration of transatlantic relations, it could theoretically put pressure on the dollar index.

In fact, the Danish pension fund began reducing its holdings of dollar-denominated assets and repatriating funds last year. This sporadic move led the market to speculate whether Europe would launch a wave of "selling off US assets," thereby impacting the dollar index.

However, in reality, Europe's idea of "weaponizing capital" has faced multiple obstacles from the outset, making it difficult to have a substantial impact on the US dollar index.

First, there is the issue of asset ownership: the vast majority of these $12.6 trillion in US assets are held by thousands of private financial institutions and millions of individual investors in Europe, rather than being directly controlled by national governments.

Aside from "moral persuasion," European authorities lack effective means of coercive intervention and are unable to form a concerted effort to sell off assets. Meanwhile, decentralized private capital decisions prioritize market returns. Although the dollar has weakened compared to a year ago, the positive outlook for US economic growth means that private investors lack the incentive to significantly reduce their dollar holdings, making it difficult to shake the dollar index.

Secondly, the limited market capacity further blocked Europe's path to influence the US dollar index by selling assets.

If Europe were to sell off US assets on a large scale, a sufficiently large number of buyers would be needed to create an effective impact . However, the reality is that although the total market capitalization of MSCI Asia stocks is approximately US$13.5 trillion, which is close to the size of the assets that Europe plans to sell, the asset structures are vastly different. European investors will not easily sell off core growth stocks such as Nvidia and instead allocate to Japanese bonds, and Asian investors also lack the willingness and ability to take over such a huge amount of US assets.

The US domestic market, with a net international investment position of -$26 trillion, lacks the foundation to absorb the selling pressure, and the sharp depreciation of the dollar index is not in the core interests of the US, making it difficult for American society to reach a consensus.

More importantly, the deep integration of the European and American financial systems means that the impact of "selling off US assets" on the dollar index will inevitably backfire, ultimately resulting in more harm than good.

For export-oriented economies, selling off US Treasury bonds would lead to a sharp appreciation of the euro, which would in turn hurt their own exports. Europe and the United States have a high degree of financial integration.

If European banks and investors withdraw their holdings of US Treasury bonds on a large scale, it could trigger a collapse of the US dollar and a sharp drop in the US dollar index in the short term. However, this would be followed by a passive surge in the euro, which would severely damage Europe's export competitiveness and ultimately lead to a recession in the European economy. This "mutually destructive" consequence would make Europe unlikely to take action easily, and it would also become an implicit support for the US dollar index.

Societe Generale's chief foreign exchange strategist, Kit Jax, aptly observed that while the root of geopolitical turmoil lies in Washington, its spillover effects are far more pronounced, with overseas markets suffering far greater damage than those in the United States.

Trump’s tariff threats and the Greenland dispute may drive a slow “sell-off of US assets” in the market, but this sporadic movement is unlikely to have a significant impact.

In conclusion, the $12.6 trillion in US assets held by Europe, while seemingly a potential bargaining chip to counterbalance the US, are actually difficult to transform into an effective tool to influence the US dollar index due to multiple limitations such as asset ownership, market absorption capacity, and the risk of backlash.

As the "ballast" of the global financial market, the US dollar index is backed by the fundamentals of the US economy, the global capital demand for dollar assets, and the deep financial ties between Europe and the United States, which together constitute its resilience that is not easily shaken.

In the future, geopolitical competition between the US and Europe may still cause short-term fluctuations in the US dollar index, but the idea of Europe significantly impacting the US dollar index through "weaponization of capital" will ultimately be difficult to implement in the face of market reality.

The recent tensions between the US and Europe over Greenland have indeed put downward pressure on dollar assets. However, high-yield US Treasury bonds and the dependence of Europe and the US on dollar assets continue to support the dollar's performance. Traders should not be overly bearish on the dollar, as a slowdown in its decline could lead to a sharp rebound, which could impact the gold and currency markets.

