One chart: With both supply and demand for shipping capacity benefiting, the Baltic Dry Index has risen for two consecutive months, and the shipping market continues to see increased activity.

2026-05-29 22:42:17

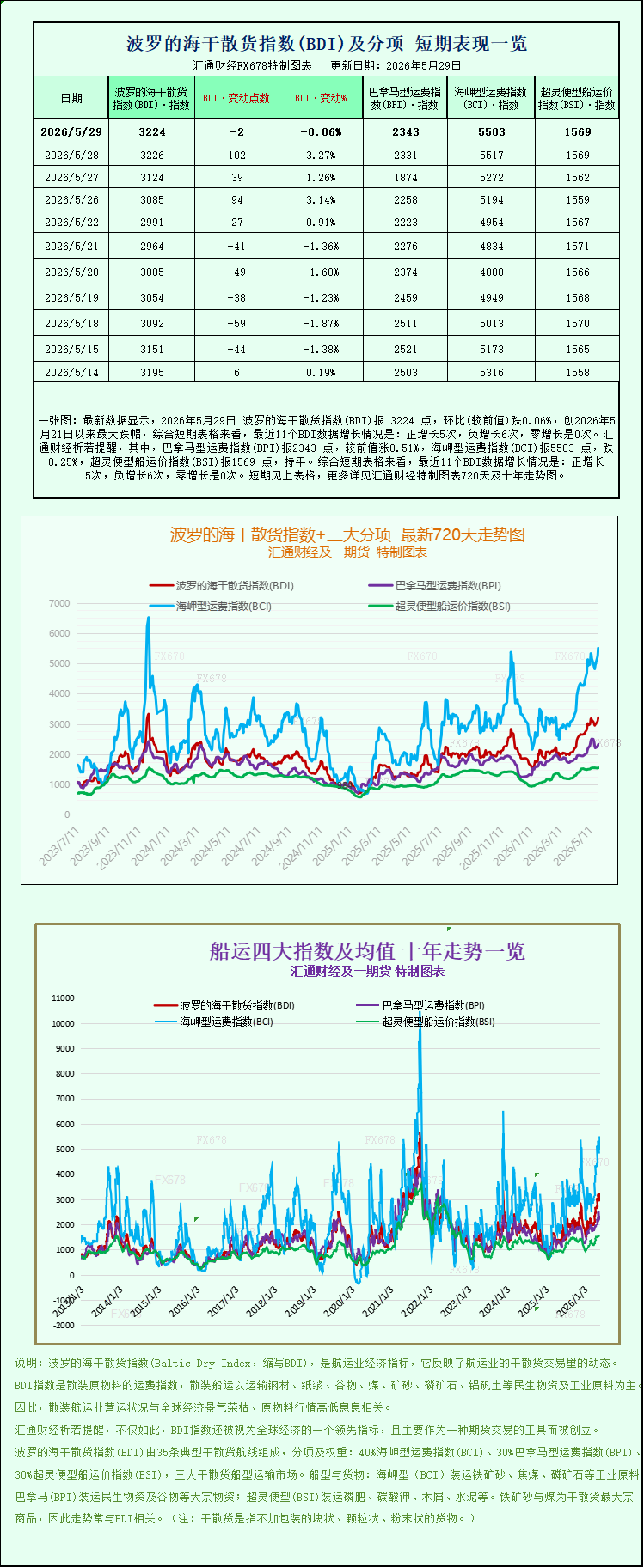

The latest data shows that the Baltic Dry Index (BDI) was 3224 points on May 29, 2026, a decrease of 0.06% compared to the previous week, marking the largest drop since May 21, 2026. Looking at the short-term charts, the BDI has seen positive growth 5 times, negative growth 6 times, and zero growth 0 times in the last 11 BDI data points. Specifically, the Panamax Freight Index (BPI) was 2343 points, up 0.51% from the previous week; the Capesize Freight Index (BCI) was 5503 points, down 0.25%; and the Supramax Freight Index (BSI) was 1569 points, unchanged. For detailed 720-day and 10-year trend charts of the Baltic Dry Index and its three main sub-indices, please refer to the specially designed charts.

