A chart shows that the Baltic Dry Index rose for the third consecutive trading day, with Capesize freight rates hitting a three-week high.

2026-03-28 01:15:45

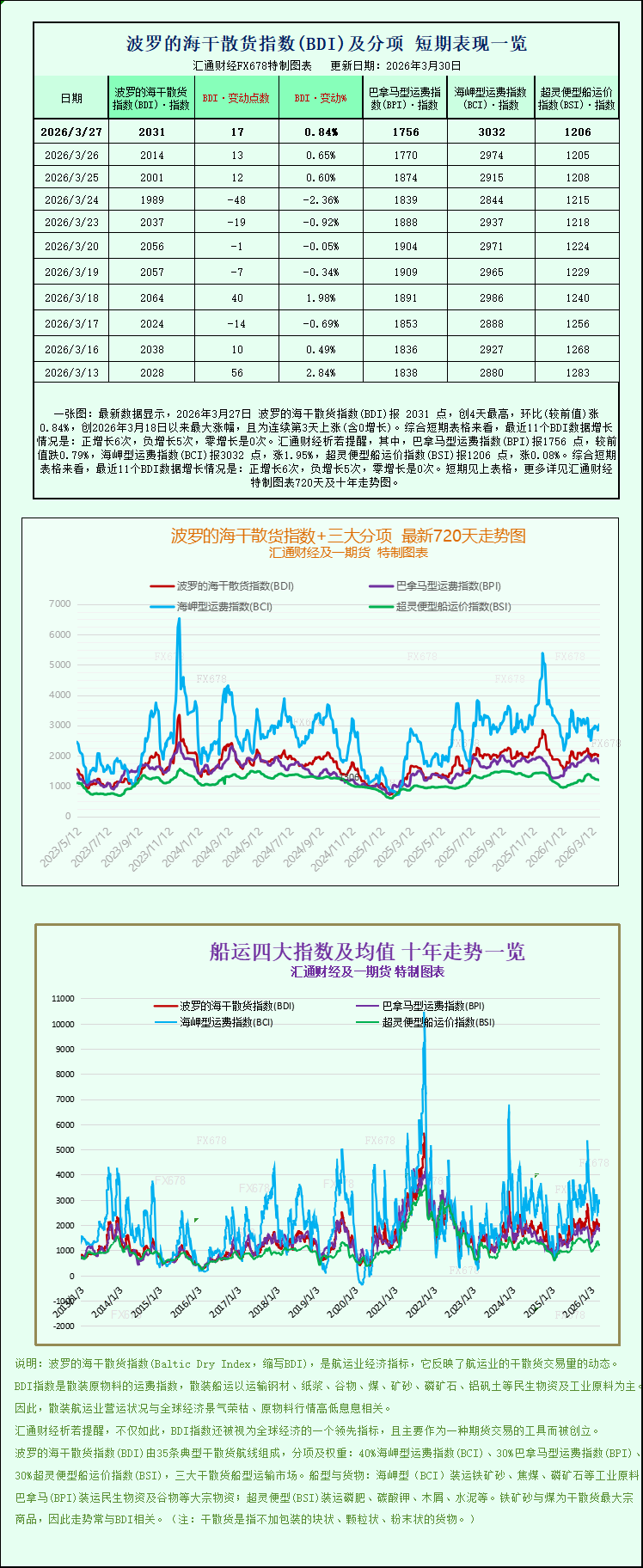

Latest data shows that the Baltic Dry Index (BDI) reached 2031 points on March 27, 2026, a four-day high, up 0.84% month-on-month (compared to the previous value), marking the largest increase since March 18, 2026, and the third consecutive day of increase (including zero growth). Looking at the short-term charts, the recent 11 BDI data points show: 6 positive increases, 5 negative increases, and 0 zero increases. Specifically, the Panamax Freight Index (BPI) was 1756 points, down 0.79% from the previous value; the Capesize Freight Index (BCI) was 3032 points, up 1.95%; and the Supramax Freight Index (BSI) was 1206 points, up 0.08%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI), which monitors freight rates for dry bulk cargoes globally in real time and is a key indicator of the international dry bulk shipping market's health, continued its upward trend on Friday, marking its third consecutive day of gains. Freight rates for Capesize vessels, a core vessel type, were particularly strong, surging to their highest level in over three weeks and becoming a key driver of the overall index's rise.

