The US dollar index is nearing a 10-month high, but the bullish structure may be difficult to sustain.

2026-03-17 16:35:45

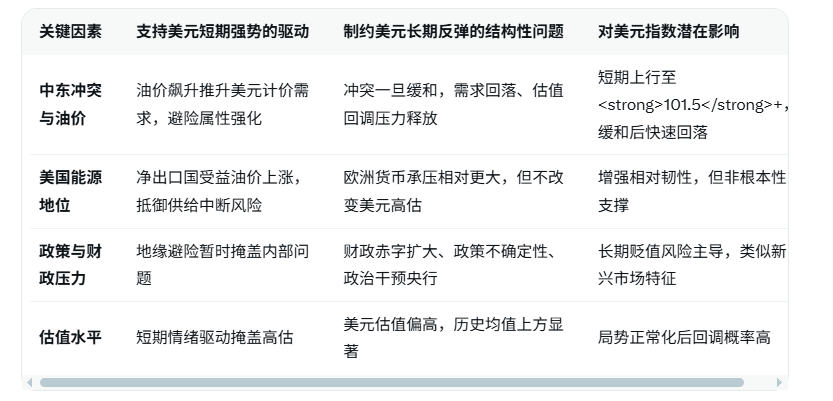

According to APP reports, driven by both the escalating conflict in the Middle East and a sharp rise in international oil prices, the US dollar index (DXY) has recently rebounded strongly, repeatedly breaking through the 100 mark and approaching a 10-month high (the 100.85-101.05 range ). HSBC forex analysts noted in their latest research report: "The geopolitical tensions in the Middle East have once again confirmed the US dollar's status as the primary safe-haven currency. This attribute has never truly changed compared to the market narrative nearly a year ago." As a major global oil exporter, the United States directly benefits from rising oil prices—crude oil is priced in US dollars, and soaring oil prices significantly boost demand for the dollar. At the same time, the resurgence of risk aversion further strengthens the dollar's attractiveness, while traditional safe-haven currencies such as the Japanese yen and Swiss franc have performed relatively poorly in this round of conflict.

Since the outbreak of the Middle East conflict on February 28, 2026, the global foreign exchange market landscape has undergone significant changes. As a net energy exporter, the United States is far more resilient to the potential disruption risks from the Strait of Hormuz than major European economies. Europe, heavily reliant on energy imports, is highly sensitive to oil price fluctuations, putting significant pressure on currencies such as the euro and the pound sterling. In contrast, the United States has achieved over 100% self-sufficiency in crude oil, meaning that rising oil prices translate more into increased demand for the US dollar than into domestic cost pressures.

However, several institutions have issued clear warnings about the sustainability of the dollar's rebound. Russ Mould, investment director at AJ Bell, one of the UK's largest investment platforms, stated, "The fundamental problems that led to the dollar's previous weakness remain, including uncertainty surrounding US policy, the widening fiscal deficit, and political pressure on central bank independence. Frankly, investors associate these characteristics more with emerging markets than developed economies." Arbuthnot Latham, investment director at private bank, similarly pointed out, "As long as the crisis continues, the dollar is expected to remain strong; but once things return to normal, downward pressure on the dollar will re-emerge. Currently, the dollar's valuation remains relatively high, and in the long run, this is the core variable determining its long-term returns."

HSBC's research report further emphasizes that the macroeconomic drivers supporting the dollar's strength in 2022 no longer exist. In the first half of 2025, the market's confidence in US assets will be severely damaged by the Trump administration's repeated "Liberation Day" tariff policies, resulting in the dollar index recording its worst half-year performance in half a century, with a full-year decline of nearly 10% , marking the official end of a 15-year dollar bull market cycle. The current rebound is more of a short-term phenomenon driven by geopolitics; once the situation in the Middle East eases, structural weakness will once again dominate the dollar's trajectory.

Overall, the current rebound in the US dollar index is mainly driven by geopolitics and energy prices. HSBC confirms its safe-haven status remains unchanged, but both AJ Bell and Arbuthnot Latham emphasize that structural problems (policy uncertainty, fiscal deficits, and pressure on central bank independence) remain unresolved, making the rebound fragile. Once there are signs of easing tensions in the Middle East, the dollar may return to a depreciation trend. Investors need to be wary of the gap between short-term strength and long-term weakness, and closely monitor the progress of the conflict, oil price trends, and US fiscal/policy developments.

