Iran only needs to wait in a protracted war of high interest rates; the US can only endure it.

2026-03-25 16:15:16

The surge in gasoline prices triggered by the geopolitical conflict in Iran is creating a chain reaction that impacts everything from energy to inflation, from interest rates to people's livelihoods. This is not only pushing up the cost of living for American residents, but also driving up long-term interest rates and increasing mortgage and corporate credit costs.

The expectation that the Federal Reserve would continue its nearly two-year rate cuts has completely cooled, which has led to a rapid revaluation of asset prices recently.

This energy shock has plunged major central banks around the world into a stagflation policy dilemma, where they must guard against runaway inflation while also being wary of economic growth being dragged down by high oil prices, bringing monetary policy to a critical turning point.

Since the outbreak of the conflict in Iran on February 28, the effects of rising energy prices have been rapidly transmitted to the financial markets and the real economy.

Long-term interest rates rose rapidly in response, with the 10-year Treasury yield climbing from nearly 4% the day before the conflict to nearly 4.4%, directly pushing up financing costs for mortgages, auto loans, and corporate credit.

According to Freddie Mac data, the average interest rate for a 30-year fixed mortgage in the United States has risen to 6.22%, a significant increase from less than 6% before the conflict, putting considerable financial pressure on residents to buy homes, consume, and expand their businesses.

At the same time, oil prices have pushed up prices across the entire industrial chain, including transportation, chemicals, and consumer goods, leading to a new rebound in US inflation indicators.

UBS estimates that, based on the Federal Reserve's core inflation indicator, the inflation rate will jump to 3.4% this month and fall back to 3% by the end of the year, both well above the policy target of 2%.

Inflation has deviated from the target for five consecutive years. Coupled with the current energy shock, the pressure of rising prices has spread further to all aspects of people's lives, and people's economic confidence continues to be undermined.

For the past two years, the Federal Reserve's policy discussions have revolved around interest rate cuts, with the market focusing on the timing, magnitude, and frequency of such cuts. However, the energy inflation shock brought about by the conflict in Iran has completely reversed this narrative, leading to a dramatic reversal in market expectations.

In simpler terms, we previously knew that facing geopolitical risks, gold prices would stagnate due to a decrease in the probability of interest rate cuts and an increase in interest rates. However, the market is now telling us that not only will prices not rise, but they may even fall, or even plummet. Technology stocks are in a similar situation. At the same time, oil prices may change from short-term fluctuations to long-term high prices.

