One chart: The Baltic Dry Index continues its upward trend, with rates increasing for all ship types.

2026-04-22 02:19:44

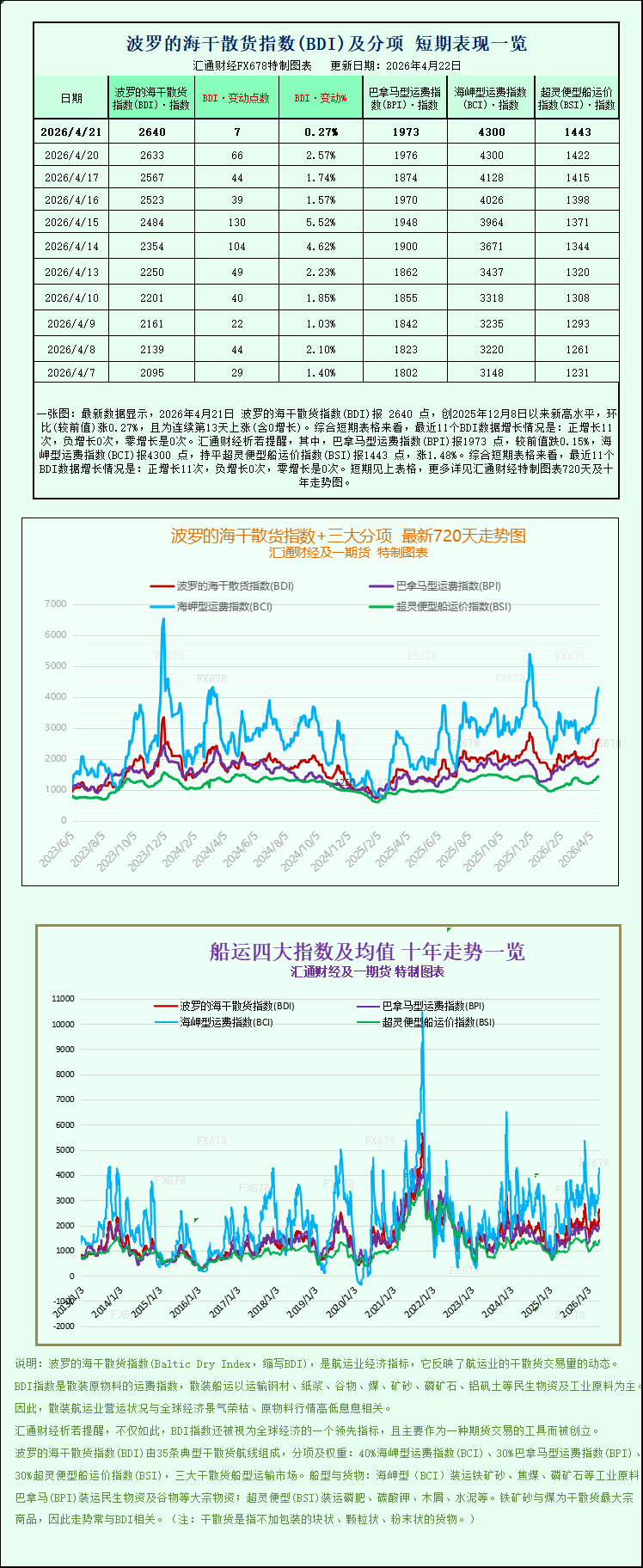

The latest data shows that the Baltic Dry Index (BDI) reached 2640 points on April 21, 2026, a new high since December 8, 2025, up 0.27% month-on-month, marking the 13th consecutive day of increase (including zero growth). Looking at the short-term charts, the BDI has seen positive growth 11 times, negative growth 0 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 1973 points, down 0.15% from the previous value; the Capesize Freight Index (BCI) was 4300 points; and the Supramax Freight Index (BSI) was unchanged at 1443 points, up 1.48%. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a slight increase on the day. As a core indicator of the global dry bulk shipping market, the index mainly monitors the fluctuations in maritime transportation costs for dry bulk commodities such as iron ore, coal, and grain worldwide. Its changes directly reflect the activity and market conditions of global dry bulk trade. This increase in the index was mainly due to the significant rebound in freight rates for Supramax vessels, while the overall shipping market showed a structural recovery trend.

