Balance sheet reduction does not represent tightening; the Federal Reserve's deeper strategy of forcing banks to "abandon reserves and buy Treasury bonds" is a strategic move.

2026-04-17 17:39:48

The Federal Reserve is determined to end the "easy money" model for American banks. Under the post-crisis regulatory framework, banks can simply deposit huge sums of money with the Federal Reserve as reserves to secure risk-free interest rates on outstanding reserves (IORB), without having to bear the risks of lending or optimize asset allocation efficiency. This "easy money" model has become a hidden danger in the financial system.

Banks' over-reliance on reserve income not only leads to funds circulating aimlessly within the financial system and reduces the efficiency of social capital allocation, but also weakens the transmission effect of monetary policy. When banks lack the incentive to actively lend and allocate assets, the impact of interest rate adjustments on the real economy will be greatly reduced.

More seriously, this model directly binds the interests of the Federal Reserve and the banking system, forcing the Federal Reserve to passively increase its holdings of Treasury bonds and expand its balance sheet in order to meet the banks' reserve requirements. In the long run, this will blur the boundaries between monetary and fiscal policies, gradually turning the Federal Reserve into a "guarantor" of fiscal financing and seriously threatening the independence of the central bank.

Once monetary policy is hijacked by fiscal needs, the Federal Reserve will find it difficult to formulate neutral policies based on core objectives such as inflation and employment, ultimately damaging the credibility of the dollar and the stability of the global financial system.

In the fourth quarter of last year, the Federal Reserve ended the latest round of quantitative tightening (QT) with a "quiet" operation, reducing its balance sheet by more than $2 trillion from a peak of nearly $9 trillion.

Unlike the 2019 QT, which was forced to halt due to the liquidity crisis, the smooth launch of QT this time confirms former Federal Reserve Chair Janet Yellen's expectation that it would be "like watching paint dry," and lays the foundation for subsequent policy implementation.

Today, Federal Reserve governors, academics, and former officials are calling for further reduction of the balance sheet, which reflects concerns about the "flattened mode" of banks and a deeper strategy to "force banks to transform, reduce their own burden of guaranteeing the market, and revitalize the Treasury bond market."

The core issue behind the Federal Reserve's insistence on continuing to shrink its balance sheet lies in banks' "excessive reliance" on reserves.

Post-crisis regulatory rules require banks to hold sufficient highly liquid reserves to cover deposit funding risks;

Meanwhile, banks' lending and credit business continues to create new deposits, which in turn further increases the demand for reserves.

To meet this demand, the Federal Reserve has had to passively increase its holdings of Treasury bonds and expand its balance sheet. This will not only distort the pricing of Treasury bonds and repurchase markets and weaken market liquidity, but also risk eroding the independence of the central bank.