As a core indicator comprehensively tracking freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—the main Baltic Dry Index rose 17 points, or 0.8%, to close at 2031 points. It's worth noting that despite the slight increase on the day, the index still showed an overall downward trend this week, with a cumulative decline of 1.2%, influenced by a mix of bullish and bearish factors, indicating that the dry bulk shipping market is currently still in a period of fluctuation and adjustment.

Looking at specific ship types, the Capesize index performed strongly, rising 58 points, or approximately 2%, to close at 3032 points. This figure represents the highest level since March 4th, ending a period of volatile and sluggish trading. Capesize bulk carriers, as the "juggernauts" of the dry bulk shipping market, primarily undertake the transportation of large-scale industrial raw materials between continents. They typically carry 150,000 tons of cargo, with core commodities including key raw materials supporting global industrial production such as iron ore and coal. Changes in their freight rates directly reflect the state of global industrial demand.

Along with the improved Capesize index, profitability also improved. On that day, the average daily revenue of Capesize bulk carriers rose by $523, eventually reaching $23,994, also a new high in more than three weeks. This change also confirms the recovery in market demand for this type of vessel, and shipowners' profitability has been significantly improved.

Meanwhile, the commodity market saw a coordinated adjustment, with iron ore futures prices falling on Friday. The core reason behind this was that after the passage of Tropical Cyclone Narrat, which had garnered significant market attention, investigations revealed no substantial impact on critical port infrastructure in Western Australia. The Pilbara region of Western Australia, home to several key iron ore export ports, is a crucial hub for global iron ore supply. Historically, there have been instances where tropical cyclones have caused port closures and supply disruptions. Consequently, some traders had preemptively placed positions bets on supply disruptions. After confirming the port safety, these traders closed their positions, leading to a decline in iron ore futures prices.

In stark contrast to the strong performance of Capesize vessels, the Panamax index weakened on the day, falling 14 points, or 0.8%, to close at 1756 points, a six-week low, reflecting continued sluggish demand for this vessel type. Panamax vessels are of moderate tonnage, typically carrying 60,000 to 70,000 tons of cargo. Their core transport categories are essential consumer goods such as coal and grain, as well as industrial auxiliary materials. Their freight rates are closely linked to global food trade and electricity demand.

Affected by the decline in the index, the average daily revenue of Panamax vessels also fell, decreasing by $131 to $15,800, further squeezing shipowners' profit margins. Industry analysts believe that the sluggishness of the Panamax market is related to factors such as the slowdown in food trade in some parts of the world, a temporary weakness in coal demand, and the excessively rapid growth in fleet supply.

Among the three major ship types, the Supramax ship index performed relatively steadily, rising only 1 point on the day, an increase of 0.1%, closing at 1206 points. The overall fluctuation range was small, indicating that the supply and demand in the corresponding segment of the freight market for this ship type is in a relatively balanced state, and there is no obvious imbalance between bulls and bears.

Geopolitically, the situation in the Middle East continues to affect the global shipping market. After Tehran, Iran, explicitly rejected US President Trump's 15-point proposal aimed at ending the war between Iran and Israel, the Trump administration adjusted its previous hardline stance, extending the deadline for Iran to reopen the Strait of Hormuz by 10 days. It also issued a clear warning that if Iran does not cooperate within the extended period, its energy plants risk being destroyed. It is understood that Trump has previously adjusted deadlines multiple times, and this extension is interpreted by the market as indicating that there is still room for negotiation between the two sides.

The war between the United States and Israel against Iran, which began on February 28, has significantly impacted global shipping and energy markets. The Strait of Hormuz, a vital chokepoint for global energy transport, connects the Persian Gulf and the Gulf of Oman and is the only sea route for crude oil exports from Middle Eastern oil-producing countries. Approximately 20% of global oil shipments pass through this strait. Since the outbreak of the war, the strait has been effectively blocked, directly disrupting the normal flow of global oil supplies and driving up global shipping and freight prices dramatically. Currently, major global shipping giants have suspended routes through the strait, with some vessels opting to detour around the Cape of Good Hope in Africa, leading to longer voyages, soaring transportation costs, and further exacerbating volatility in the global shipping market.

The Baltic Dry Index (BDI), which monitors freight rates for dry bulk cargoes globally in real time and is a key indicator of the international dry bulk shipping market's health, continued its upward trend on Friday, marking its third consecutive day of gains. Freight rates for Capesize vessels, a core vessel type, were particularly strong, surging to their highest level in over three weeks and becoming a key driver of the overall index's rise.