Specifically, the Baltic Dry Index, which tracks freight rates for the three core vessel types—Capesize, Panamax, and Supramax—continued its upward trend, achieving a slight increase for the 13th consecutive trading day. It rose 7 points, or 0.3%, to close at 2640 points, the highest level since early December 2025. This steady increase over several days fully reflects the continued release of demand and increased activity in the dry bulk shipping market, sending a positive signal to the global commodity trade market.

Looking at specific vessel types, the Capesize index remained stable at a high level of 4300 points, marking its highest level in over four months and becoming a key force supporting the overall index stability. Capesize vessels, the "giants" of the dry bulk shipping market, primarily undertake the long-distance transport of large dry bulk cargoes, typically carrying up to 150,000 tons. Their core cargoes are basic industrial raw materials such as iron ore and coal, making them crucial transport carriers in the global steel industry supply chain. However, the average daily revenue of Capesize vessels carrying 150,000 tons of cargo fluctuated slightly, decreasing by $1 from the previous trading day, ultimately closing at $35,495. Despite the slight decline in daily revenue, it remains at a recent high level, indicating stable profitability for shipping companies.

The recovery in the dry bulk shipping market is closely related to the continued strength of the iron ore market. On that day, Dalian iron ore futures prices continued their upward trend, steadily climbing, mainly driven by two factors: Firstly, as the world's largest importer and consumer of iron ore, domestic steel mills in China have initiated raw material procurement plans ahead of schedule to prepare for the upcoming May Day holiday, increasing iron ore stockpiling and directly boosting demand for iron ore transportation. Secondly, major global iron ore exporters Australia and Brazil have recently experienced fuel shortages, raising concerns about potential iron ore supply disruptions. These changes in supply and demand expectations have further pushed up iron ore futures prices, indirectly leading to an increase in dry bulk shipping rates.

Unlike Capesize and Supramax vessels, the Panamax index saw a slight pullback, falling 1 point, or approximately 0.2%, to close at 1973 points, making it the only core vessel type index to decline that day. Panamax vessels are primarily used for short- to medium-haul dry bulk shipping, typically carrying between 60,000 and 70,000 tons. Their core cargoes are commodities such as coal and grain. Affected by the recent slowdown in global grain trade and a temporary adjustment in coal shipping demand, freight rates for Panamax vessels have slightly decreased. Correspondingly, the average daily earnings for Panamax vessels also fell by $27 to $17,758. Despite the decline, it remains within a reasonable range and has not significantly impacted the overall market recovery.

The Very Large Crude Carrier (VLCC) index performed strongly on the day, becoming one of the key drivers of the overall index rise. It rose 21 points, or 1.5%, to close at 1443 points. As a crucial component of the dry bulk shipping market, VLCCs primarily handle large-scale dry bulk cargo transportation. The increase in VLCC rates further confirms the comprehensive recovery of the global dry bulk shipping market, particularly the rebound in freight demand in Asia and the Indian Ocean region, which provided strong support for VLCC freight rates. Slight tightening of spot capacity supply in some key areas further pushed up rates.

Meanwhile, changes in the international geopolitical situation are also having a potential impact on the global shipping market. US President Trump publicly stated that he did not want to extend the expiring ceasefire agreement between the US and Iran, and clearly stated that the US military was "ready to act" if negotiations between the two sides failed. Trump added that the US military had completed sufficient resupply during the ceasefire and was now better prepared than four or five weeks ago, possessing the capability to respond to any changes in the situation. This statement has further escalated tensions between the US and Iran. As a vital global shipping route, the safety of passage through the Strait of Hormuz is of paramount importance. Subsequent developments may indirectly affect the route planning and transportation costs of global dry bulk shipping. The market needs to continue to monitor the further escalation of geopolitical risks.