Editor's Summary:

The Middle East conflict and soaring oil prices have temporarily reshaped the dollar's safe-haven appeal, pushing the dollar index near a 10-month high, with HSBC confirming its continued leading position. However, both AJ Bell and Arbuthnot Latham warned that unresolved structural issues such as policy uncertainty, fiscal deficits, and central bank independence have led to a high dollar valuation and questionable sustainability of the rebound. Once geopolitical tensions ease, depreciation pressures will once again dominate.

Frequently Asked Questions

1. Why did the Middle East conflict and soaring oil prices drive a rapid rebound in the US dollar index?

Crude oil is priced in US dollars, and rising oil prices (WTI around $ 100.20 /barrel, Brent around $ 103.50 /barrel) directly increase global demand for the dollar. Simultaneously, geopolitical tensions boost risk aversion, leading to capital inflows into dollar assets. HSBC analysts point out that this rebound reaffirms the dollar's status as the primary safe-haven currency. The US, as a net energy exporter, further benefits from rising oil prices, while currencies of energy-import-dependent economies such as Europe face significant pressure.

2. The US dollar index is currently approaching a 10-month high, but why do many institutions believe that the rebound is unlikely to last?

AJ Bell's Chief Investment Officer, Russ Molde, emphasized that the structural problems leading to a significant weakening of the US dollar in 2025 remain: a lack of policy consistency in the US government, a continuing widening fiscal deficit, and political interference affecting the independence of the Federal Reserve. These characteristics are causing investors to worry about the long-term stability of the US economy. Arbuthnot Latham also pointed out that the dollar is currently overvalued, and once the situation in the Middle East eases and safe-haven demand subsides, the pressure for a valuation correction will be released rapidly.

3. What are the specific mechanisms by which the United States benefits from rising oil prices?

The United States has become a net exporter of crude oil, making it highly resilient to the risk of supply disruptions through the Strait of Hormuz. Rising oil prices increase oil export revenues, while the fact that global oil transactions are settled in US dollars further boosts demand for the dollar. Unlike Europe, the negative impact of rising domestic energy costs in the United States on inflation and growth is relatively manageable, making the dollar more resilient in conflict environments.

4. Why did the US dollar experience a historic period of weakness?

In the first half of 2025, the Trump administration's announcement and subsequent rapid withdrawal of "Liberation Day" tariffs led to a sharp decline in market confidence in US assets, resulting in the worst half-year performance for the US dollar index in over half a century, with a full-year drop of nearly 10% . Morgan Stanley and other institutions confirmed that this marks the end of a 15-year bull market for the US dollar. The current rebound is more of a short-term, geopolitically driven phenomenon than a fundamental improvement.

5. What are the key points to watch for in the future trend of the US dollar?

In the short term, the outlook depends on the evolution of the Middle East conflict: if tensions persist, safe-haven demand for the dollar and support from oil prices could push the dollar index further above 101.5 ; if the situation eases rapidly, the safe-haven premium will subside, and the dollar will face a valuation correction. In the long term, the outlook depends on whether the structural problems within the US worsen—whether the fiscal deficit spirals out of control, whether political intervention in the Federal Reserve intensifies, and whether policy uncertainty persists. Investors should simultaneously monitor oil prices, the progress of the conflict, US fiscal data, and the Federal Reserve's statements to determine whether the rebound will become sustainable or whether it will return to a depreciation trend.

Since the outbreak of the Middle East conflict on February 28, 2026, the global foreign exchange market landscape has undergone significant changes. As a net energy exporter, the United States is far more resilient to the potential disruption risks from the Strait of Hormuz than major European economies. Europe, heavily reliant on energy imports, is highly sensitive to oil price fluctuations, putting significant pressure on currencies such as the euro and the pound sterling. In contrast, the United States has achieved over 100% self-sufficiency in crude oil, meaning that rising oil prices translate more into increased demand for the US dollar than into domestic cost pressures.

However, several institutions have issued clear warnings about the sustainability of the dollar's rebound. Russ Mould, investment director at AJ Bell, one of the UK's largest investment platforms, stated, "The fundamental problems that led to the dollar's previous weakness remain, including uncertainty surrounding US policy, the widening fiscal deficit, and political pressure on central bank independence. Frankly, investors associate these characteristics more with emerging markets than developed economies." Arbuthnot Latham, investment director at private bank, similarly pointed out, "As long as the crisis continues, the dollar is expected to remain strong; but once things return to normal, downward pressure on the dollar will re-emerge. Currently, the dollar's valuation remains relatively high, and in the long run, this is the core variable determining its long-term returns."