As a core indicator comprehensively tracking freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—the main Baltic Dry Index rose 17 points, or 0.8%, to close at 2031 points. It's worth noting that despite the slight increase on the day, the index still showed an overall downward trend this week, with a cumulative decline of 1.2%, influenced by a mix of bullish and bearish factors, indicating that the dry bulk shipping market is currently still in a period of fluctuation and adjustment.

Looking at specific ship types, the Capesize index performed strongly, rising 58 points, or approximately 2%, to close at 3032 points. This figure represents the highest level since March 4th, ending a period of volatile and sluggish trading. Capesize bulk carriers, as the "juggernauts" of the dry bulk shipping market, primarily undertake the transportation of large-scale industrial raw materials between continents. They typically carry 150,000 tons of cargo, with core commodities including key raw materials supporting global industrial production such as iron ore and coal. Changes in their freight rates directly reflect the state of global industrial demand.

Along with the improved Capesize index, profitability also improved. On that day, the average daily revenue of Capesize bulk carriers rose by $523, eventually reaching $23,994, also a new high in more than three weeks. This change also confirms the recovery in market demand for this type of vessel, and shipowners' profitability has been significantly improved.

Meanwhile, the commodity market saw a coordinated adjustment, with iron ore futures prices falling on Friday. The core reason behind this was that after the passage of Tropical Cyclone Narrat, which had garnered significant market attention, investigations revealed no substantial impact on critical port infrastructure in Western Australia. The Pilbara region of Western Australia, home to several key iron ore export ports, is a crucial hub for global iron ore supply. Historically, there have been instances where tropical cyclones have caused port closures and supply disruptions. Consequently, some traders had preemptively placed positions bets on supply disruptions. After confirming the port safety, these traders closed their positions, leading to a decline in iron ore futures prices.

In stark contrast to the strong performance of Capesize vessels, the Panamax index weakened on the day, falling 14 points, or 0.8%, to close at 1756 points, a six-week low, reflecting continued sluggish demand for this vessel type. Panamax vessels are of moderate tonnage, typically carrying 60,000 to 70,000 tons of cargo. Their core transport categories are essential consumer goods such as coal and grain, as well as industrial auxiliary materials. Their freight rates are closely linked to global food trade and electricity demand.

Affected by the decline in the index, the average daily revenue of Panamax vessels also fell, decreasing by $131 to $15,800, further squeezing shipowners' profit margins. Industry analysts believe that the sluggishness of the Panamax market is related to factors such as the slowdown in food trade in some parts of the world, a temporary weakness in coal demand, and the excessively rapid growth in fleet supply.

Among the three major ship types, the Supramax ship index performed relatively steadily, rising only 1 point on the day, an increase of 0.1%, closing at 1206 points. The overall fluctuation range was small, indicating that the supply and demand in the corresponding segment of the freight market for this ship type is in a relatively balanced state, and there is no obvious imbalance between bulls and bears.

Geopolitically, the situation in the Middle East continues to affect the global shipping market. After Tehran, Iran, explicitly rejected US President Trump's 15-point proposal aimed at ending the war between Iran and Israel, the Trump administration adjusted its previous hardline stance, extending the deadline for Iran to reopen the Strait of Hormuz by 10 days. It also issued a clear warning that if Iran does not cooperate within the extended period, its energy plants risk being destroyed. It is understood that Trump has previously adjusted deadlines multiple times, and this extension is interpreted by the market as indicating that there is still room for negotiation between the two sides.

The war between the United States and Israel against Iran, which began on February 28, has significantly impacted global shipping and energy markets. The Strait of Hormuz, a vital chokepoint for global energy transport, connects the Persian Gulf and the Gulf of Oman and is the only sea route for crude oil exports from Middle Eastern oil-producing countries. Approximately 20% of global oil shipments pass through this strait. Since the outbreak of the war, the strait has been effectively blocked, directly disrupting the normal flow of global oil supplies and driving up global shipping and freight prices dramatically. Currently, major global shipping giants have suspended routes through the strait, with some vessels opting to detour around the Cape of Good Hope in Africa, leading to longer voyages, soaring transportation costs, and further exacerbating volatility in the global shipping market.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.