The Baltic Dry Index (BDI) released by the London Baltic Exchange saw a slight increase on the day. As a core indicator of the global dry bulk shipping market, the index mainly monitors the fluctuations in maritime transportation costs for dry bulk commodities such as iron ore, coal, and grain worldwide. Its changes directly reflect the activity and market conditions of global dry bulk trade. This increase in the index was mainly due to the significant rebound in freight rates for Supramax vessels, while the overall shipping market showed a structural recovery trend.

Specifically, the Baltic Dry Index, which tracks freight rates for the three core vessel types—Capesize, Panamax, and Supramax—continued its upward trend, achieving a slight increase for the 13th consecutive trading day. It rose 7 points, or 0.3%, to close at 2640 points, the highest level since early December 2025. This steady increase over several days fully reflects the continued release of demand and increased activity in the dry bulk shipping market, sending a positive signal to the global commodity trade market.

Looking at specific vessel types, the Capesize index remained stable at a high level of 4300 points, marking its highest level in over four months and becoming a key force supporting the overall index stability. Capesize vessels, the "giants" of the dry bulk shipping market, primarily undertake the long-distance transport of large dry bulk cargoes, typically carrying up to 150,000 tons. Their core cargoes are basic industrial raw materials such as iron ore and coal, making them crucial transport carriers in the global steel industry supply chain. However, the average daily revenue of Capesize vessels carrying 150,000 tons of cargo fluctuated slightly, decreasing by $1 from the previous trading day, ultimately closing at $35,495. Despite the slight decline in daily revenue, it remains at a recent high level, indicating stable profitability for shipping companies.

The recovery in the dry bulk shipping market is closely related to the continued strength of the iron ore market. On that day, Dalian iron ore futures prices continued their upward trend, steadily climbing, mainly driven by two factors: Firstly, as the world's largest importer and consumer of iron ore, domestic steel mills in China have initiated raw material procurement plans ahead of schedule to prepare for the upcoming May Day holiday, increasing iron ore stockpiling and directly boosting demand for iron ore transportation. Secondly, major global iron ore exporters Australia and Brazil have recently experienced fuel shortages, raising concerns about potential iron ore supply disruptions. These changes in supply and demand expectations have further pushed up iron ore futures prices, indirectly leading to an increase in dry bulk shipping rates.

Unlike Capesize and Supramax vessels, the Panamax index saw a slight pullback, falling 1 point, or approximately 0.2%, to close at 1973 points, making it the only core vessel type index to decline that day. Panamax vessels are primarily used for short- to medium-haul dry bulk shipping, typically carrying between 60,000 and 70,000 tons. Their core cargoes are commodities such as coal and grain. Affected by the recent slowdown in global grain trade and a temporary adjustment in coal shipping demand, freight rates for Panamax vessels have slightly decreased. Correspondingly, the average daily earnings for Panamax vessels also fell by $27 to $17,758. Despite the decline, it remains within a reasonable range and has not significantly impacted the overall market recovery.

The Very Large Crude Carrier (VLCC) index performed strongly on the day, becoming one of the key drivers of the overall index rise. It rose 21 points, or 1.5%, to close at 1443 points. As a crucial component of the dry bulk shipping market, VLCCs primarily handle large-scale dry bulk cargo transportation. The increase in VLCC rates further confirms the comprehensive recovery of the global dry bulk shipping market, particularly the rebound in freight demand in Asia and the Indian Ocean region, which provided strong support for VLCC freight rates. Slight tightening of spot capacity supply in some key areas further pushed up rates.

Meanwhile, changes in the international geopolitical situation are also having a potential impact on the global shipping market. US President Trump publicly stated that he did not want to extend the expiring ceasefire agreement between the US and Iran, and clearly stated that the US military was "ready to act" if negotiations between the two sides failed. Trump added that the US military had completed sufficient resupply during the ceasefire and was now better prepared than four or five weeks ago, possessing the capability to respond to any changes in the situation. This statement has further escalated tensions between the US and Iran. As a vital global shipping route, the safety of passage through the Strait of Hormuz is of paramount importance. Subsequent developments may indirectly affect the route planning and transportation costs of global dry bulk shipping. The market needs to continue to monitor the further escalation of geopolitical risks.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.