The signal for currency intervention has been clear; this time, the yen is different from before.

2026-02-24 18:21:02

On Tuesday (February 24), the USD/JPY pair continued its recent range-bound trading pattern, fluctuating between 152 and 158. Despite the Bank of Japan exiting negative interest rates, tapering bond purchases, and halting stock purchases, the yen has failed to find effective support, with the trade-weighted index even hitting a record low of 52.65 in January. The current core contradiction in the market lies in the fact that while fundamentals have created conditions for intervention, the technical picture shows a typical wait-and-see attitude, with both bulls and bears awaiting the release of key variables.

When the USD/JPY pair reached a high of 159.45 in January, news circulated that the Federal Reserve had inquired about the USD/JPY level, after which the exchange rate quickly fell back to around 152.10. In February, Japanese media further revealed that the US had proactively initiated a yen inquiry in January. The sensitivity of this detail lies in the fact that it suggests potential intervention may no longer be a unilateral action by the Japanese Ministry of Finance, but rather a joint intervention led or participated in by the US.

This shift in expectations is crucial. Looking back to July 2024, Japan unilaterally intervened using nearly $100 billion of its foreign exchange reserves, successfully lowering the dollar-yen exchange rate from 161.96 to 139.58. However, the effectiveness of unilateral intervention is often short-lived, and the market quickly returns to a depreciation trend. In contrast, the case of the Federal Reserve and the Bank of Japan jointly selling dollars in June 1998 is more relevant: the exchange rate plummeted from 142 to 137 that day, and although it fluctuated in the following months, it had fallen to around 101 by the end of 1999. The reason why joint intervention is more deterrent is that it directly challenges the US's "strong dollar" policy—if the US Treasury actively sells dollars, it is tantamount to admitting the weaponization of the exchange rate, and its impact on import costs is comparable to tariffs.

The core variable currently being focused on has shifted from "whether Japan will intervene" to "whether the United States will participate." A well-known institution points out that if the Federal Reserve does indeed sell dollars and buy yen, this would be an extremely rare instance of coordinated monetary policy, with spillover effects far exceeding the foreign exchange market itself. On one hand, the Nikkei index could repeat the scenario of the July 2024 intervention—falling from 42,000 points to 31,000 points; on the other hand, high-yield currencies in the carry trade chain (South African rand, Mexican peso, Hungarian forint) will face massive unwinding pressure. Safe-haven assets such as gold and the Swiss franc are expected to receive inflows, while the euro's rebound may be constrained by large speculative long positions.