HSBC's research report further emphasizes that the macroeconomic drivers supporting the dollar's strength in 2022 no longer exist. In the first half of 2025, the market's confidence in US assets will be severely damaged by the Trump administration's repeated "Liberation Day" tariff policies, resulting in the dollar index recording its worst half-year performance in half a century, with a full-year decline of nearly 10% , marking the official end of a 15-year dollar bull market cycle. The current rebound is more of a short-term phenomenon driven by geopolitics; once the situation in the Middle East eases, structural weakness will once again dominate the dollar's trajectory.

Overall, the current rebound in the US dollar index is mainly driven by geopolitics and energy prices. HSBC confirms its safe-haven status remains unchanged, but both AJ Bell and Arbuthnot Latham emphasize that structural problems (policy uncertainty, fiscal deficits, and pressure on central bank independence) remain unresolved, making the rebound fragile. Once there are signs of easing tensions in the Middle East, the dollar may return to a depreciation trend. Investors need to be wary of the gap between short-term strength and long-term weakness, and closely monitor the progress of the conflict, oil price trends, and US fiscal/policy developments.

Editor's Summary:

The Middle East conflict and soaring oil prices have temporarily reshaped the dollar's safe-haven appeal, pushing the dollar index near a 10-month high, with HSBC confirming its continued leading position. However, both AJ Bell and Arbuthnot Latham warned that unresolved structural issues such as policy uncertainty, fiscal deficits, and central bank independence have led to a high dollar valuation and questionable sustainability of the rebound. Once geopolitical tensions ease, depreciation pressures will once again dominate.

Frequently Asked Questions

1. Why did the Middle East conflict and soaring oil prices drive a rapid rebound in the US dollar index?

Crude oil is priced in US dollars, and rising oil prices (WTI around $ 100.20 /barrel, Brent around $ 103.50 /barrel) directly increase global demand for the dollar. Simultaneously, geopolitical tensions boost risk aversion, leading to capital inflows into dollar assets. HSBC analysts point out that this rebound reaffirms the dollar's status as the primary safe-haven currency. The US, as a net energy exporter, further benefits from rising oil prices, while currencies of energy-import-dependent economies such as Europe face significant pressure.

2. The US dollar index is currently approaching a 10-month high, but why do many institutions believe that the rebound is unlikely to last?

AJ Bell's Chief Investment Officer, Russ Molde, emphasized that the structural problems leading to a significant weakening of the US dollar in 2025 remain: a lack of policy consistency in the US government, a continuing widening fiscal deficit, and political interference affecting the independence of the Federal Reserve. These characteristics are causing investors to worry about the long-term stability of the US economy. Arbuthnot Latham also pointed out that the dollar is currently overvalued, and once the situation in the Middle East eases and safe-haven demand subsides, the pressure for a valuation correction will be released rapidly.

3. What are the specific mechanisms by which the United States benefits from rising oil prices?

The United States has become a net exporter of crude oil, making it highly resilient to the risk of supply disruptions through the Strait of Hormuz. Rising oil prices increase oil export revenues, while the fact that global oil transactions are settled in US dollars further boosts demand for the dollar. Unlike Europe, the negative impact of rising domestic energy costs in the United States on inflation and growth is relatively manageable, making the dollar more resilient in conflict environments.

4. Why did the US dollar experience a historic period of weakness?

In the first half of 2025, the Trump administration's announcement and subsequent rapid withdrawal of "Liberation Day" tariffs led to a sharp decline in market confidence in US assets, resulting in the worst half-year performance for the US dollar index in over half a century, with a full-year drop of nearly 10% . Morgan Stanley and other institutions confirmed that this marks the end of a 15-year bull market for the US dollar. The current rebound is more of a short-term, geopolitically driven phenomenon than a fundamental improvement.

5. What are the key points to watch for in the future trend of the US dollar?

In the short term, the outlook depends on the evolution of the Middle East conflict: if tensions persist, safe-haven demand for the dollar and support from oil prices could push the dollar index further above 101.5 ; if the situation eases rapidly, the safe-haven premium will subside, and the dollar will face a valuation correction. In the long term, the outlook depends on whether the structural problems within the US worsen—whether the fiscal deficit spirals out of control, whether political intervention in the Federal Reserve intensifies, and whether policy uncertainty persists. Investors should simultaneously monitor oil prices, the progress of the conflict, US fiscal data, and the Federal Reserve's statements to determine whether the rebound will become sustainable or whether it will return to a depreciation trend.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.