The global dry bulk shipping market continues its overall recovery, supported by both increased effective shipping capacity and a rebound in global demand for commodity transportation. The Baltic Dry Index has now risen for the second consecutive month. Even with a slight pullback today, the overall upward trend in the industry remains unchanged, and the shipping market is currently maintaining its recent high levels.

On that day, the Baltic Dry Index (.BADI), which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—fell slightly lower by 2 basis points, a decrease of 0.1%, and finally closed at 3224 points. Historically, the index remains firmly within its high range since December 2023; monthly analysis shows a cumulative increase of 20% this month, marking two consecutive months of gains, directly reflecting the overall recovery of the global dry bulk shipping industry.

In the segmented vessel market, the market for large Capesize vessels weakened somewhat during the day. Data shows that the Capesize-specific freight index fell 14 points, a decrease of 0.3%, closing at 5503 points. However, looking at a longer time frame, the index for this vessel type still shows a strong increase this month, with a cumulative rise of approximately 27%, which was one of the core drivers of the previous upward trend in the overall market index.

It is understood that Capesize vessels primarily carry bulk industrial raw materials such as iron ore, thermal coal, and coking coal, with a single vessel having a deadweight tonnage of up to 150,000 tons. They are the core vessel type for transoceanic bulk raw material transportation. On that day, the average daily earnings for this type of vessel (BATCA) declined by $127, with a final average daily revenue of $46,411. The slight decline in earnings was mainly due to short-term profit-taking and did not change the long-term demand pattern of downstream steel mills and energy companies for essential goods.

Market fluctuations in energy raw materials also indirectly affect the dry bulk shipping market. This Friday, Chinese coking coal spot and futures prices fluctuated, with intense competition between bulls and bears. However, overall, coking coal prices are still expected to achieve their best weekly gain in six weeks. Domestically, to smoothly prepare for the summer peak electricity consumption season, domestic regulatory authorities have introduced policies requiring a stable supply of electricity and heat-related energy materials, stimulating increased demand for coal exports. Simultaneously, some domestic coal mines have temporarily suspended production due to safety accidents, leading to expectations of a tightening coal supply. These two factors offset each other, resulting in differentiated trends in the coal transportation market and indirectly supporting long-haul shipping demand for large bulk carriers. In addition, global iron ore market demand remains resilient, overseas mine shipments are stable, and domestic steel companies' restocking demand further solidifies the market demand for Capesize vessels.

The medium-sized vessel sector performed particularly well, becoming one of the few sectors to rise in the market that day. The Panamax index rose 12 points, or 0.5%, to close at 2343 points, marking its second consecutive month of gains, indicating strong upward potential for the industry.

Panamax vessels, with a deadweight range of 60,000 to 70,000 tons, are primarily responsible for regional and transoceanic transportation of essential goods and industrial supplies such as coal, grain, and fertilizer, making them highly adaptable. Data shows that the average daily charter rate for this vessel type (BPWT) increased by $108 that day, reaching $21,086. Industry analysts indicate that the arrival of the peak summer harvest and trade season in the Northern Hemisphere has led to a continued increase in global grain trade orders, while demand for coal transportation in the Asia-Pacific region remains high. These dual positive factors have driven a steady rise in Panamax freight rates.

The market for small dry bulk carriers remained generally stable. The Supramax index, primarily for short-haul and regional transport, remained unchanged from the previous trading day at 1569 points, continuing its overall upward trend over the past two months. This type of vessel, with its high flexibility and wide port coverage, mainly handles small- to medium-sized bulk transport of raw materials, building materials, and agricultural products. Benefiting from increased global regional trade activity, the market fundamentals are solid, and prices have not fluctuated significantly.

Looking ahead, many shipping industry analysts believe that in the short term, the new effective capacity of global dry bulk carriers and the seasonal demand for bulk commodity transportation will continue to resonate, coupled with the peak season for energy and grain trade in summer. The dry bulk shipping index is likely to maintain a high-level fluctuation pattern, and different ship types may show differentiated rise and fall trends based on the demand of downstream sub-categories.

The global dry bulk shipping market continues its overall recovery, supported by both increased effective shipping capacity and a rebound in global demand for commodity transportation. The Baltic Dry Index has now risen for the second consecutive month. Even with a slight pullback today, the overall upward trend in the industry remains unchanged, and the shipping market is currently maintaining its recent high levels.