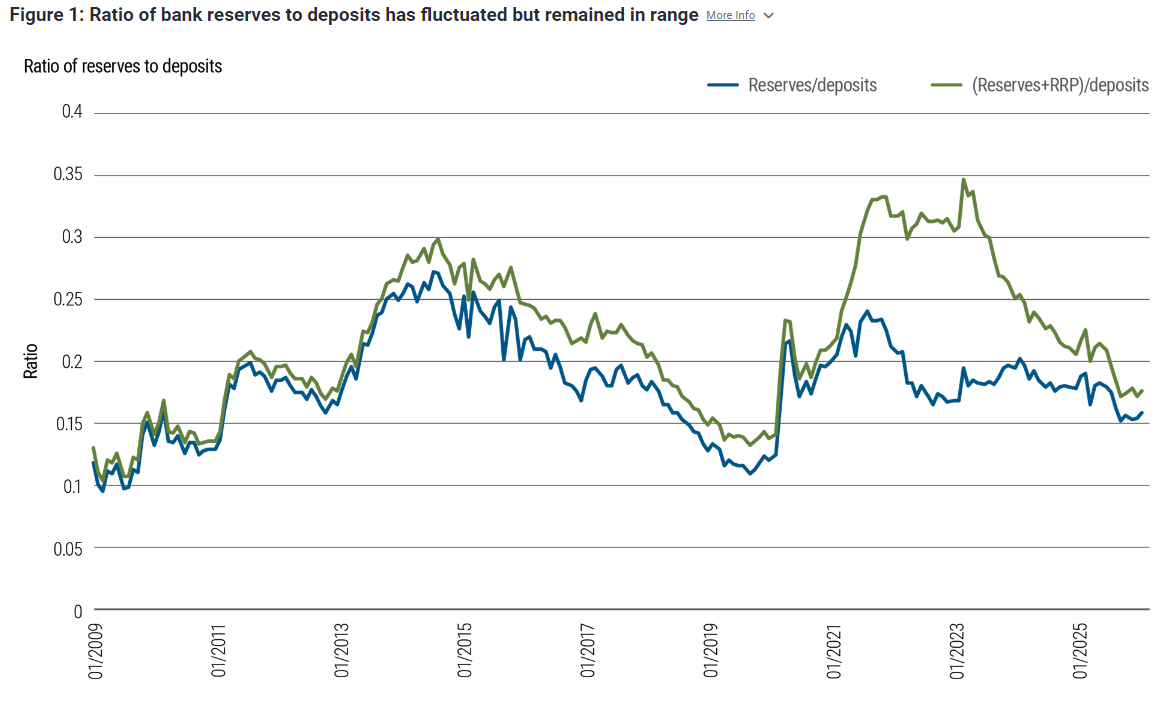

(Chart showing the ratio of bank reserves held at the Federal Reserve / total bank deposits to bank reserves + Federal Reserve reverse repos ÷ total deposits)

The chart shows that as long as bank deposits grow, banks' demand for reserves will increase accordingly. Without regulatory reform, the Federal Reserve will always be forced to passively expand its balance sheet and buy more Treasury bonds, which is the Fed's biggest headache.

To break this deadlock, the Federal Reserve's core idea is to reform policies so that banks no longer hoard large amounts of reserves and instead allocate highly liquid assets.

Among the series of proposals recently put forward by Federal Reserve economists, the most feasible is to optimize the regulatory rules for liquidity of large banks—allowing banks to use the discount window in extreme stress scenarios, while guiding them to replace some of their reserves with collateralizable assets such as Treasury bills and short-term agency bonds.

This reform not only removes the "stigma" of the use of central bank tools, but also allows banks to maintain a liquidity safety net while giving up the inertia of "earning interest passively";

For the Federal Reserve, this reduces the pressure of passively expanding its balance sheet, avoids having to bail out the market for an extended period, and thus maintains the independence and flexibility of monetary policy.

From a market impact perspective, this reform is essentially about creating new demand for the government bond market.

The current yield curve for government bonds is steepening, giving banks a strong incentive to replace low-yield reserves with high-yield government bonds.

In the past, the Federal Reserve was the main "buyer" of Treasury bonds, but in the future, banks are expected to become an important source of incremental funds for the Treasury bond market, which will not only revitalize the liquidity of the Treasury bond market, but also reduce the burden of the Federal Reserve's continuous bond purchases.

The Federal Reserve plans to assess the effectiveness of its policies by monitoring changes in the spread between money market rates and the IORB and by surveying the minimum comfortable reserve levels of large banks. It is expected that after confirming a decrease in reserve demand of at least $500 billion, it may continue the gradual quantitative easing (QT) in the second half of next year.

