The difficulty in lowering the energy component of the US February CPI may trigger risk aversion.

2026-03-11 17:25:18

According to APP, Ilya Spivak, global head of macro at Tastylive , said the next catalyst for the market is likely to come from inflation data itself. Economists expect the U.S. overall CPI to rise 2.4% year-on-year in February , and the core CPI to rise 2.5% year-on-year.

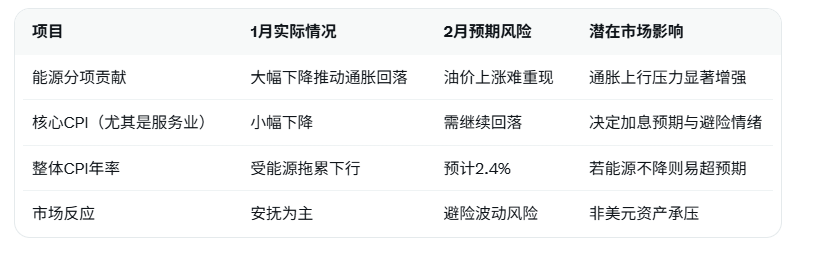

However, beneath the surface of the data, a key risk looms. A significant driver of the January CPI data was the declining contribution of energy prices to overall inflation, but given that oil prices have already begun to rise in early 2026 , replicating this seems extremely difficult. Whatever this means for the energy component of the February CPI data, traders will be keenly watching whether core price growth (especially in the services sector) continues its slight decline. This could fuel hopes for inflation normalization after the Middle East conflict subsides, helping to calm market anxieties. If not, fragile financial markets could experience another wave of risk aversion , as investors will again face the possibility of interest rates remaining high for an extended period. This would foreshadow a precarious situation for stocks, bonds, and currencies other than the US dollar.

To visually compare the differences in inflation drivers between January and February, the following table summarizes the key risk factors:

Ilya Spivak 's analysis hits the nail on the head: the rebound in energy prices is a done deal, and if the stickiness of inflation in the service sector cannot be further eased, it will reignite the pricing logic of "higher interest rates for longer periods." Traders are currently paying close attention to the service sector sub-data; any unexpected slowdown could temporarily boost risk appetite, while conversely, it could trigger a new round of dollar strength and asset sell-offs.

At a deeper level, this inflation data window coincides with a vulnerable period in global financial markets. While the anticipated easing of tensions in the Middle East provides a buffer, the uncertainty surrounding oil price paths has made investors extremely cautious about the Federal Reserve's policy direction. Non-dollar asset pricing will be directly constrained by this, and stock market valuations, bond yields, and exchange rate volatility may all be amplified simultaneously.

Editor's Summary

Ilya Spivak's accurate prediction highlights the decisive role of the February CPI data in market sentiment. The trends of the energy sub-index and the core service sector will become the core of short-term pricing, and investors need to closely track the actual release results to dynamically adjust their risk exposure.

Frequently Asked Questions

1. Question: Why does Ilya Spivak believe that the February CPI will be the next major catalyst for the market?

A: Because the market has already fully priced in geopolitical and policy expectations, inflation data is the only key variable yet to be realized. While the consensus forecast of 2.4% for overall CPI and 2.5% for core CPI is moderate, the energy component is unlikely to replicate the decline in January due to rising oil prices. The trend of core service sector prices will directly determine the market's confidence in "inflation normalization," and any deviation could trigger sharp fluctuations.

2. Question: Why is it difficult for the decline in energy contribution in January to be repeated in February?

A: Oil prices entered an upward trend at the beginning of 2026, and the ongoing conflict in the Middle East continues to push up energy costs. This external factor contrasts sharply with the low base effect in January. The drag on the overall CPI from the energy component will significantly weaken, or even turn into a positive contribution, making it easier for the overall inflation reading to exceed expectations and amplifying the upside risks.

3. Question: What would be the consequences if the growth of core service sector prices failed to continue its slight decline?

A: This will shatter market optimism about a sustained decline in inflation, causing investors to reprice the probability of "high interest rates lasting longer," leading to a rapid rise in risk aversion. Non-dollar stocks, bonds, and currencies will face selling pressure, while the dollar index may strengthen further, creating a typical "risk-averse" trading pattern.

4. Question: How will expectations of a de-escalation of the Middle East conflict affect the interpretation of inflation data?

A: If inflation in the service sector continues to decline, the market will interpret this as a positive signal of inflation normalization after the easing of conflict, thereby calming sentiment and supporting risk assets; conversely, it will strengthen concerns about "energy spillover + sticky inflation", and fragile markets will once again experience risk aversion volatility, further postponing the window for policy easing.