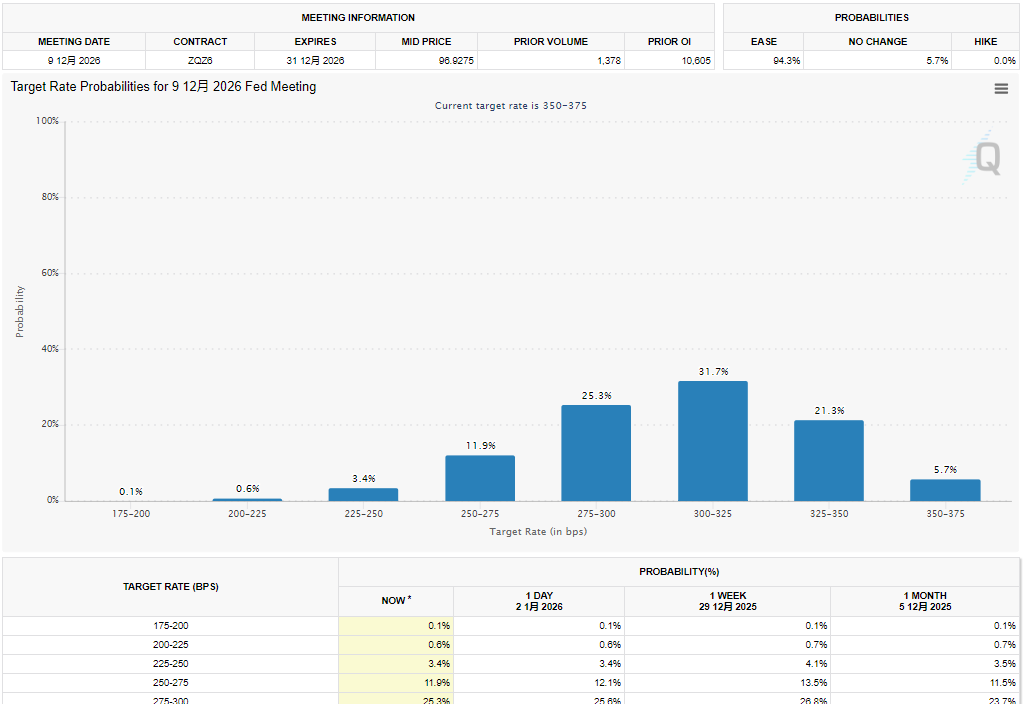

Data from the CME FedWatch Tool shows that as of Tuesday morning, Wall Street investors have completely abandoned their expectations of a Fed rate cut this year, with the probability of a higher policy rate at the end of the year reaching 26%, compared to zero a week ago.

The probability of a Fed rate hike before October is approaching 25%, turning what was considered "nonsense" at the beginning of the year into a real possibility.

(Interest rate futures up to the end of 2026 before the war, source: CME Group)

(Current interest rate futures as of the end of 2026, source: CME Group)

The yield on two-year U.S. Treasury bonds rose to 3.9%, breaking through the Federal Reserve's policy rate range of 3.5%-3.75%, confirming that the market has begun to price in expectations of rising interest rates in the coming years. This also reflects investors' concerns about the Federal Reserve's credibility in combating inflation.

The stagflationary pressures brought about by oil prices have put the Federal Reserve in an unprecedented policy dilemma.

On the one hand, persistent inflation coupled with energy shocks could cause inflation expectations to derail if prices are allowed to rise unchecked, and the Federal Reserve would need to curb inflation by raising interest rates or maintaining high interest rates.

On the other hand, if oil prices remain high for an extended period, it will squeeze residents' disposable income, forcing consumers to cut other spending, which in turn will drag down economic growth and push up the unemployment rate. At this time, interest rate cuts will exacerbate the risk of inflation.

Federal Reserve officials are divided and cautious on the matter. Chicago Fed President Gusby said that if inflation picks up, the unemployment rate remains stable, and inflation expectations rise, raising interest rates must be included in the policy options. He also mentioned that there is room for policy in both directions, and that interest rates can still be cut if inflation improves. Fed Chairman Powell made it clear that raising interest rates is not the baseline scenario expected by most officials.

San Francisco Fed President Daly stated that given the geopolitical uncertainty, there is no single, certain trend in interest rates; there are three possibilities: an increase, a decrease, or no change.

Furthermore, the Trump administration's continued pressure on the Federal Reserve to cut interest rates has further eroded the central bank's policy independence, making the Fed's decision-making more constrained.

From the perspective of the central bank's policy framework, under normal circumstances, energy price shocks are mostly one-off price adjustments and will inhibit economic growth. Monetary policy should downplay such disturbances and there is no need to tighten excessively.

However, exceptions to this principle are the risk of inflation expectations becoming unanchored and the full transmission of energy price increases to core prices, which is precisely the current dilemma facing the Federal Reserve.

Historical lessons have also served as a warning to central banks around the world. In the spring and summer of 2008, with a weakening economy and soaring oil prices, then-European Central Bank President Trichet raised interest rates twice, which was later proven to be a major decision-making error, leading the Eurozone into a more passive position in the subsequent financial crisis.

The current situation is highly similar to that of 2008. Regardless of whether it is Federal Reserve Chairman Powell or Trump's nominee Warsh, the feasibility of raising interest rates has extremely low given the weak job market, suppressed consumption, and tightening financial conditions. Therefore, the Federal Reserve still only has two options: cut interest rates or keep interest rates unchanged.

Warsh is the president's handpicked strategist for interest rate cuts, but he has been unable to pass the committee's review. Senior Democratic Senator Elizabeth Warren criticized him for "being more concerned with Wall Street interests and ignoring ordinary people's jobs," and believed that his nomination was "a step by Trump to try to control the Federal Reserve," further exacerbating the resistance to his nomination.

Looking globally, the European Central Bank and the Bank of England, among others, have also fallen into stagflation. They have maintained their interest rates unchanged and released cautious signals, refraining from raising or lowering rates for the time being. They are closely monitoring oil price transmission and inflation data to make dynamic decisions in order to avoid repeating the policy mistakes of 2008.