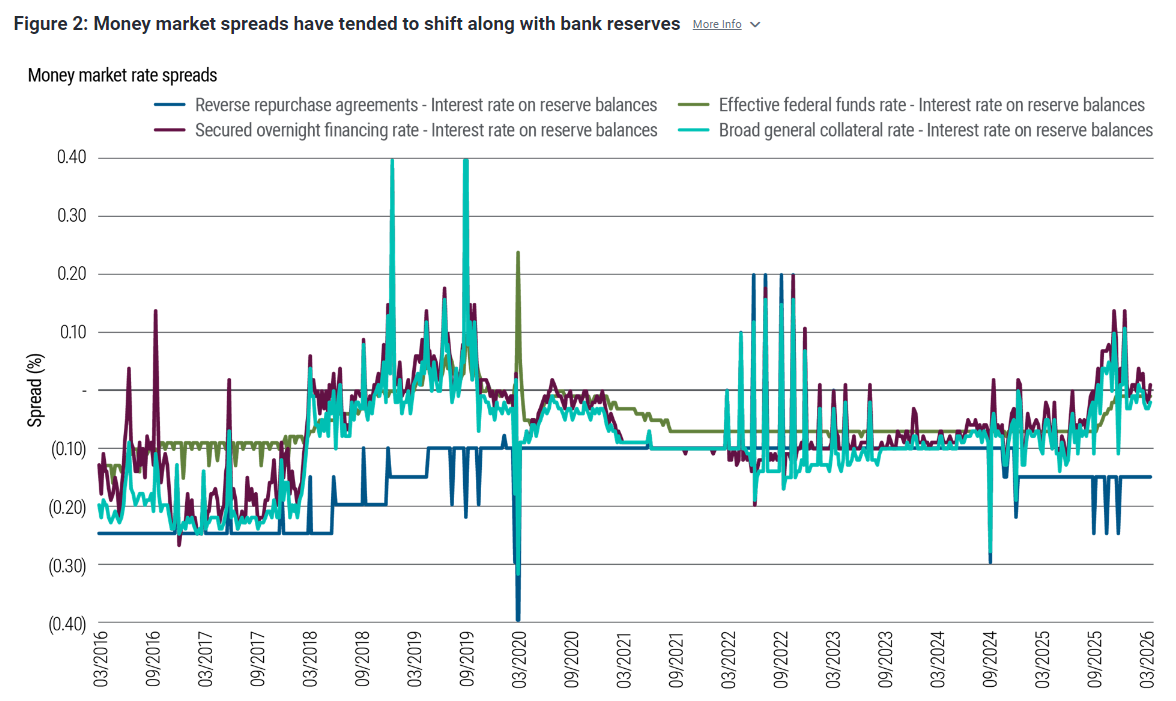

(Payouts between different money market interest rates and the Federal Reserve Reserve Balance Rate (IORB))

IORB is the risk-free return banks receive for depositing money with the Federal Reserve, while other money market rates are the returns banks receive for lending money to the market. The spread between these two rates directly reflects the supply and demand of liquidity in the market.

When reserves are "excessive" (e.g., 2016-2019, 2021-2023), money market rates fall below the IORB, with the blue and purple lines remaining below the zero axis for extended periods, even reaching as low as -0.2%. When reserves are "tightened" (e.g., mid-2019, 2022 to present), the interest rate spread approaches the zero axis, and may even exceed the IORB (e.g., the surge in repo rates in September 2019).

Overall, the Fed's resumption of balance sheet reduction is not simply a matter of "shrinking liquidity," but rather a systemic adjustment that balances "reducing excessive reserves, activating market liquidity, and maintaining the central bank's independence."

As the balance sheet returns to a more reasonable size, the Fed's policy space will be greatly expanded: On the one hand, freed from the constraints of passive balance sheet expansion, the Fed can more flexibly adjust the intensity of its policies according to inflation trends. If inflation stickiness exceeds expectations, the liquidity tightening brought about by balance sheet reduction, in conjunction with interest rate tools, can more accurately suppress inflationary pressures on the demand side.

On the other hand, when the economy faces downside risks, the previously contracted balance sheet has reserved ample room for a new round of quantitative easing and liquidity injection, avoiding the predicament of "running out of policy ammunition".

This ability to "manage and adjust at will" will allow the Federal Reserve to be more proactive in balancing the goals of inflation control and economic growth, thus safeguarding its core mission of price stability and laying a solid monetary and financial foundation for sustainable growth in the U.S. economy.

As banks shift from "sitting back and earning interest" to market-based asset allocation, they will improve the efficiency of the financial system, make monetary policy transmission smoother, and ultimately form a virtuous cycle of "effective central bank regulation, sufficient market vitality, and stable economic operation".

Banks' over-reliance on reserve income not only leads to funds circulating aimlessly within the financial system and reduces the efficiency of social capital allocation, but also weakens the transmission effect of monetary policy. When banks lack the incentive to actively lend and allocate assets, the impact of interest rate adjustments on the real economy will be greatly reduced.

More seriously, this model directly binds the interests of the Federal Reserve and the banking system, forcing the Federal Reserve to passively increase its holdings of Treasury bonds and expand its balance sheet in order to meet the banks' reserve requirements. In the long run, this will blur the boundaries between monetary and fiscal policies, gradually turning the Federal Reserve into a "guarantor" of fiscal financing and seriously threatening the independence of the central bank.

Once monetary policy is hijacked by fiscal needs, the Federal Reserve will find it difficult to formulate neutral policies based on core objectives such as inflation and employment, ultimately damaging the credibility of the dollar and the stability of the global financial system.

Background: The previous QT round concluded smoothly, and calls for further reduction in the balance sheet are growing louder.

In the fourth quarter of last year, the Federal Reserve ended the latest round of quantitative tightening (QT) with a "quiet" operation, reducing its balance sheet by more than $2 trillion from a peak of nearly $9 trillion.

Unlike the 2019 QT, which was forced to halt due to the liquidity crisis, the smooth launch of QT this time confirms former Federal Reserve Chair Janet Yellen's expectation that it would be "like watching paint dry," and lays the foundation for subsequent policy implementation.

Today, Federal Reserve governors, academics, and former officials are calling for further reduction of the balance sheet, which reflects concerns about the "flattened mode" of banks and a deeper strategy to "force banks to transform, reduce their own burden of guaranteeing the market, and revitalize the Treasury bond market."

The core contradiction: Banks' reliance on reserve requirements increases pressure on the Federal Reserve to expand its balance sheet.