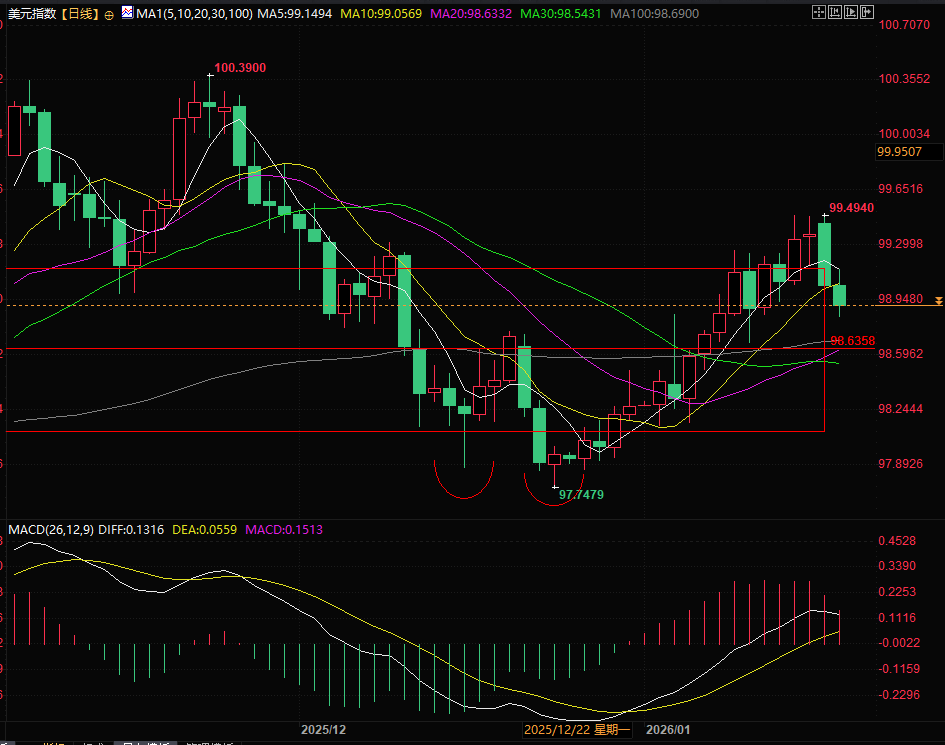

From a technical perspective, the US dollar index is currently consolidating around the support level of 98.90, as mentioned in last night's article. The extreme adjustment point is currently around 98.63. We need to pay attention to whether 98.90 will be broken. The resistance levels are at 99.15 and 99.23.

(US Dollar Index Daily Chart, Source: FX678)

At 15:30 Beijing time, the US dollar index is currently at 98.87.

As a core indicator of the world's major reserve currencies, the stability of the US dollar index is closely related to global capital flows and the dynamics of US asset holdings in various countries.

The current scale of US financial assets held by Europe is enormous: approximately $8 trillion in direct holdings, plus funds held by European financial institutions in the Middle East, Asia, and the United States, totaling $12.6 trillion.

Among them, European NATO member states, including Canada, hold $3.3 trillion in U.S. Treasury bonds, twice the combined holdings of Japan (approximately $1.1 trillion) and China ($730-770 billion). The movement of these assets was considered a potential variable affecting the dollar index.

Theoretical Logic: US Dependence on Foreign Investment May Pose Risks to the US Dollar Index

From the perspective of the US economic structure, as of the end of June last year, its international investment position was a deep negative value of -$26.14 trillion, which means that the stability of the US dollar index is highly dependent on the continuous inflow of overseas capital.

George Saravelos, chief foreign exchange strategist at Deutsche Bank, once pointed out that the United States’ huge foreign deficit is essentially paid for by global capital, and that if Europe withdraws its funds after the deterioration of transatlantic relations, it could theoretically put pressure on the dollar index.

In fact, the Danish pension fund began reducing its holdings of dollar-denominated assets and repatriating funds last year. This sporadic move led the market to speculate whether Europe would launch a wave of "selling off US assets," thereby impacting the dollar index.

Real-world obstacle 1: Dispersed asset ownership makes it difficult to form a concerted effort to sell off assets.

However, in reality, Europe's idea of "weaponizing capital" has faced multiple obstacles from the outset, making it difficult to have a substantial impact on the US dollar index.

