The closure of the Strait of Hormuz marks the darkest moment for the global energy supply chain.

2026-03-03 15:34:45

A senior commander of Iran's Islamic Revolutionary Guard Corps announced on Monday (March 2) that the Strait of Hormuz had been closed and warned that any ships attempting to pass through the waterway would be attacked. This statement, released by Iranian state media, quickly triggered strong turmoil in global energy markets. During Tuesday's Asian and European trading sessions, US crude oil prices fluctuated upwards, currently trading around $73.25 per barrel, a daily increase of approximately 2.8%.

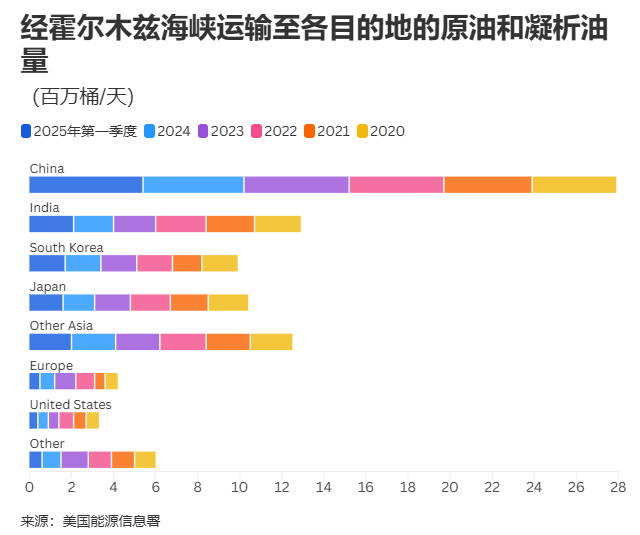

The Strait of Hormuz, located between Iran and Oman, is a vital waterway for global oil trade. According to data from energy consultancy Kpler, approximately 13 million barrels of crude oil will pass through the strait daily in 2025, accounting for about 31% of global seaborne crude oil traffic.

In addition, about 20% of liquefied natural gas (LNG) exports from the Persian Gulf are also highly dependent on this route, mainly from Qatar.

The Iranian action comes at a time of escalating US-Israeli joint strikes against Iran, resulting in a significant contraction in shipping traffic, multiple insurance companies canceling coverage of the war zone, and numerous oil tankers being damaged or stranded. International benchmark Brent crude oil prices have risen nearly 10% since the conflict began. Market analysts warn that if the blockade continues for several weeks, oil prices could break through the $100 per barrel mark.

Qatar, one of the world’s largest LNG suppliers, announced on Monday that it was suspending LNG production due to Iranian drone attacks on its Ras Raffan and Mesayed industrial city facilities, further exacerbating global gas supply shortages and causing spot prices in Asia and Europe to surge significantly.

Analysts generally believe that Asia will be the hardest hit by this energy crisis. A Nomura report on Monday pointed out that Thailand, India, South Korea, and the Philippines are the most vulnerable due to their high dependence on energy imports, while Malaysia, as a net energy exporter, may benefit relatively.

South Asian countries are highly dependent on Gulf LNG. Kpler data shows that Qatar and the UAE account for 99% of Pakistan's LNG imports, Bangladesh 72%, and India 53%. Pakistan and Bangladesh have limited storage capacity and poor procurement flexibility. Once the supply is disrupted, it could quickly lead to demand destruction in the power sector, rather than filling the gap through high-priced spot bidding.

India faces the largest combined exposure in the region: over half of its LNG imports are linked to the Gulf, and many contracts are priced using the Brent index. The Straits crisis will simultaneously drive up crude oil import costs and LNG contract prices, creating a "double physical and financial shock." Furthermore, approximately 60% of India's crude oil imports come from the Middle East, and a continued blockade will significantly amplify its energy import bills and current account pressures.

The Middle East supplies 75% of Japan's crude oil imports and 70% of South Korea's. Regarding LNG, the Gulf region has a relatively lower dependence (South Korea 14%, Japan 6%), but their high energy import dependence makes them highly sensitive to price shocks.

South Korea has approximately 3.5 million tons of LNG in stock, while Japan has about 4.4 million tons, enough to stabilize demand for only 2-4 weeks. South Korea's net oil imports account for 2.7% of its GDP, leading Nomura to classify it as one of the most vulnerable economies in terms of its current account. Price increases, rather than physical shortages, will be the primary pain point.

For most Southeast Asian economies, the immediate impact will be on cost-side inflation rather than immediate supply shortages. Buyers reliant on spot LNG will face fierce competition from Europe for Atlantic cargoes, leading to a surge in replacement costs.