On that day, the Baltic Dry Index (.BADI), which tracks freight rates for the three major dry bulk shipping types—Capesize, Panamax, and Supramax—fell slightly lower by 2 basis points, a decrease of 0.1%, and finally closed at 3224 points. Historically, the index remains firmly within its high range since December 2023; monthly analysis shows a cumulative increase of 20% this month, marking two consecutive months of gains, directly reflecting the overall recovery of the global dry bulk shipping industry.

In the segmented vessel market, the market for large Capesize vessels weakened somewhat during the day. Data shows that the Capesize-specific freight index fell 14 points, a decrease of 0.3%, closing at 5503 points. However, looking at a longer time frame, the index for this vessel type still shows a strong increase this month, with a cumulative rise of approximately 27%, which was one of the core drivers of the previous upward trend in the overall market index.

It is understood that Capesize vessels primarily carry bulk industrial raw materials such as iron ore, thermal coal, and coking coal, with a single vessel having a deadweight tonnage of up to 150,000 tons. They are the core vessel type for transoceanic bulk raw material transportation. On that day, the average daily earnings for this type of vessel (BATCA) declined by $127, with a final average daily revenue of $46,411. The slight decline in earnings was mainly due to short-term profit-taking and did not change the long-term demand pattern of downstream steel mills and energy companies for essential goods.

Market fluctuations in energy raw materials also indirectly affect the dry bulk shipping market. This Friday, Chinese coking coal spot and futures prices fluctuated, with intense competition between bulls and bears. However, overall, coking coal prices are still expected to achieve their best weekly gain in six weeks. Domestically, to smoothly prepare for the summer peak electricity consumption season, domestic regulatory authorities have introduced policies requiring a stable supply of electricity and heat-related energy materials, stimulating increased demand for coal exports. Simultaneously, some domestic coal mines have temporarily suspended production due to safety accidents, leading to expectations of a tightening coal supply. These two factors offset each other, resulting in differentiated trends in the coal transportation market and indirectly supporting long-haul shipping demand for large bulk carriers. In addition, global iron ore market demand remains resilient, overseas mine shipments are stable, and domestic steel companies' restocking demand further solidifies the market demand for Capesize vessels.

The medium-sized vessel sector performed particularly well, becoming one of the few sectors to rise in the market that day. The Panamax index rose 12 points, or 0.5%, to close at 2343 points, marking its second consecutive month of gains, indicating strong upward potential for the industry.

Panamax vessels, with a deadweight range of 60,000 to 70,000 tons, are primarily responsible for regional and transoceanic transportation of essential goods and industrial supplies such as coal, grain, and fertilizer, making them highly adaptable. Data shows that the average daily charter rate for this vessel type (BPWT) increased by $108 that day, reaching $21,086. Industry analysts indicate that the arrival of the peak summer harvest and trade season in the Northern Hemisphere has led to a continued increase in global grain trade orders, while demand for coal transportation in the Asia-Pacific region remains high. These dual positive factors have driven a steady rise in Panamax freight rates.

The market for small dry bulk carriers remained generally stable. The Supramax index, primarily for short-haul and regional transport, remained unchanged from the previous trading day at 1569 points, continuing its overall upward trend over the past two months. This type of vessel, with its high flexibility and wide port coverage, mainly handles small- to medium-sized bulk transport of raw materials, building materials, and agricultural products. Benefiting from increased global regional trade activity, the market fundamentals are solid, and prices have not fluctuated significantly.

Looking ahead, many shipping industry analysts believe that in the short term, the new effective capacity of global dry bulk carriers and the seasonal demand for bulk commodity transportation will continue to resonate, coupled with the peak season for energy and grain trade in summer. The dry bulk shipping index is likely to maintain a high-level fluctuation pattern, and different ship types may show differentiated rise and fall trends based on the demand of downstream sub-categories.

- Risk Warning and Disclaimer

- The market involves risk, and trading may not be suitable for all investors. This article is for reference only and does not constitute personal investment advice, nor does it take into account certain users’ specific investment objectives, financial situation, or other needs. Any investment decisions made based on this information are at your own risk.