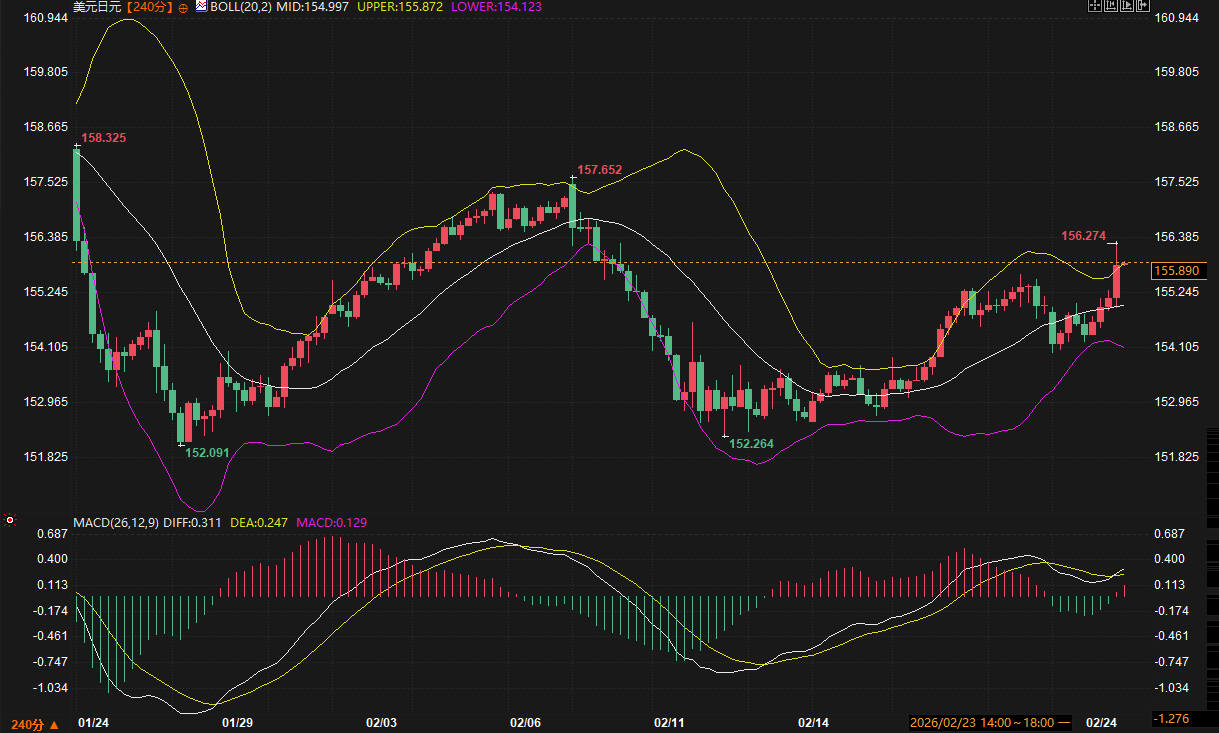

Observing the 240-minute candlestick chart, the USD/JPY pair has formed a clear trading range since the end of January, with the upper band at 158.325 and the lower band at 152.091. The recent trading range has further narrowed to between 152.264 and 157.652. The Bollinger Bands (BOLL) indicator shows that the middle band is currently at 154.998, while the upper and lower bands extend to 155.877 and 154.120 respectively. This narrowing bandwidth suggests that the price is about to face a directional choice.

The MACD indicator (26,12,9) shows a subtle bullish convergence pattern: the DIFF and DEA are converging near the zero line, both at 0.247, and the histogram is only 0.131, indicating that the short-term bullish and bearish forces are almost balanced. This technical pattern usually appears on the eve of a major news announcement—if there is no external intervention, the exchange rate will likely continue to fluctuate within a range; once intervention occurs, it may choose a direction through a gap or a rapid breakout.

It's worth noting that the current price consolidation zone (around 155) is precisely near the retracement level of the upward wave from the September 2024 low of 139.59 to the January 2026 high of 159.45. Based on historical intervention effectiveness, for coordinated action to have a substantial impact, the exchange rate would need to be pushed below the 2024 post-intervention low of 139.50—a technical breakdown on the daily chart.

Regarding support and resistance, the 152.10-152.28 area needs to be monitored in the short term. This is the intraday low after the "price inquiry" news in January and also an important defensive line for the bulls. If this area is broken, the next support will test the psychological level of 152.00 and the 151.50 level. On the upside, the 157.60-158.30 area constitutes strong resistance. If the January high of 158.325 is broken, it means that the intervention expectation has temporarily failed, and the exchange rate may test the 160 level.

Two key signals to watch during the trading session: first, any breaking news regarding exchange rates during the US session, especially wording related to changes in the Federal Reserve's stance; second, the correlation with the Nikkei 225 index. A single-day drop of more than 2% in Japanese stocks often indicates accelerated unwinding of carry trades, passively strengthening the yen. Furthermore, some institutional traders have noted a recent increase in the skewness of implied volatility options on the yen, suggesting that hedge funds are beginning to establish protective positions to mitigate intervention risks.

Looking ahead, the USD/JPY exchange rate is in the final stages of a tug-of-war between "intervention expectations" and "fundamental inertia." On the one hand, Japanese authorities face pressure from the historically low yen trade-weighted index; on the other hand, the increased risk of a pullback in US stocks provides "cover" for intervention—compared to the previously accumulated huge gains, a 10% pullback in Japanese stocks would be more psychologically acceptable to the market.

The real risk lies in the fact that if coordinated intervention is implemented, its impact will not be limited to the exchange rate itself. As the largest foreign holder of US Treasury bonds, if intervention puts pressure on domestic asset prices, it could trigger its investors to reduce their holdings of US Treasury bonds to balance their balance sheets, leading to an increase in US Treasury yields and consequently impacting global risk assets. This chain reaction of "foreign exchange market intervention—bond market sell-off—stock market decline" could become a new source of market volatility in 2026.

For market participants, the current price level does not offer a safety margin for trend trading; reversal signals at the edge of the range are more valuable than chasing breakouts. Regardless of intervention, the yen exchange rate will enter a period of high volatility, and the final direction of the exchange rate will depend on whether this action ends with a "verbal warning" or leads to "joint action."

Fundamentals: Intervention expectations shift from "unilateral" to "joint".

When the USD/JPY pair reached a high of 159.45 in January, news circulated that the Federal Reserve had inquired about the USD/JPY level, after which the exchange rate quickly fell back to around 152.10. In February, Japanese media further revealed that the US had proactively initiated a yen inquiry in January. The sensitivity of this detail lies in the fact that it suggests potential intervention may no longer be a unilateral action by the Japanese Ministry of Finance, but rather a joint intervention led or participated in by the US.