The core issue behind the Federal Reserve's insistence on continuing to shrink its balance sheet lies in banks' "excessive reliance" on reserves.

Post-crisis regulatory rules require banks to hold sufficient highly liquid reserves to cover deposit funding risks;

Meanwhile, banks' lending and credit business continues to create new deposits, which in turn further increases the demand for reserves.

To meet this demand, the Federal Reserve has had to passively increase its holdings of Treasury bonds and expand its balance sheet. This will not only distort the pricing of Treasury bonds and repurchase markets and weaken market liquidity, but also risk eroding the independence of the central bank.

(Chart showing the ratio of bank reserves held at the Federal Reserve / total bank deposits to bank reserves + Federal Reserve reverse repos ÷ total deposits)

The chart shows that as long as bank deposits grow, banks' demand for reserves will increase accordingly. Without regulatory reform, the Federal Reserve will always be forced to passively expand its balance sheet and buy more Treasury bonds, which is the Fed's biggest headache.

Solution: Reform regulation and guide banks to shift towards highly liquid assets.

To break this deadlock, the Federal Reserve's core idea is to reform policies so that banks no longer hoard large amounts of reserves and instead allocate highly liquid assets.

Among the series of proposals recently put forward by Federal Reserve economists, the most feasible is to optimize the regulatory rules for liquidity of large banks—allowing banks to use the discount window in extreme stress scenarios, while guiding them to replace some of their reserves with collateralizable assets such as Treasury bills and short-term agency bonds.

This reform not only removes the "stigma" of the use of central bank tools, but also allows banks to maintain a liquidity safety net while giving up the inertia of "earning interest passively";

For the Federal Reserve, this reduces the pressure of passively expanding its balance sheet, avoids having to bail out the market for an extended period, and thus maintains the independence and flexibility of monetary policy.

Market impact: Injecting incremental funds into the treasury bond market

From a market impact perspective, this reform is essentially about creating new demand for the government bond market.

The current yield curve for government bonds is steepening, giving banks a strong incentive to replace low-yield reserves with high-yield government bonds.

In the past, the Federal Reserve was the main "buyer" of Treasury bonds, but in the future, banks are expected to become an important source of incremental funds for the Treasury bond market, which will not only revitalize the liquidity of the Treasury bond market, but also reduce the burden of the Federal Reserve's continuous bond purchases.

The Federal Reserve plans to assess the effectiveness of its policies by monitoring changes in the spread between money market rates and the IORB and by surveying the minimum comfortable reserve levels of large banks. It is expected that after confirming a decrease in reserve demand of at least $500 billion, it may continue the gradual quantitative easing (QT) in the second half of next year.

(Payouts between different money market interest rates and the Federal Reserve Reserve Balance Rate (IORB))

IORB is the risk-free return banks receive for depositing money with the Federal Reserve, while other money market rates are the returns banks receive for lending money to the market. The spread between these two rates directly reflects the supply and demand of liquidity in the market.

When reserves are "excessive" (e.g., 2016-2019, 2021-2023), money market rates fall below the IORB, with the blue and purple lines remaining below the zero axis for extended periods, even reaching as low as -0.2%. When reserves are "tightened" (e.g., mid-2019, 2022 to present), the interest rate spread approaches the zero axis, and may even exceed the IORB (e.g., the surge in repo rates in September 2019).

Long-term value: Balance sheet reduction broadens policy space and strengthens regulatory capabilities.

Overall, the Fed's resumption of balance sheet reduction is not simply a matter of "shrinking liquidity," but rather a systemic adjustment that balances "reducing excessive reserves, activating market liquidity, and maintaining the central bank's independence."

As the balance sheet returns to a more reasonable size, the Fed's policy space will be greatly expanded: On the one hand, freed from the constraints of passive balance sheet expansion, the Fed can more flexibly adjust the intensity of its policies according to inflation trends. If inflation stickiness exceeds expectations, the liquidity tightening brought about by balance sheet reduction, in conjunction with interest rate tools, can more accurately suppress inflationary pressures on the demand side.

On the other hand, when the economy faces downside risks, the previously contracted balance sheet has reserved ample room for a new round of quantitative easing and liquidity injection, avoiding the predicament of "running out of policy ammunition".

This ability to "manage and adjust at will" will allow the Federal Reserve to be more proactive in balancing the goals of inflation control and economic growth, thus safeguarding its core mission of price stability and laying a solid monetary and financial foundation for sustainable growth in the U.S. economy.

As banks shift from "sitting back and earning interest" to market-based asset allocation, they will improve the efficiency of the financial system, make monetary policy transmission smoother, and ultimately form a virtuous cycle of "effective central bank regulation, sufficient market vitality, and stable economic operation".

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.