In Nomura's analytical framework, Thailand is considered Asia's biggest "oil price loser": its net oil imports account for 4.7% of its GDP, and every 10% increase in oil prices will worsen the current account by about 0.5 percentage points of GDP.

The Strait of Hormuz crisis highlights the extreme fragility of the global energy supply chain. In the short term, high oil and gas prices will exacerbate inflationary pressures and trade imbalances in Asian importing countries; if the conflict drags on, the global economy may face a new wave of energy shocks.

The market is closely watching the risk of escalation and the emergency coordination capabilities of major consuming and oil-producing countries.

(US crude oil daily chart, source: FX678)

At 15:32 Beijing time, US crude oil futures were trading at $73.23 per barrel.

The strategic importance of the Strait of Hormuz

The Strait of Hormuz, located between Iran and Oman, is a vital waterway for global oil trade. According to data from energy consultancy Kpler, approximately 13 million barrels of crude oil will pass through the strait daily in 2025, accounting for about 31% of global seaborne crude oil traffic.

In addition, about 20% of liquefied natural gas (LNG) exports from the Persian Gulf are also highly dependent on this route, mainly from Qatar.

Immediate response of oil and gas prices and potential extreme scenarios

The Iranian action comes at a time of escalating US-Israeli joint strikes against Iran, resulting in a significant contraction in shipping traffic, multiple insurance companies canceling coverage of the war zone, and numerous oil tankers being damaged or stranded. International benchmark Brent crude oil prices have risen nearly 10% since the conflict began. Market analysts warn that if the blockade continues for several weeks, oil prices could break through the $100 per barrel mark.

Qatar, one of the world’s largest LNG suppliers, announced on Monday that it was suspending LNG production due to Iranian drone attacks on its Ras Raffan and Mesayed industrial city facilities, further exacerbating global gas supply shortages and causing spot prices in Asia and Europe to surge significantly.

Asian economies will be hit hardest: Import dependence determines the severity of the impact.

Analysts generally believe that Asia will be the hardest hit by this energy crisis. A Nomura report on Monday pointed out that Thailand, India, South Korea, and the Philippines are the most vulnerable due to their high dependence on energy imports, while Malaysia, as a net energy exporter, may benefit relatively.

South Asia: LNG supply faces immediate physical disruption

South Asian countries are highly dependent on Gulf LNG. Kpler data shows that Qatar and the UAE account for 99% of Pakistan's LNG imports, Bangladesh 72%, and India 53%. Pakistan and Bangladesh have limited storage capacity and poor procurement flexibility. Once the supply is disrupted, it could quickly lead to demand destruction in the power sector, rather than filling the gap through high-priced spot bidding.

India faces the largest combined exposure in the region: over half of its LNG imports are linked to the Gulf, and many contracts are priced using the Brent index. The Straits crisis will simultaneously drive up crude oil import costs and LNG contract prices, creating a "double physical and financial shock." Furthermore, approximately 60% of India's crude oil imports come from the Middle East, and a continued blockade will significantly amplify its energy import bills and current account pressures.

Japan and South Korea: Extremely sensitive to oil prices, with limited inventory buffers.

The Middle East supplies 75% of Japan's crude oil imports and 70% of South Korea's. Regarding LNG, the Gulf region has a relatively lower dependence (South Korea 14%, Japan 6%), but their high energy import dependence makes them highly sensitive to price shocks.

South Korea has approximately 3.5 million tons of LNG in stock, while Japan has about 4.4 million tons, enough to stabilize demand for only 2-4 weeks. South Korea's net oil imports account for 2.7% of its GDP, leading Nomura to classify it as one of the most vulnerable economies in terms of its current account. Price increases, rather than physical shortages, will be the primary pain point.

Southeast Asia: Cost and inflationary pressures take the lead, with Thailand experiencing a particularly significant impact.

For most Southeast Asian economies, the immediate impact will be on cost-side inflation rather than immediate supply shortages. Buyers reliant on spot LNG will face fierce competition from Europe for Atlantic cargoes, leading to a surge in replacement costs.

In Nomura's analytical framework, Thailand is considered Asia's biggest "oil price loser": its net oil imports account for 4.7% of its GDP, and every 10% increase in oil prices will worsen the current account by about 0.5 percentage points of GDP.

Conclusion: The fragility of the global energy supply chain has been further confirmed.

The Strait of Hormuz crisis highlights the extreme fragility of the global energy supply chain. In the short term, high oil and gas prices will exacerbate inflationary pressures and trade imbalances in Asian importing countries; if the conflict drags on, the global economy may face a new wave of energy shocks.

The market is closely watching the risk of escalation and the emergency coordination capabilities of major consuming and oil-producing countries.

(US crude oil daily chart, source: FX678)

At 15:32 Beijing time, US crude oil futures were trading at $73.23 per barrel.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.