This shift in expectations is crucial. Looking back to July 2024, Japan unilaterally intervened using nearly $100 billion of its foreign exchange reserves, successfully lowering the dollar-yen exchange rate from 161.96 to 139.58. However, the effectiveness of unilateral intervention is often short-lived, and the market quickly returns to a depreciation trend. In contrast, the case of the Federal Reserve and the Bank of Japan jointly selling dollars in June 1998 is more relevant: the exchange rate plummeted from 142 to 137 that day, and although it fluctuated in the following months, it had fallen to around 101 by the end of 1999. The reason why joint intervention is more deterrent is that it directly challenges the US's "strong dollar" policy—if the US Treasury actively sells dollars, it is tantamount to admitting the weaponization of the exchange rate, and its impact on import costs is comparable to tariffs.

The core variable currently being focused on has shifted from "whether Japan will intervene" to "whether the United States will participate." A well-known institution points out that if the Federal Reserve does indeed sell dollars and buy yen, this would be an extremely rare instance of coordinated monetary policy, with spillover effects far exceeding the foreign exchange market itself. On one hand, the Nikkei index could repeat the scenario of the July 2024 intervention—falling from 42,000 points to 31,000 points; on the other hand, high-yield currencies in the carry trade chain (South African rand, Mexican peso, Hungarian forint) will face massive unwinding pressure. Safe-haven assets such as gold and the Swiss franc are expected to receive inflows, while the euro's rebound may be constrained by large speculative long positions.

Technical Analysis: Critical Point Selection in a Converging Pattern

Observing the 240-minute candlestick chart, the USD/JPY pair has formed a clear trading range since the end of January, with the upper band at 158.325 and the lower band at 152.091. The recent trading range has further narrowed to between 152.264 and 157.652. The Bollinger Bands (BOLL) indicator shows that the middle band is currently at 154.998, while the upper and lower bands extend to 155.877 and 154.120 respectively. This narrowing bandwidth suggests that the price is about to face a directional choice.

The MACD indicator (26,12,9) shows a subtle bullish convergence pattern: the DIFF and DEA are converging near the zero line, both at 0.247, and the histogram is only 0.131, indicating that the short-term bullish and bearish forces are almost balanced. This technical pattern usually appears on the eve of a major news announcement—if there is no external intervention, the exchange rate will likely continue to fluctuate within a range; once intervention occurs, it may choose a direction through a gap or a rapid breakout.

It's worth noting that the current price consolidation zone (around 155) is precisely near the retracement level of the upward wave from the September 2024 low of 139.59 to the January 2026 high of 159.45. Based on historical intervention effectiveness, for coordinated action to have a substantial impact, the exchange rate would need to be pushed below the 2024 post-intervention low of 139.50—a technical breakdown on the daily chart.

Key price levels and points to watch during trading hours

Regarding support and resistance, the 152.10-152.28 area needs to be monitored in the short term. This is the intraday low after the "price inquiry" news in January and also an important defensive line for the bulls. If this area is broken, the next support will test the psychological level of 152.00 and the 151.50 level. On the upside, the 157.60-158.30 area constitutes strong resistance. If the January high of 158.325 is broken, it means that the intervention expectation has temporarily failed, and the exchange rate may test the 160 level.

Two key signals to watch during the trading session: first, any breaking news regarding exchange rates during the US session, especially wording related to changes in the Federal Reserve's stance; second, the correlation with the Nikkei 225 index. A single-day drop of more than 2% in Japanese stocks often indicates accelerated unwinding of carry trades, passively strengthening the yen. Furthermore, some institutional traders have noted a recent increase in the skewness of implied volatility options on the yen, suggesting that hedge funds are beginning to establish protective positions to mitigate intervention risks.

Outlook: Intervention Window and Market Structure Changes

Looking ahead, the USD/JPY exchange rate is in the final stages of a tug-of-war between "intervention expectations" and "fundamental inertia." On the one hand, Japanese authorities face pressure from the historically low yen trade-weighted index; on the other hand, the increased risk of a pullback in US stocks provides "cover" for intervention—compared to the previously accumulated huge gains, a 10% pullback in Japanese stocks would be more psychologically acceptable to the market.

The real risk lies in the fact that if coordinated intervention is implemented, its impact will not be limited to the exchange rate itself. As the largest foreign holder of US Treasury bonds, if intervention puts pressure on domestic asset prices, it could trigger its investors to reduce their holdings of US Treasury bonds to balance their balance sheets, leading to an increase in US Treasury yields and consequently impacting global risk assets. This chain reaction of "foreign exchange market intervention—bond market sell-off—stock market decline" could become a new source of market volatility in 2026.

For market participants, the current price level does not offer a safety margin for trend trading; reversal signals at the edge of the range are more valuable than chasing breakouts. Regardless of intervention, the yen exchange rate will enter a period of high volatility, and the final direction of the exchange rate will depend on whether this action ends with a "verbal warning" or leads to "joint action."

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.