5. Question: How should ordinary investors plan ahead before the release of the February CPI data?

A: We recommend closely monitoring the performance of the services sector and energy prices. In the short term, it's advisable to moderately increase holdings of dollar assets or defensive bonds to hedge against upside risks. Simultaneously, set clear stop-loss levels to avoid excessive exposure to non-dollar stocks and emerging market currencies. After the data release, if the energy sector outperforms expectations, quickly reduce holdings of risky assets; if the services sector continues to decline, consider buying into sectors benefiting from easing expectations. In the long term, maintain flexible positioning, dynamically adjusting based on subsequent statements from the Federal Reserve, and diversify allocations to address the uncertainty of the inflation path.

However, beneath the surface of the data, a key risk looms. A significant driver of the January CPI data was the declining contribution of energy prices to overall inflation, but given that oil prices have already begun to rise in early 2026 , replicating this seems extremely difficult. Whatever this means for the energy component of the February CPI data, traders will be keenly watching whether core price growth (especially in the services sector) continues its slight decline. This could fuel hopes for inflation normalization after the Middle East conflict subsides, helping to calm market anxieties. If not, fragile financial markets could experience another wave of risk aversion , as investors will again face the possibility of interest rates remaining high for an extended period. This would foreshadow a precarious situation for stocks, bonds, and currencies other than the US dollar.

To visually compare the differences in inflation drivers between January and February, the following table summarizes the key risk factors:

Ilya Spivak 's analysis hits the nail on the head: the rebound in energy prices is a done deal, and if the stickiness of inflation in the service sector cannot be further eased, it will reignite the pricing logic of "higher interest rates for longer periods." Traders are currently paying close attention to the service sector sub-data; any unexpected slowdown could temporarily boost risk appetite, while conversely, it could trigger a new round of dollar strength and asset sell-offs.

At a deeper level, this inflation data window coincides with a vulnerable period in global financial markets. While the anticipated easing of tensions in the Middle East provides a buffer, the uncertainty surrounding oil price paths has made investors extremely cautious about the Federal Reserve's policy direction. Non-dollar asset pricing will be directly constrained by this, and stock market valuations, bond yields, and exchange rate volatility may all be amplified simultaneously.

Editor's Summary

Ilya Spivak's accurate prediction highlights the decisive role of the February CPI data in market sentiment. The trends of the energy sub-index and the core service sector will become the core of short-term pricing, and investors need to closely track the actual release results to dynamically adjust their risk exposure.

Frequently Asked Questions

1. Question: Why does Ilya Spivak believe that the February CPI will be the next major catalyst for the market?

A: Because the market has already fully priced in geopolitical and policy expectations, inflation data is the only key variable yet to be realized. While the consensus forecast of 2.4% for overall CPI and 2.5% for core CPI is moderate, the energy component is unlikely to replicate the decline in January due to rising oil prices. The trend of core service sector prices will directly determine the market's confidence in "inflation normalization," and any deviation could trigger sharp fluctuations.

2. Question: Why is it difficult for the decline in energy contribution in January to be repeated in February?

A: Oil prices entered an upward trend at the beginning of 2026, and the ongoing conflict in the Middle East continues to push up energy costs. This external factor contrasts sharply with the low base effect in January. The drag on the overall CPI from the energy component will significantly weaken, or even turn into a positive contribution, making it easier for the overall inflation reading to exceed expectations and amplifying the upside risks.

3. Question: What would be the consequences if the growth of core service sector prices failed to continue its slight decline?

A: This will shatter market optimism about a sustained decline in inflation, causing investors to reprice the probability of "high interest rates lasting longer," leading to a rapid rise in risk aversion. Non-dollar stocks, bonds, and currencies will face selling pressure, while the dollar index may strengthen further, creating a typical "risk-averse" trading pattern.

4. Question: How will expectations of a de-escalation of the Middle East conflict affect the interpretation of inflation data?

A: If inflation in the service sector continues to decline, the market will interpret this as a positive signal of inflation normalization after the easing of conflict, thereby calming sentiment and supporting risk assets; conversely, it will strengthen concerns about "energy spillover + sticky inflation", and fragile markets will once again experience risk aversion volatility, further postponing the window for policy easing.

5. Question: How should ordinary investors plan ahead before the release of the February CPI data?

A: We recommend closely monitoring the performance of the services sector and energy prices. In the short term, it's advisable to moderately increase holdings of dollar assets or defensive bonds to hedge against upside risks. Simultaneously, set clear stop-loss levels to avoid excessive exposure to non-dollar stocks and emerging market currencies. After the data release, if the energy sector outperforms expectations, quickly reduce holdings of risky assets; if the services sector continues to decline, consider buying into sectors benefiting from easing expectations. In the long term, maintain flexible positioning, dynamically adjusting based on subsequent statements from the Federal Reserve, and diversify allocations to address the uncertainty of the inflation path.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.