Mainstream institutions are reaching a consensus on the Federal Reserve's policy path, believing that interest rate cuts are more likely to be postponed rather than canceled, and that interest rate hikes will require meeting stringent conditions.

Evercore ISI chief economist Guha pointed out that the rate cut is only postponed to September, December or even 2027, rather than being completely shelved; UBS economist Pingel believes that higher inflation corresponds to higher interest rates, but energy shocks will also hinder economic growth, making it difficult for the Federal Reserve to take aggressive action.

In summary, the most feasible policy path for the Federal Reserve is to maintain the key interest rate unchanged, wage a "protracted war of high interest rates," and then cut rates when the opportunity arises. This is the Achilles' heel of the US's protracted war.

For ordinary people, the pressure of high borrowing costs and rising prices will continue, which will lead to a decline in economic vitality. The United States is particularly disadvantaged in the face of a protracted war with massive debt, high borrowing costs, and a potentially deteriorating job market, which makes it difficult to lower interest rates. Therefore, Iran is unwilling to talk to the United States. High domestic price increases and government borrowing costs will naturally hinder US military operations. What Iran needs to do is control costs and fight a long-term war of attrition.

The expectation that the Federal Reserve would continue its nearly two-year rate cuts has completely cooled, which has led to a rapid revaluation of asset prices recently.

This energy shock has plunged major central banks around the world into a stagflation policy dilemma, where they must guard against runaway inflation while also being wary of economic growth being dragged down by high oil prices, bringing monetary policy to a critical turning point.

Oil price shock transmission: Inflation rises, interest rates and borrowing costs increase across the board.

Since the outbreak of the conflict in Iran on February 28, the effects of rising energy prices have been rapidly transmitted to the financial markets and the real economy.

Long-term interest rates rose rapidly in response, with the 10-year Treasury yield climbing from nearly 4% the day before the conflict to nearly 4.4%, directly pushing up financing costs for mortgages, auto loans, and corporate credit.

According to Freddie Mac data, the average interest rate for a 30-year fixed mortgage in the United States has risen to 6.22%, a significant increase from less than 6% before the conflict, putting considerable financial pressure on residents to buy homes, consume, and expand their businesses.

At the same time, oil prices have pushed up prices across the entire industrial chain, including transportation, chemicals, and consumer goods, leading to a new rebound in US inflation indicators.

UBS estimates that, based on the Federal Reserve's core inflation indicator, the inflation rate will jump to 3.4% this month and fall back to 3% by the end of the year, both well above the policy target of 2%.

Inflation has deviated from the target for five consecutive years. Coupled with the current energy shock, the pressure of rising prices has spread further to all aspects of people's lives, and people's economic confidence continues to be undermined.

Market expectations reverse: from heated discussions about interest rate cuts to a sharp increase in the probability of interest rate hikes.

For the past two years, the Federal Reserve's policy discussions have revolved around interest rate cuts, with the market focusing on the timing, magnitude, and frequency of such cuts. However, the energy inflation shock brought about by the conflict in Iran has completely reversed this narrative, leading to a dramatic reversal in market expectations.

In simpler terms, we previously knew that facing geopolitical risks, gold prices would stagnate due to a decrease in the probability of interest rate cuts and an increase in interest rates. However, the market is now telling us that not only will prices not rise, but they may even fall, or even plummet. Technology stocks are in a similar situation. At the same time, oil prices may change from short-term fluctuations to long-term high prices.

Data from the CME FedWatch Tool shows that as of Tuesday morning, Wall Street investors have completely abandoned their expectations of a Fed rate cut this year, with the probability of a higher policy rate at the end of the year reaching 26%, compared to zero a week ago.

The probability of a Fed rate hike before October is approaching 25%, turning what was considered "nonsense" at the beginning of the year into a real possibility.

(Interest rate futures up to the end of 2026 before the war, source: CME Group)

(Current interest rate futures as of the end of 2026, source: CME Group)

The yield on two-year U.S. Treasury bonds rose to 3.9%, breaking through the Federal Reserve's policy rate range of 3.5%-3.75%, confirming that the market has begun to price in expectations of rising interest rates in the coming years. This also reflects investors' concerns about the Federal Reserve's credibility in combating inflation.