First, there is the issue of asset ownership: the vast majority of these $12.6 trillion in US assets are held by thousands of private financial institutions and millions of individual investors in Europe, rather than being directly controlled by national governments.

Aside from "moral persuasion," European authorities lack effective means of coercive intervention and are unable to form a concerted effort to sell off assets. Meanwhile, decentralized private capital decisions prioritize market returns. Although the dollar has weakened compared to a year ago, the positive outlook for US economic growth means that private investors lack the incentive to significantly reduce their dollar holdings, making it difficult to shake the dollar index.

Second practical obstacle: Insufficient market absorption capacity, making it difficult to implement a sell-off strategy.

Secondly, the limited market capacity further blocked Europe's path to influence the US dollar index by selling assets.

If Europe were to sell off US assets on a large scale, a sufficiently large number of buyers would be needed to create an effective impact . However, the reality is that although the total market capitalization of MSCI Asia stocks is approximately US$13.5 trillion, which is close to the size of the assets that Europe plans to sell, the asset structures are vastly different. European investors will not easily sell off core growth stocks such as Nvidia and instead allocate to Japanese bonds, and Asian investors also lack the willingness and ability to take over such a huge amount of US assets.

The US domestic market, with a net international investment position of -$26 trillion, lacks the foundation to absorb the selling pressure, and the sharp depreciation of the dollar index is not in the core interests of the US, making it difficult for American society to reach a consensus.

Key risk: Deep financial ties mean that a sell-off will inevitably backfire.

More importantly, the deep integration of the European and American financial systems means that the impact of "selling off US assets" on the dollar index will inevitably backfire, ultimately resulting in more harm than good.

For export-oriented economies, selling off US Treasury bonds would lead to a sharp appreciation of the euro, which would in turn hurt their own exports. Europe and the United States have a high degree of financial integration.

If European banks and investors withdraw their holdings of US Treasury bonds on a large scale, it could trigger a collapse of the US dollar and a sharp drop in the US dollar index in the short term. However, this would be followed by a passive surge in the euro, which would severely damage Europe's export competitiveness and ultimately lead to a recession in the European economy. This "mutually destructive" consequence would make Europe unlikely to take action easily, and it would also become an implicit support for the US dollar index.

Market consensus: Short-term fluctuations are unlikely to alter the long-term resilience of the US dollar index.

Societe Generale's chief foreign exchange strategist, Kit Jax, aptly observed that while the root of geopolitical turmoil lies in Washington, its spillover effects are far more pronounced, with overseas markets suffering far greater damage than those in the United States.

Trump’s tariff threats and the Greenland dispute may drive a slow “sell-off of US assets” in the market, but this sporadic movement is unlikely to have a significant impact.

In conclusion, the $12.6 trillion in US assets held by Europe, while seemingly a potential bargaining chip to counterbalance the US, are actually difficult to transform into an effective tool to influence the US dollar index due to multiple limitations such as asset ownership, market absorption capacity, and the risk of backlash.

As the "ballast" of the global financial market, the US dollar index is backed by the fundamentals of the US economy, the global capital demand for dollar assets, and the deep financial ties between Europe and the United States, which together constitute its resilience that is not easily shaken.

In the future, geopolitical competition between the US and Europe may still cause short-term fluctuations in the US dollar index, but the idea of Europe significantly impacting the US dollar index through "weaponization of capital" will ultimately be difficult to implement in the face of market reality.

Summary and Technical Analysis:

The recent tensions between the US and Europe over Greenland have indeed put downward pressure on dollar assets. However, high-yield US Treasury bonds and the dependence of Europe and the US on dollar assets continue to support the dollar's performance. Traders should not be overly bearish on the dollar, as a slowdown in its decline could lead to a sharp rebound, which could impact the gold and currency markets.

From a technical perspective, the US dollar index is currently consolidating around the support level of 98.90, as mentioned in last night's article. The extreme adjustment point is currently around 98.63. We need to pay attention to whether 98.90 will be broken. The resistance levels are at 99.15 and 99.23.

(US Dollar Index Daily Chart, Source: FX678)

At 15:30 Beijing time, the US dollar index is currently at 98.87.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.