Strong oil prices are driving structural inflation, and the expectation of a Fed rate cut in 2026 has been completely ruled out?

2026-04-07 16:58:08

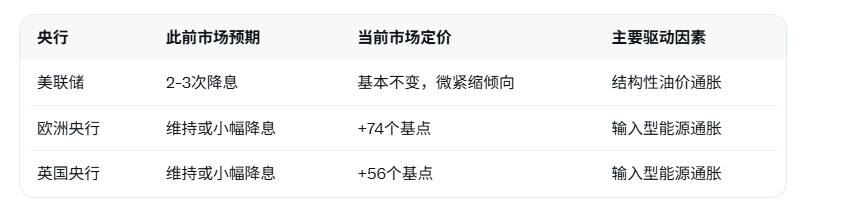

According to APP, analysts at First Abu Dhabi Bank stated in their latest report that the strength of oil prices has been and will continue to be (at least in the short term) a more structural driver of inflationary pressures. The analysts pointed out that inflationary pressures have led to a sell-off in interest rates as expectations of central bank rate cuts have faded. Previously, the market widely expected the Federal Reserve to cut rates two to three times this year, but these expectations have been completely ruled out. According to the latest data from the financial data platform LSEG, the money market currently expects US policy rates to remain largely unchanged in 2026, with a very slight tightening tendency. The market has even priced in a more hawkish rate hike scenario by the European Central Bank and the Bank of England by the end of this year, with increases of 74 basis points and 56 basis points respectively, "largely a result of imported energy inflation in Europe."

The current high oil prices have become a core variable in the global macroeconomic environment. Geopolitical conflicts in the Middle East have significantly increased uncertainty in energy supply, with Brent crude oil prices breaking through the $100 per barrel mark and maintaining their strength. This price level not only directly pushes up energy inflation but also transmits to core inflation through multiple channels, including production costs, logistics expenses, and consumer expectations, creating more persistent structural pressure. Unlike previous temporary supply shocks, this round of oil price increases is accompanied by long-term geopolitical risks, making it difficult for central banks to simply view it as a "one-off" factor, thus forcing a shift in monetary policy.

The Federal Reserve's initial easing expectations have completely reversed. At the end of 2025, the market priced in 2-3 rate cuts for the year, but current futures markets indicate that the probability of rate cuts throughout 2026 is close to zero, with a slight tightening tendency emerging instead. This reflects investors' concerns about the persistence of inflation: every $10/barrel increase in oil prices could potentially push up overall US inflation by 0.3-0.5 percentage points, amplifying through the supply chain to the service and wage sectors. This has led to a steepening of the bond yield curve, with rising long-term interest rates further suppressing interest rate-sensitive assets such as stocks and real estate.

The European Central Bank (ECB) and the Bank of England (BOE) face more direct imported inflationary pressures. Europe is highly dependent on external energy imports, and rising oil prices directly translate into higher import costs and production expenses for businesses. The market has already priced in a 74-basis-point increase in the ECB's deposit facility rate and a 56-basis-point increase in the BOE's benchmark interest rate by the end of 2026. This hawkish pricing far exceeds the easing expectations at the beginning of the year, highlighting the significant reshaping of the inflation path in the Eurozone and the UK by the energy crisis.

To visually illustrate the shift in policy expectations of major central banks, the following table compares previous market consensus with the current pricing scenario:

The core of this shift lies in the evolution of oil prices from a cyclical variable to a structural one. Investors need to continuously monitor actual energy price trends and the latest central bank inflation forecasts to dynamically adjust their asset allocation.

Editor's Summary : Strong oil prices are reshaping the global monetary policy framework. First Abu Dhabi Bank 's analysis clearly reveals the profound impact of the shift in inflation drivers from temporary to persistent factors on central bank decisions. The pricing adjustments by the Federal Reserve, the European Central Bank, and the Bank of England all reflect the central role of energy security in macroeconomic stability. Ultimately, the interest rate path will depend on the evolution of the Middle East situation, the actual duration of oil price increases, and the verification of inflation data in various countries. Market participants should maintain flexible risk management anchored to data.

The current high oil prices have become a core variable in the global macroeconomic environment. Geopolitical conflicts in the Middle East have significantly increased uncertainty in energy supply, with Brent crude oil prices breaking through the $100 per barrel mark and maintaining their strength. This price level not only directly pushes up energy inflation but also transmits to core inflation through multiple channels, including production costs, logistics expenses, and consumer expectations, creating more persistent structural pressure. Unlike previous temporary supply shocks, this round of oil price increases is accompanied by long-term geopolitical risks, making it difficult for central banks to simply view it as a "one-off" factor, thus forcing a shift in monetary policy.

The Federal Reserve's initial easing expectations have completely reversed. At the end of 2025, the market priced in 2-3 rate cuts for the year, but current futures markets indicate that the probability of rate cuts throughout 2026 is close to zero, with a slight tightening tendency emerging instead. This reflects investors' concerns about the persistence of inflation: every $10/barrel increase in oil prices could potentially push up overall US inflation by 0.3-0.5 percentage points, amplifying through the supply chain to the service and wage sectors. This has led to a steepening of the bond yield curve, with rising long-term interest rates further suppressing interest rate-sensitive assets such as stocks and real estate.

The European Central Bank (ECB) and the Bank of England (BOE) face more direct imported inflationary pressures. Europe is highly dependent on external energy imports, and rising oil prices directly translate into higher import costs and production expenses for businesses. The market has already priced in a 74-basis-point increase in the ECB's deposit facility rate and a 56-basis-point increase in the BOE's benchmark interest rate by the end of 2026. This hawkish pricing far exceeds the easing expectations at the beginning of the year, highlighting the significant reshaping of the inflation path in the Eurozone and the UK by the energy crisis.

To visually illustrate the shift in policy expectations of major central banks, the following table compares previous market consensus with the current pricing scenario:

The core of this shift lies in the evolution of oil prices from a cyclical variable to a structural one. Investors need to continuously monitor actual energy price trends and the latest central bank inflation forecasts to dynamically adjust their asset allocation.

Editor's Summary : Strong oil prices are reshaping the global monetary policy framework. First Abu Dhabi Bank 's analysis clearly reveals the profound impact of the shift in inflation drivers from temporary to persistent factors on central bank decisions. The pricing adjustments by the Federal Reserve, the European Central Bank, and the Bank of England all reflect the central role of energy security in macroeconomic stability. Ultimately, the interest rate path will depend on the evolution of the Middle East situation, the actual duration of oil price increases, and the verification of inflation data in various countries. Market participants should maintain flexible risk management anchored to data.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.