The Federal Reserve's core dilemma: the difficult balance between fighting inflation and stabilizing growth.

The stagflationary pressures brought about by oil prices have put the Federal Reserve in an unprecedented policy dilemma.

On the one hand, persistent inflation coupled with energy shocks could cause inflation expectations to derail if prices are allowed to rise unchecked, and the Federal Reserve would need to curb inflation by raising interest rates or maintaining high interest rates.

On the other hand, if oil prices remain high for an extended period, it will squeeze residents' disposable income, forcing consumers to cut other spending, which in turn will drag down economic growth and push up the unemployment rate. At this time, interest rate cuts will exacerbate the risk of inflation.

Federal Reserve officials are divided and cautious on the matter. Chicago Fed President Gusby said that if inflation picks up, the unemployment rate remains stable, and inflation expectations rise, raising interest rates must be included in the policy options. He also mentioned that there is room for policy in both directions, and that interest rates can still be cut if inflation improves. Fed Chairman Powell made it clear that raising interest rates is not the baseline scenario expected by most officials.

San Francisco Fed President Daly stated that given the geopolitical uncertainty, there is no single, certain trend in interest rates; there are three possibilities: an increase, a decrease, or no change.

Furthermore, the Trump administration's continued pressure on the Federal Reserve to cut interest rates has further eroded the central bank's policy independence, making the Fed's decision-making more constrained.

The central bank's response logic and historical lessons

From the perspective of the central bank's policy framework, under normal circumstances, energy price shocks are mostly one-off price adjustments and will inhibit economic growth. Monetary policy should downplay such disturbances and there is no need to tighten excessively.

However, exceptions to this principle are the risk of inflation expectations becoming unanchored and the full transmission of energy price increases to core prices, which is precisely the current dilemma facing the Federal Reserve.

Historical lessons have also served as a warning to central banks around the world. In the spring and summer of 2008, with a weakening economy and soaring oil prices, then-European Central Bank President Trichet raised interest rates twice, which was later proven to be a major decision-making error, leading the Eurozone into a more passive position in the subsequent financial crisis.

The current situation is highly similar to that of 2008. Regardless of whether it is Federal Reserve Chairman Powell or Trump's nominee Warsh, the feasibility of raising interest rates has extremely low given the weak job market, suppressed consumption, and tightening financial conditions. Therefore, the Federal Reserve still only has two options: cut interest rates or keep interest rates unchanged.

Warsh is the president's handpicked strategist for interest rate cuts, but he has been unable to pass the committee's review. Senior Democratic Senator Elizabeth Warren criticized him for "being more concerned with Wall Street interests and ignoring ordinary people's jobs," and believed that his nomination was "a step by Trump to try to control the Federal Reserve," further exacerbating the resistance to his nomination.

Looking globally, the European Central Bank and the Bank of England, among others, have also fallen into stagflation. They have maintained their interest rates unchanged and released cautious signals, refraining from raising or lowering rates for the time being. They are closely monitoring oil price transmission and inflation data to make dynamic decisions in order to avoid repeating the policy mistakes of 2008.

Institutional Views and Actual Policy Trends

Mainstream institutions are reaching a consensus on the Federal Reserve's policy path, believing that interest rate cuts are more likely to be postponed rather than canceled, and that interest rate hikes will require meeting stringent conditions.

Evercore ISI chief economist Guha pointed out that the rate cut is only postponed to September, December or even 2027, rather than being completely shelved; UBS economist Pingel believes that higher inflation corresponds to higher interest rates, but energy shocks will also hinder economic growth, making it difficult for the Federal Reserve to take aggressive action.

In summary, the most feasible policy path for the Federal Reserve is to maintain the key interest rate unchanged, wage a "protracted war of high interest rates," and then cut rates when the opportunity arises. This is the Achilles' heel of the US's protracted war.

For ordinary people, the pressure of high borrowing costs and rising prices will continue, which will lead to a decline in economic vitality. The United States is particularly disadvantaged in the face of a protracted war with massive debt, high borrowing costs, and a potentially deteriorating job market, which makes it difficult to lower interest rates. Therefore, Iran is unwilling to talk to the United States. High domestic price increases and government borrowing costs will naturally hinder US military operations. What Iran needs to do is control costs and fight a long-term war of attrition.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.